TPG's comprehensive guide to independent travel insurance — including coronavirus coverage

Update: Some offers mentioned below are no longer available. View the current offers here.

As we head into the middle of summer and vaccination rates continue to expand, travel is surging back. More countries are opening back up to tourists, and many U.S. destinations are seeing a notable uptick in visitors. If you are planning to travel this year, it's a good idea to think about third-party travel insurance. No one wants to think about having to cancel a trip last minute or something going wrong while away from home. But having travel insurance can help give you peace of mind and potentially save you hundreds or even thousands in case things do go awry.

We'll start off with everything you need to know about third-party travel insurance coverage during the COVID-19 pandemic before diving into the ins and outs of trip protection as a whole.

Interested in travel insurance? Visit InsureMyTrip.com to shop for plans that will fit your travel needs.

Trip insurance during COVID-19: What you need to know

We'll give you the bad news first: Some travel insurance plans do not cover coronavirus disruptions. This holds true whether your plan is included with your credit card or was purchased from a third-party provider. The most important thing to do is carefully review the policy details — some plans specifically exclude COVID-19, while others exclude pandemics in general.

Related: Will future travel insurance plans offer coronavirus protection? Experts say yes

While it's true that trip insurance covers illness and emergency evacuations, the coronavirus pandemic does not fall under the qualifying criteria unless you personally have been diagnosed with the coronavirus, which falls under the typical clauses on illness.

Travel insurance doesn't cover cancellations from airlines, restricted country entrance guidelines based on coronavirus-related border closures or many of the pandemic-related reasons why you might not be able to complete a trip as planned.

Plans typically cover unforeseen issues such as accidental bodily injury; loss of life or sickness; severe weather; terrorist incident; and jury duty or a court subpoena that cannot be postponed or waived. If you need to cancel your trip and are looking for full reimbursement under the policy, it must be due to a covered reason listed within the policy's wording.

Some airlines now offer free coronavirus coverage — but even if you qualify, your coverage and benefits are often quite limited.

How many insurance plans offer COVID-19 coverage?

Your insurance options will vary depending on your destination, trip duration and many other factors. However, let's show you an example in action from the insurance marketplace website InsureMyTrip.

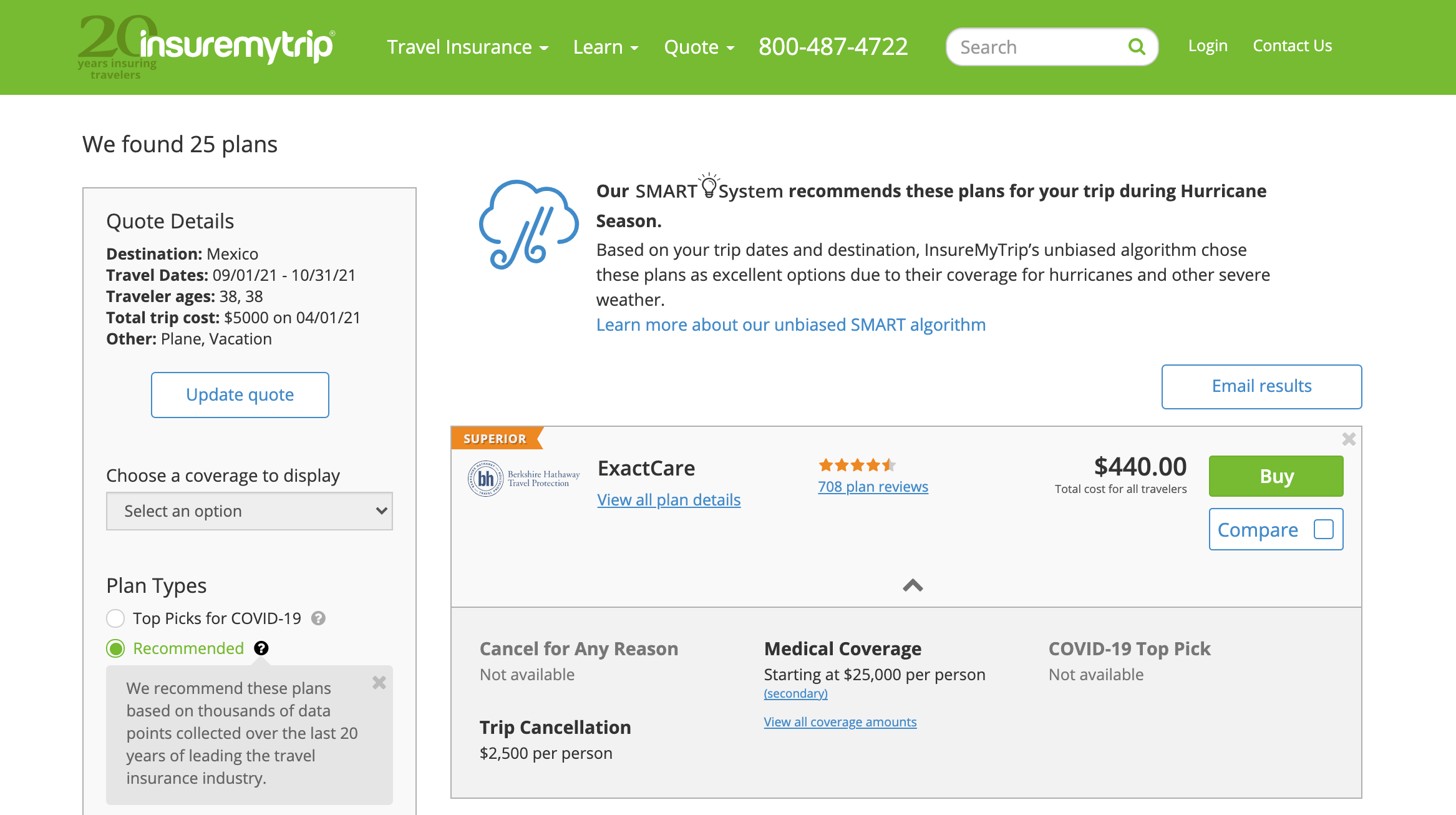

In the screenshot below, you'll see that a traveler from New York purchasing insurance for a hypothetical two-month stay in Mexico in the fall of 2021 has 25 plans to choose from.

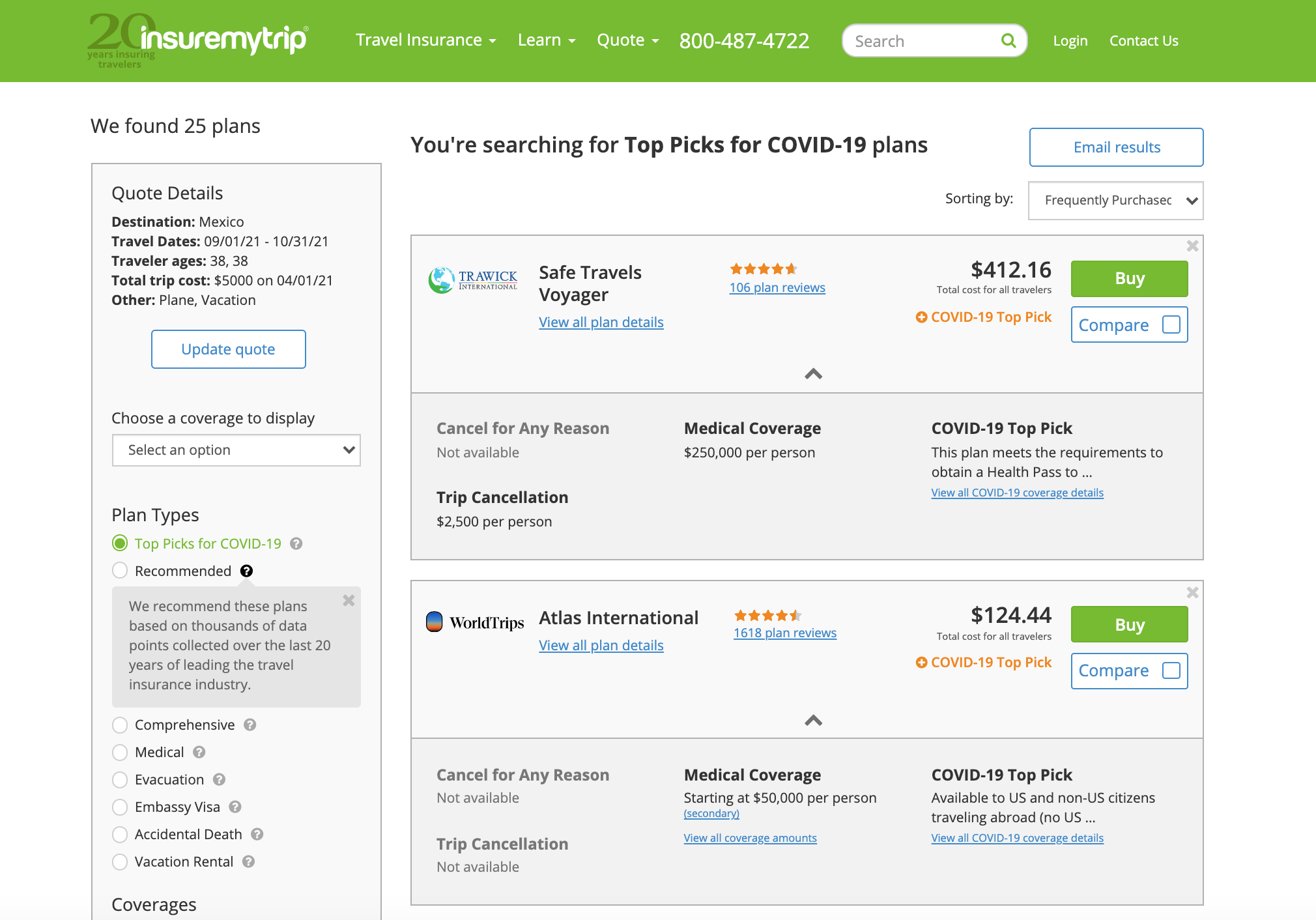

However, someone looking for COVID-specific coverage should select the "Top Picks for COVID-19" option at the left-hand side of the results page. This will then display the best options for your unique travel details.

Furthermore, costs and coverage vary significantly between the coronavirus-covered plans. A comprehensive plan in this example trip — issued by Trawick International in the above screen shot — starts at $412.16, while a basic medical plan with emergency coverage for serious COVID-19 issues only — issued by WordTrips — costs $124.44.

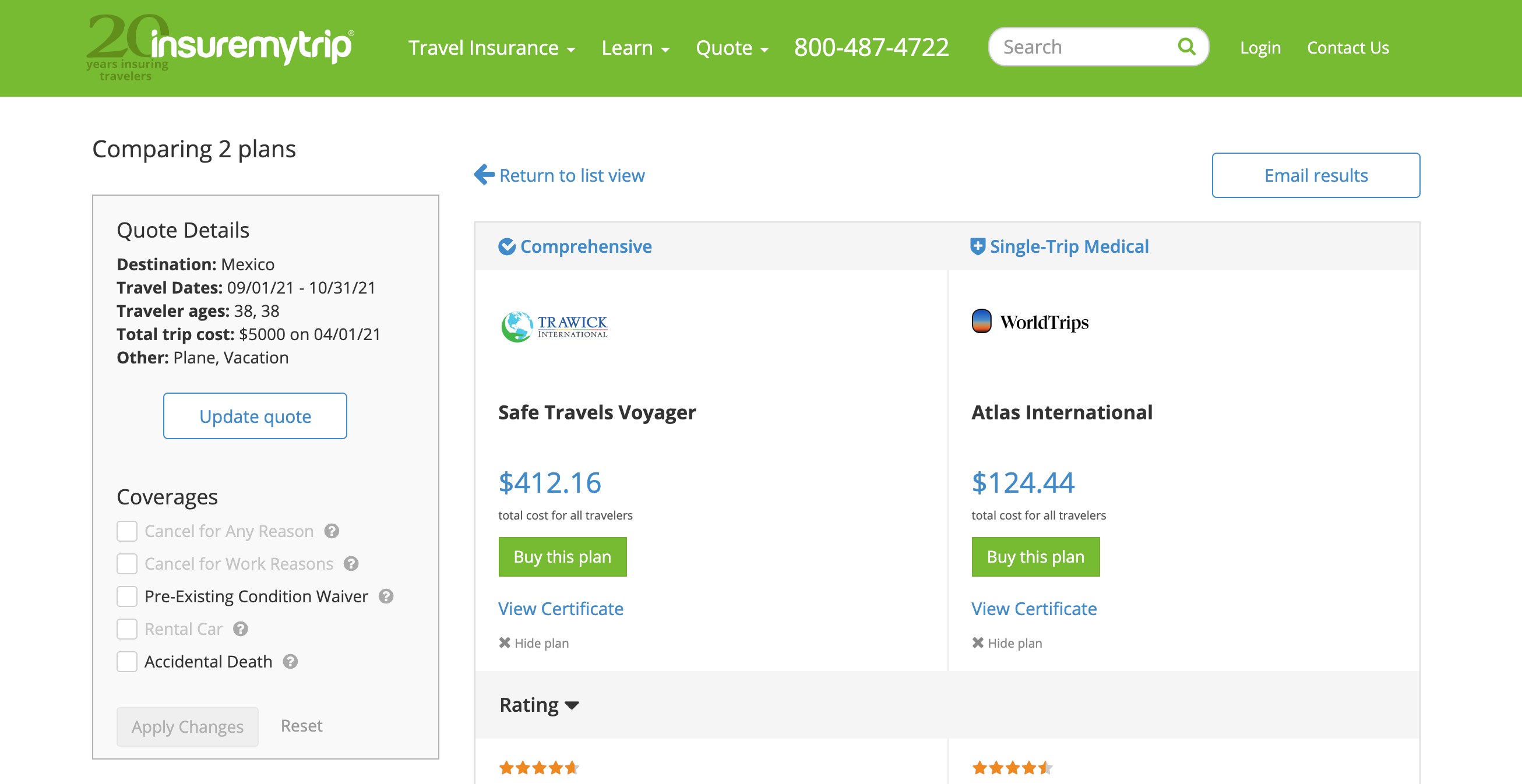

The easiest way to do a side-by-side comparison of these plan options is by checking the Compare boxes for each of them.

From this page, you'll see that the comprehensive plan (Safe Travels Voyager) is just that — comprehensive. For the significantly higher cost, you're receiving trip cost protection along with coverage for baggage loss or delay, travel delay, emergency medical, emergency medical evacuation and more. The Travel Medical Plan, on the other hand, only offers coverage for emergency medical services (including evacuation) and only when you leave your home country. This medical plan won't offer any assistance if you aren't traveling abroad.

So, if you're worried about losing money on a trip due to contracting COVID-19 or other related fears, what should you do?

Haven't left home yet? Purchase "cancel for any reason" or coronavirus-specific coverage before you go.

If you're planning for a trip in the near future, you may still be able to purchase coverage now.

But while you can usually purchase basic travel insurance up to 24 hours before departure, most premium add-ons such as "cancel for any reason" coverage must be purchased within a certain number of days from when you made your initial trip payment. If you've already had a trip planned for some time but haven't purchased insurance yet, do some research to see if you're still within the correct timeframe from your initial trip payment in order to qualify for "cancel for any reason" coverage — or other time-sensitive benefits.

If you're worried you may need to cancel your trip for a pandemic-related reason, a "cancel for any reason" insurance plan could be a good investment to hedge your bets. Some comprehensive plans will offer "cancel for any reason" coverage if all eligibility requirements are met, but that option will cost more — usually an additional 40-50% on top of the base premium.

With Squaremouth travel insurance, for example, you'll have to purchase "cancel for any reason" insurance within 14 to 21 days of making your initial payment on vacation expenses, and you also have to insure 100% of your trip costs in addition to canceling your trip at least 48 hours before departure time to receive a refund of up to 75% of the trip cost.

Related: Everything you need to know about "cancel for any reason" travel insurance

If you're only concerned about worst-case scenarios, consider a medical evacuation plan

As of Jan. 26, 2021, travelers entering the U.S. must provide proof of a negative COVID-19 test before boarding their international flight into the country.

But, this policy did raise questions for some travelers: What if a traveler is asymptomatic, or the test result is a false positive? Where can tests be found last minute? If a traveler can't return home, who foots the bill for unexpected expenses?

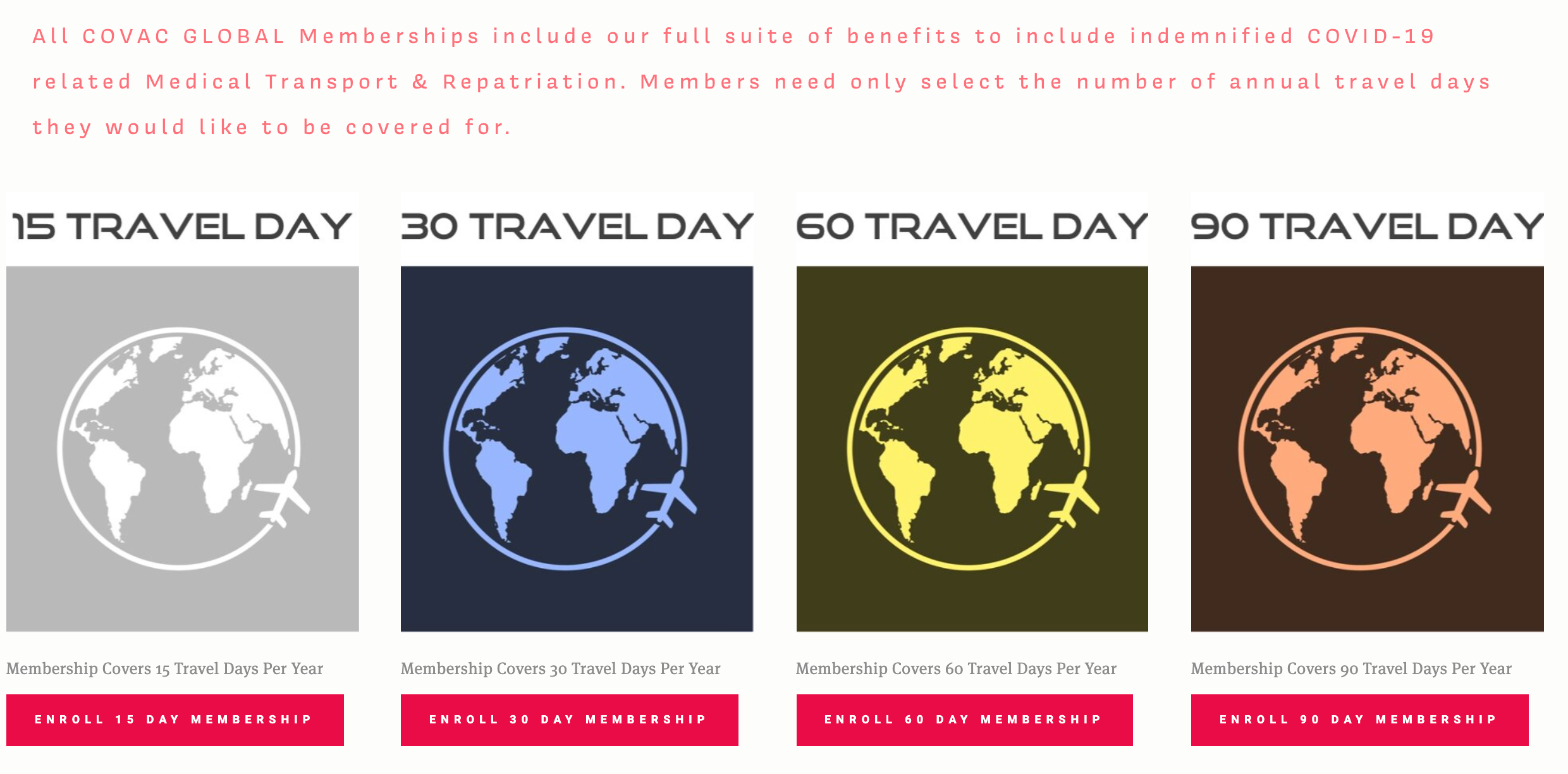

Enter companies like COVAC GLOBAL, which offer coronavirus-positive travelers a way to get home without flouting CDC requirements.

While commercial, private and charter flight passengers are all subject to the health requirements, medical transports are exempt. Thus, COVAC's insurance policy offers customers the guarantee of a private flight home on a medical transport aircraft, provided the traveler holds a positive PCR test result and shows at least one COVID-19 symptom.

COVAC's unique plan rates begin as low as $27 per person per day (on the 90-day membership), although travelers must purchase a minimum of 15 days of coverage at once. But customers can use the coverage days however they like. For example, a four-day trip this month would mean 11 days of coverage left over for future travel.

As with other forms of insurance, however, travelers can't purchase a COVAC plan when they test positive; plans require a 14-day delay between purchase and effective date.

Medjet is another popular evacuation company offering coverage that's different from typical travel insurance. Travelers who hold Medjet memberships can be transferred to their home hospital of choice, regardless of medical necessity. Even better: Your Medjet membership doesn't exclude adventure travel, has very few limitations and no preexisting condition exclusions for travelers under 75 — many of the disqualifications people face when shopping for travel insurance coverage.

What if I'm afraid to travel?

Unfortunately, risk aversion isn't a covered reason under trip cancellation or interruption protection. Even an alert from the U.S. Centers for Disease Control and Prevention for your destination won't be sufficient for most plans to offer financial relief.

Under what situations might I qualify for trip protection?

- If your doctor issues a note stating that you're too ill to fly, you may be able to file a claim under trip cancellation for reimbursement of your insured, prepaid, nonrefundable trip costs. That said, all details of the claim are reviewed once it has been filed, and every situation is different — so this is no guarantee of reimbursement. However, if you're immunocompromised and can prove you will suffer high risk from germ exposure, a travel insurance policy with the optional cancel for any reason benefit might help you recoup some of your lost travel costs.

- If you've been ordered to quarantine for safety precautions — even if you don't ultimately get sick — your insurance may cover your unexpected costs under the "trip cancellation and interruption" clause on your policy. However, this quarantine typically must be ordered by a doctor (or by a government, on some plans) to trigger coverage, and it typically requires strict isolation. In other words, a self-imposed quarantine will not be covered, so it's important to know exactly how your policy defines "quarantine" and what requirements go along with it.

Should I just stay at home?

Travel is on the rebound as we enter the latter half of 2021, but there are still hoops to jump through depending on where you plan to travel. Whether or not you should stay home is a personal decision, to be made with your doctors and with your community in mind. If you are in frequent contact with high-risk individuals, it might behoove you to postpone your trip for the time being.

But whether you stay or you go, travel insurance can be one powerful tool in protecting your trip.

Want to learn more about trip protection? Keep reading our guide to independent travel insurance below.

For more travel news and advice during COVID-19, make sure to check out our dedicated coronavirus hub page.

What is independent travel insurance, and when do I need it?

More than ever, travelers need to be prepared for times when travel plans go awry — like I experienced on a trip to Italy in the summer of 2018 (more on that below).

But the term travel insurance is often used interchangeably with trip protection and cancellation coverage, and it can be difficult to tell if your credit card benefits offer sufficient peace of mind for big or complex trips.

Related: The best credit cards with complimentary travel protection

So, what exactly is independent travel insurance, and how does it differ from credit card trip delay reimbursement, trip cancellation and interruption protection or accident and evacuation insurance?

A travel insurance plan can offer valuable protection

In a nutshell, travel insurance can help to protect your financial investment in a trip. If your domestic flight is delayed, a service like Freebird previously could help you get on another flight, sometimes even through another airline. (Unfortunately, Freebird is not an option right now, but it isn't dead: Capital One now owns the company and technology.)

But you won't be reimbursed for other consequences of your flight delay; for instance, you usually can't get your money back for a missed hotel stay resulting from your delayed flight.

Your premium credit card benefits usually offer plenty of protection for your average domestic weekend getaway. But while card benefits vary, many only cover transportation-related cancellation or interruption costs in the event of illness, injury or death.

Furthermore, most credit card-based benefits only cover expenses and activities paid with that particular credit card. Finally, credit card terms and conditions may limit you to a certain number of claims or maximum reimbursement amount within 12 months.

Related: When to buy travel insurance vs. when to rely on your credit card protections

However, many credit cards don't provide robust protection, and even those that do provide coverage have many exclusions and exceptions — and zero options for customization. While travel insurance plans also have exclusions, you may be a great candidate for third-party coverage if you're looking for more options.

You can purchase a third-party plan for pretty much any kind of trip, which will cover many aspects of your travel from the flights and hotel stays to the prepaid, nonrefundable tours and excursions. There's a wide variety of policies available, from comprehensive coverage to plans that offer coverage for specific travel-related concerns — like emergency medical evacuation or travel medical protection.

If you're looking for broad coverage, look for a comprehensive travel insurance plan that can cover your costs in the event of canceled, delayed or interrupted transportation; medical expenses and emergency evacuations; as well as any costs associated with lost or delayed luggage.

Where should I shop for travel insurance?

Independent travel insurance plans can be purchased from providers such as Allianz and WorldNomads, and typically offer coverage that's more comprehensive than the protection included with your credit card.

You can expect your insurance plan to cost between 4–12% of your total trip expenses, depending on the plan you purchase. So if you spent $1,000 on your next vacation, for example, expect to pay between $40–$120 for a standard, comprehensive travel insurance plan.

Related: Should I buy trip insurance from my airline during checkout?

But not all plans and protection are created equal. Third-party travel insurance plans also differ from the trip protection add-on you can buy through your airline. Airline trip protection typically costs more and covers less than a travel policy purchased through a dedicated underwriter.

Additionally, airline trip protection only covers the flight-related portion of your travel and specifically targets delays or cancellations relevant to natural disasters, or dire circumstances such as a death in the family. Finally, as we saw above, not all plans include COVID-19 coverage, so you'll need to keep that in mind when shopping your options.

Related: Comparing the best travel insurance policies and providers

One option for doing so is InsureMyTrip.com, which offers an easy, straightforward way to compare plans, prices, ratings and some other factors side by side. You can thus opt for the protection that works best for your unique needs — whether that's a comprehensive plan or a policy that addresses your specific, travel-related concerns.

Usually, the basic requirement is that all coverage kicks in only if you are located a certain distance away from your primary residence (the home address listed in your plan).

Whatever you do, don't buy the "travel insurance" offered on the airline checkout page when you're purchasing your next flight without shopping around — and reading the fine print. While the plan may be offered through a reputable provider, you'll pay about the same amount for a plan that isn't offered through the airline — thus maintaining a lot more flexibility to select terms that make sense for you.

What types of coverage do these plans offer?

Trip cancellation coverage targets nonrefundable portions of your trip, from flights to excursions and hotel stays.

Most hotels and tour groups have very strict rules regarding last-minute cancellations or missed travel, so you most likely will not be able to get a refund if a canceled or delayed flight prevents you from reaching your destination. If you've planned a full, expensive vacation with many moving parts, travel insurance is the best way to protect your investment.

That said, it's critical to carefully read your policy to understand what is (and is not) covered — especially for exclusions that may prevent you from getting reimbursed when something goes wrong during a trip. If you need complete peace of mind, you can opt for plans that offer optional "cancel for any reason" or "cancel for work reasons" coverage, which will offer the most flexibility.

Trip interruption coverage is very similar to cancellation coverage, though it offers post-departure coverage rather than pre-departure protection. The wording may differ slightly, and the coverage amount can be even higher to take into account emergency flights home in the event of a covered interruption. If you're already partially through your trip and need to change your itinerary, head home early or reroute your plans for a covered reason, the plan may reimburse you for the unused portion of your trip — and may cover additional costs for last-minute travel changes.

Medical expenses can encompass anything from a saline-drip IV for heat exhaustion to serious injuries treated in the emergency room or a hospital overseas. Most health insurance plans in the U.S. don't cover international incidents or needs that arise, and a travel insurance plan can provide coverage for accidents and illnesses while abroad.

Related: I got food poisoning right before my international flight from Africa

Emergency evacuation coverage can easily save you tens of thousands in out-of-pocket expenses if you need an unexpected helicopter airlift, medically equipped flights home or ambulance transportation to a local hospital. However, this is at the discretion of the attending physician and the company. Typically, evacuation occurs if it's determined that you can't be treated properly at the hospital to which you are initially taken.

Lost or delayed luggage and delayed flights can happen at any time, and they can create a number of headaches for travelers. Third-party travel insurance may provide reimbursement here. Baggage loss coverage provides reimbursement for luggage as well as covered items that are lost or stolen while you're traveling, while baggage delay coverage allows you to purchase essential items you need for your personal comfort while you're waiting for your bags to arrive. Meanwhile, trip delay protection may offer reimbursement for additional expenses incurred due to a late-arriving flight or missed connection — including unexpected, overnight hotel stays or nonrefundable tours you missed as a result of the delay.

However, these are typically secondary coverage — so they'll supplement any reimbursements offered by a common carrier (like an airline that loses your bag or delays your flight) or your homeowner's insurance. In addition, plan limits define the amount of coverage, which varies by plan.

It's also worth noting here that many credit cards also offer protection for things like trip delays and lost luggage. Once again, be sure to carefully compare the details of these offerings to those from a third-party insurance provider to select the one that best meets your needs.

Related: These cards offer luggage delay and loss insurance

Additional coverage options

If you need or want more robust insurance for peace of mind, providers also offer add-on options for:

- Accidental death and dismemberment

- Hazardous sports

- Rental car collision damage (though not liability)

Note that death/dismemberment insurance and rental car coverage are frequently offered with many credit cards, so check your card benefits before purchasing these add-ons to avoid redundant coverage.

When travel insurance plans are a great idea

Still unsure of whether independent travel insurance is something you should consider? Here are a few scenarios in which travel insurance might make sense for you:

You're traveling in a group, especially with small children

There are a variety of things that can go wrong when traveling with your family or in a large group — more travelers means greater potential for sickness, injury or other covered reasons that could offer reimbursement under travel insurance. And standard, comprehensive travel insurance plans typically cover up to 10 travelers. A few hundred dollars spent on a good policy can save you thousands in otherwise-sunk costs in the event of an emergency.

When traveling with her niece or nephews overseas, Shannon O'Donnell of A Little Adrift purchased insurance plans that, among other protections, covered travel costs for a back-up guardian in case she became ill or injured — a scenario that doesn't typically occur to most travelers.

You need medical protection overseas

If you plan to hike Machu Picchu, backpack your way through Southeast Asia or undertake any other equally adventurous trip, it can be a good idea to look into two different types of coverage:

- Emergency medical evacuation coverage: This provides transport assistance in the event that you become seriously ill or injured while traveling. Generally, these plans provide emergency medical evacuation to the nearest appropriate care facility if the assistance company and the physician feel you'd be better suited at a different facility.

- Travel medical coverage: These plans offer specific, defined coverage needed by some while traveling abroad. These are only available to travelers who are leaving their home country and who require medical insurance that will fill the gaps in their primary health insurance coverage while traveling internationally.

Most credit card benefits don't offer robust medical expense or evacuation coverage, so if you need one or both of these coverages, you may want to purchase a comprehensive travel insurance plan.

Bear in mind that Medicare doesn't offer any international assistance, and U.S.-based private health insurance plans offer little to no coverage for international travel. Countries with universal health care may offer some basic help, but they aren't obligated to do so, especially if you aren't a citizen.

You're planning a complex trip with many moving parts

There are a few ways you can purchase insurance, even if you're planning a long-term trip.

In 2015, Connie Wang quit her job to travel the world for 15 months by stringing together a series of shorter trips across 47 countries and six continents. Instead of purchasing one giant insurance plan for the full year, she purchased individual plans for each leg of her travels through World Nomads as she went. Purchasing insurance this way lessened her upfront travel expenses and simplified the stress of planning each activity months in advance.

However, many travel agents and full-time nomads prefer to purchase annual insurance coverage, such as the year-round plan offered by TravelGuard. With an annual policy, you can book a trip in the next 30 minutes without the additional stress of scrambling for last-minute coverage.

When purchasing travel insurance may be unnecessary

On the flip side, there are plenty of trips where a separate insurance plan would be overkill. Here are a few examples:

You're traveling on a domestic flight worth $300 or less, and staying with friends or family

Usually, a trip of this cost won't be worth the additional cost of a travel insurance plan. In this situation, your credit card trip delay protection will most likely prove more than sufficient to cover any expenses incurred as a result of travel delays.

Your trip is already refundable

If you book a flight through an airline like Southwest, a travel insurance claims adjuster may see that the airline issued travel credit for the value of a canceled ticket, and refuse to further reimburse you for your sunk travel costs. This is especially important to consider now that most U.S. airlines have committed to permanently removing change fees.

Related: What to do when an airline changes your flight

While many of us purchase nonrefundable flights these days, this would also be the case if you purchase a fully-refundable premium-cabin flight in cash. For example, an underwriter may ask why you didn't pursue a refund with the airline directly instead.

You're traveling on award bookings

Insurance companies will only reimburse your actual spend, not the value of your seat. A round-trip Singapore Suites ticket may be worth $13,000 but when your underwriter sees that you only paid $203 in fees, your financial return on insurance investment will be very low.

Instead, look into your airline's policies regarding canceled or missed award travel for help. In some cases, you may be eligible for a partial or full refund, although redeposit fees will often apply. Cards such as the Chase Sapphire Preferred Card are eligible for compensation on award redemptions.

You rarely plan big, complicated or dangerous trips

Many cards limit protection claims under a certain dollar amount within 12 months. So if you've already filed a large insurance claim with your credit card company within the past year, independent travel insurance might be a wise purchase to consider for your next trip.

But if you're only on the road once or twice a year, those limited protection claims might be sufficient for your needs.

How to find and purchase travel insurance

Katie Warner, CEO of Lucid Routes, recommends travelers price-shop for insurance as soon as they make their initial trip payment so they can take full advantage of the coverage options that must be purchased within a set time frame after booking. Many travel insurance plans offer additional coverages to travelers who protect their trip within the first 10 to 21 days after making their first trip payment

The most important first step is to figure out your coverage priorities and identify the most important criteria for your trip. For example, when Shannon O'Donnell purchased the previously-mentioned, comprehensive plan for her around-the-world trip, she sought out a policy that would cover the cost of an emergency guardian for her 11-year-old niece if anything happened to O'Donnell.

You can determine the key coverages you need by browsing a list and selecting the top two or three; use them as filtering criteria when comparing insurance quotes.

Once you've established what you need in an insurance plan, utilize a reputable comparison site such as InsureMyTrip, which includes reviews for every insurance company plan it recommends. You can select the travel details for which you need insurance, using drop-down menus on the website to receive an instant quote.

WorldNomads is one of the most popular providers among solo world travelers, endorsed by the likes of Lonely Planet and similar backpacker guides. However, you may find that AIG, Nationwide or Allianz offer more competitive prices for your bachelor cruise or family vacation to Disneyland.

How much will travel insurance cost?

Depending on the package you select, expect to pay between 4 to 8% of your total prepaid, nonrefundable trip expenses. Basic plans for peace of mind can cost less than 4%, while premium vacation plans that cover just about any conceivable issue can cost more than 12% of your total trip expenses. Travel medical insurance is sold based on the duration of your travels, and can be as low as a few dollars per day.

All reputable insurance companies will offer a "free-look period" in most states during which you can cancel your policy for a full refund of the premium (on some plans, refunds may be subject to a small administration fee). This allows you to review the policy you've selected and return it for any reason within the period allotted.

Under normal circumstances, you don't need to purchase a "cancel for any reason" policy unless you really need the flexibility — you'll overpay when most accepted reasons are plenty sufficient.

You can receive a quote and purchase a policy online in minutes with any credit card. Note that although you may assume travel insurance should count as travel and be eligible for bonus rewards on cards like the Chase Sapphire Reserve, your earnings will depend on the individual provider's merchant code. When in doubt, expect that the purchase will fall under the insurance category for earnings.

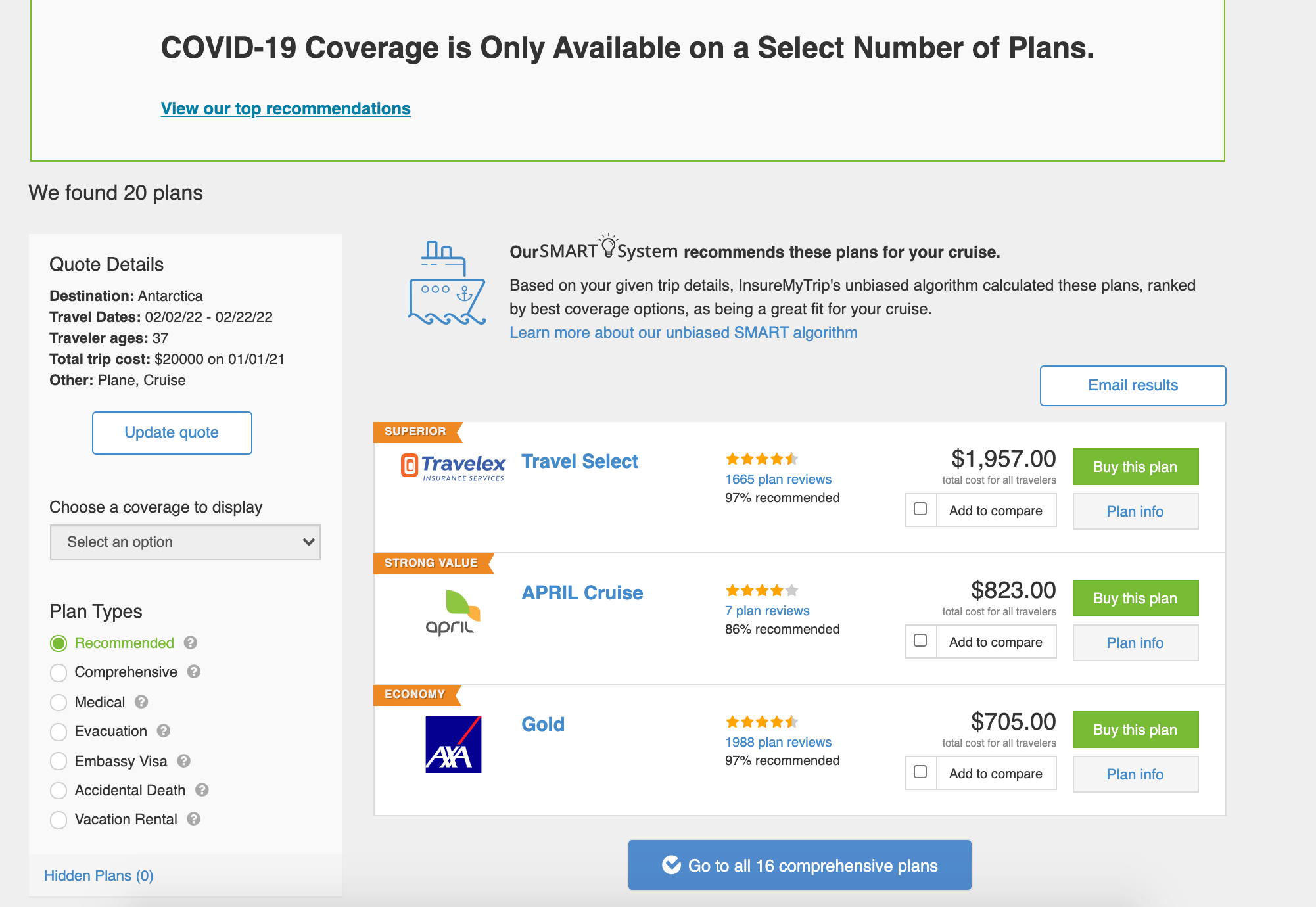

Here's a sample insurance price comparison from InsureMyTrip that I generated for my dream vacation to Antarctica, valued at a total travel cost of $20,000 (dream big, right?).

There's a drastic difference between the top three quotes I received out of 20 recommendations. InsureMyTrip.com conveniently labeled each plan for me by quality: Superior, Strong Value and Economy.

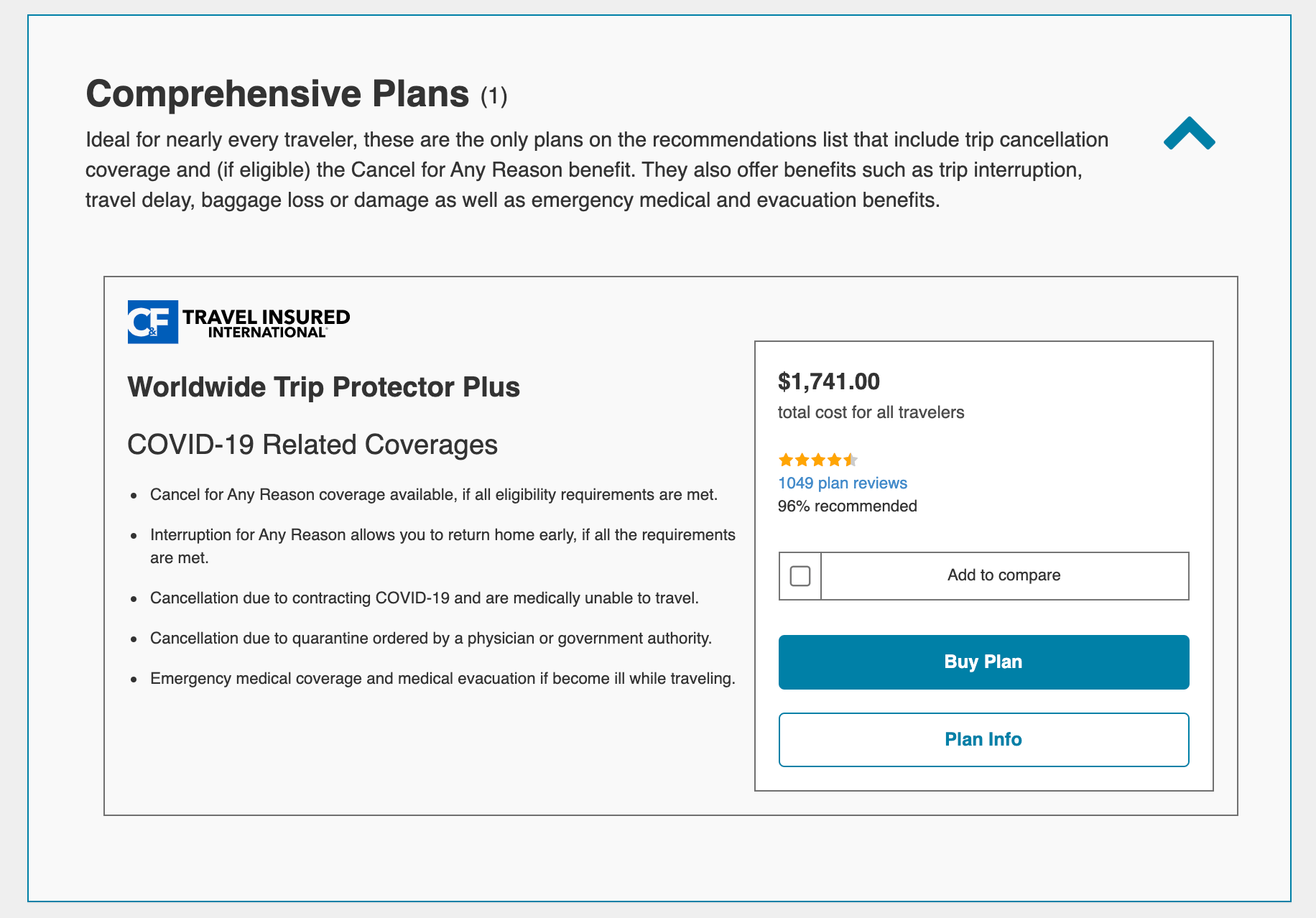

But keep in mind that if I want coverage that specifically covers COVID-related setbacks, there's only one option available through InsureMyTrip. It will set me back $1,741 — a large number, but still just 8.7% of my $20,000 hypothetical trip total.

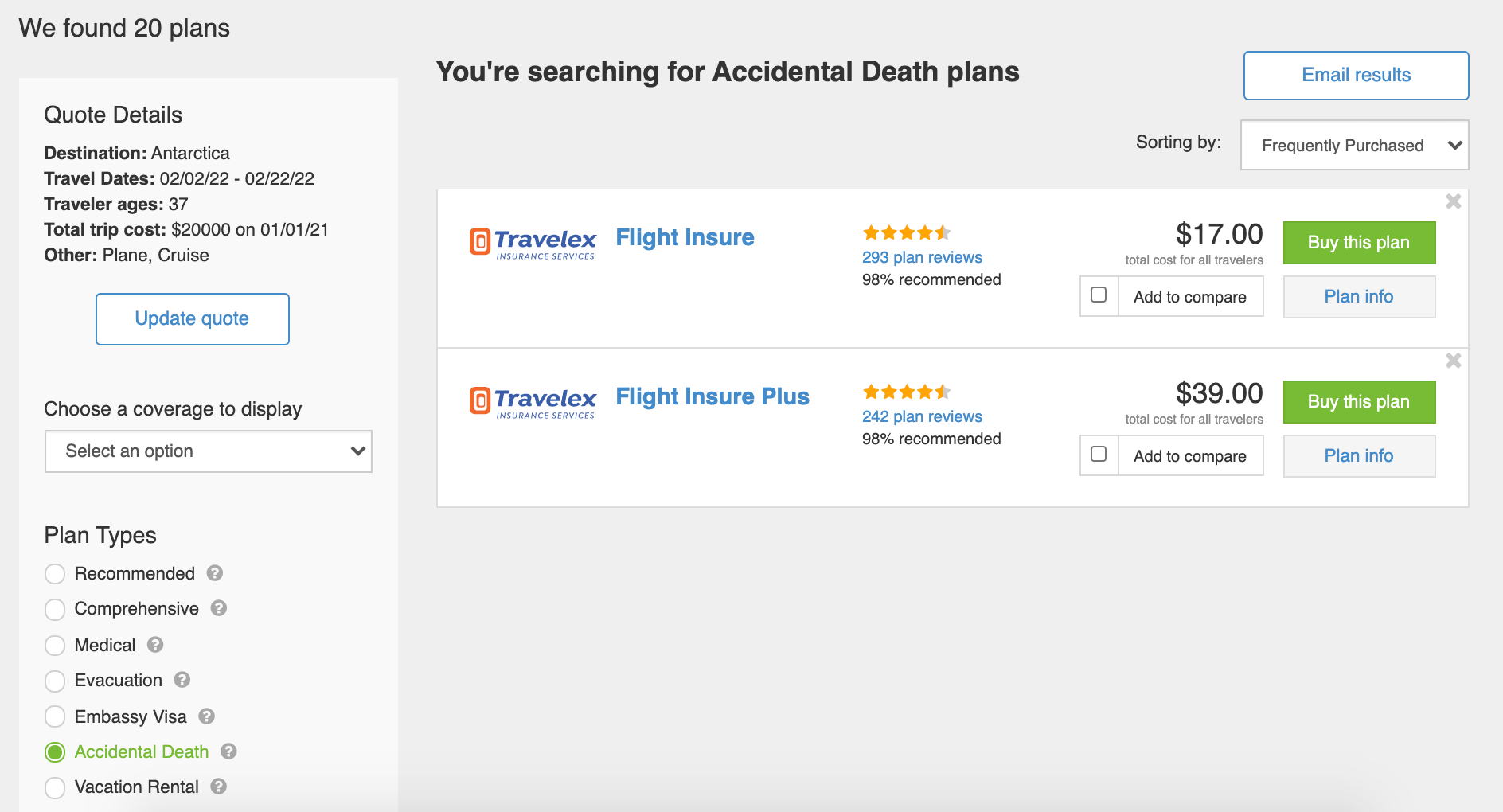

However, I could decide to only focus on the worst-case scenario instead by purchasing accidental death coverage. Unfortunately, the average funeral easily costs thousands of dollars, a sum that few families are equipped to pay on short notice.

If I opted to fly down to Antarctica, basic flight insurance for accidental death would cost me just $17 in the unlikely event that the unthinkable happened to me.

How do I make a claim?

Ideally, you'll never need to make good on your insurance investment. But if you do, here are some easy tips to keep in mind when filing a claim. Best-case scenario, you'll have your reimbursement back in hand in no time; worst-case scenario, you can avoid the disappointment of a rejected claim.

Here are a couple of the most common reasons why insurance companies might deny your claim — and how to avoid them.

You're trying to claim coverage on an activity or event that isn't covered on your plan

Make sure you read the fine print on your contract very carefully, both when you purchase your plan and when you begin filing your claim. Many plans will not offer medical coverage for injuries sustained during certain activities — like bungee jumping, for example.

You haven't filed a claim through your primary insurance yet

Third-party travel insurance may offer benefits on either a primary or secondary basis. If the coverage is primary, the travel insurance company will pay benefits for a covered claim first. If coverage is secondary, your claims adjuster will ask you to reach out to any primary source of reimbursement first before paying out any expenses — whether that's through homeowner's or medical insurance or from a travel provider that bears responsibility for a loss.

In other words, if your travel insurance policy offers secondary coverage and your luggage is stolen (for example), you'll have to file a claim with the airline or your homeowner's insurance provider first, and show proof of either denial or resolution before your travel insurance company will pay out your lost items.

Or if you get sick in the U.S. and your health insurance covers you for any domestic doctor visit, you'll have to file your insurance claim there rather than through your travel insurance company. If you incur additional expenses that aren't covered by your health insurance, such as an ambulance or medical evacuation, that's where your travel insurance may kick in.

Your documentation is incomplete or inaccurate

Hang on to your receipts! Your insurance claims adjuster will require, at minimum, all paperwork related to your property loss or medical expenses, such as a police report or hospital discharge papers. The faster you can get written proof or documentation for an issue, the quicker your claim can be processed.

It's crucial to remember that travel cancellations due to illness must be recommended by a doctor, in writing; unless you purchased a "cancel for any reason" policy, it will not be sufficient to expect reimbursement just because, say, your child developed a cough that you believe is a precursor to bronchitis.

Purchasing travel insurance after an incident has already occurred

I hate to play Captain Obvious here, but travel insurance can't be purchased after a hurricane has already been named, or after your illness has already set in. Again, this is why it's important to purchase travel insurance as soon as you've made a payment on your trip bookings.

My own success story: How a $200 travel insurance plan paid for $1,300 of expenses in Italy

My faith in travel insurance paid off when I left for a three-week trip to Italy in July 2018. Thunderstorms in Chicago delayed my inbound flight, which meant I was rerouted onto another plane with just two hours to spare. I eventually made it to Venice — but my checked luggage did not for an additional five days.

Since I was attending a photography workshop, I had packed my suitcase full of fancy dresses for our models to wear, all of which had to be replaced on the spot during the height of peak tourist season. I also ended up having to pay out of pocket for additional basics like extra socks, rain gear and alternative transportation.

Fortunately, I knew I could float my unexpected expenses on my credit cards for a few weeks. And even better, I knew that my travel insurance plan would cover additional expenses associated with my flight delay — including coverage for my alternative transportation within Venice.

While my Chase Sapphire Reserve also includes trip protection, the $500 total coverage for delayed baggage expenses wouldn't have been sufficient to cover the cost of the clothing I had to purchase for the workshop. And since I wasn't delayed for more than six hours at any single point, I also wouldn't have been able to claim credit card insurance coverage for my rebooked transportation.

Related: Which credit cards cover baggage delays?

In contrast to my credit card trip protection, my travel insurance plan covered all of my costs — every, last cent.

As Murphy's Law would have it, Lufthansa finally delivered my lost luggage to me — but not until the morning after the workshop had ended.

In total, I claimed $1,296.55 in expenses for the five and a half days I spent without my luggage, between the cost of replacement clothing, the formal dresses, a replacement suitcase to carry everything back and forth on the cobblestones of Venice, a canceled Airbnb in Florence and the rebooked water taxi. And if I hadn't been sharing an Airbnb with friends, my housing costs very well could have added to that total, since I had to stay on in Venice for a couple of extra days to wait for my bag. But my AIG insurance plan covered every penny.

The claims process was complicated and involved, and I had to save all of my Italian receipts and convert euros to U.S. dollars for every line item. But once I finally buckled down and submitted all my paperwork, I received a check within seven business days of final confirmation.

And other than all the extra luggage I ended up having to haul all over the land of pasta, all's well that ends well, right?

Bottom line

Independent travel insurance isn't for everyone — or necessary for every trip. But if you constantly find yourself on the road, or frequently book complicated travel, independent travel insurance may be just what you need to bring your peace of mind with you, everywhere you go.

I've personally experienced the benefits of having travel insurance, and so have plenty of other TPG readers and staffers. Hopefully, this guide gave you some insight into when it makes sense to purchase travel insurance and how to find the best plan for you.

Additional reporting by Madison Blancaflor, Katie Genter, Jordi Lippe-McGraw, and Squaremouth.

Disclaimer: This information is provided by IMT Services, LLC (InsureMyTrip.com), a licensed insurance producer (NPN: 5119217) and a member of the Tokio Marine HCC group of companies. IMT's services are only available in states where it is licensed to do business and the products provided through InsureMyTrip.com may not be available in all states. All insurance products are governed by the terms in the applicable insurance policy, and all related decisions (such as approval for coverage, premiums, commissions and fees) and policy obligations are the sole responsibility of the underwriting insurer. The information on this site does not create or modify any insurance policy terms in any way. For more information, please visit www.insuremytrip.com.