Got excellent credit? These are the best credit cards for you

Update: Some offers mentioned below are no longer available. View the current offers here.

You can be approved for some of the best rewards credit cards if you have a decent credit score. However, having an excellent credit score can unlock access to the most rewarding premium cards, higher credit lines and lower interest rates.

An excellent credit score is generally defined as 760 or higher.

Most of the best credit cards for consumers with excellent credit are travel credit cards that earn transferable points currencies or rewards for a specific loyalty program, but we've also included a couple of cash-back cards.

Here's what we recommend.

Best credit cards for excellent credit

With excellent credit, you have an excellent chance of approval for any credit card, so long as you follow the application rules for the various banks. These are the best credit cards for various types of spending and benefits, which we'll cover in detail below:

- American Express® Gold Card: Best for dining rewards

- Blue Cash Preferred® Card from American Express: Best cash-back card for gas, groceries, and streaming

- Capital One Venture Rewards Credit Card: Best for rewards with fixed-rate and transfer partner options

- Capital One Venture X Rewards Credit Card: Best for rewards and perks for authorized users

- Chase Sapphire Preferred® Card (see rates and fees): Best for travel rewards with a low annual fee

- Chase Sapphire Reserve® (see rates and fees): Best for travel rewards with premium travel protections

- Citi Double Cash® Card (see rates and fees): Best for everyday earning rate and balance transfers

- The Platinum Card® from American Express: Best for premium perks and benefits

The best credit cards for excellent credit

American Express® Gold Card: Best for dining rewards

Welcome bonus: Find out your offer and see if you are eligible to for high as 100,000 Membership Rewards points after spending $8,000 on eligible purchases in your first six months of card membership. Welcome offers vary and you may not be eligible for an offer.

Rewards rate: Earn 5 Membership Rewards points per dollar spent on prepaid hotels booked on amextravel.com or the Amex Travel App™, 4 points per dollar at restaurants worldwide — on up to $50,000 of these purchases per year (then 1 point per dollar), 4 points per dollar at U.S. supermarkets — on up to $25,000 of these purchases per year (then 1 point per dollar), 3 points per dollar spent on flights booked directly with the airline or booked on amextravel.com or the Amex Travel App, 2 points per dollar spent on car rentals booked on amextravel.com or the Amex Travel App and 2 points per dollar spent on cruises and other eligible purchases booked on amextravel.com and 1 point per dollar spent on all other eligible purchases.

Annual fee: $325 (see rates and fees)

Who should apply: If you want an Amex card that makes it easy to earn Membership Rewards on everyday expenses such as restaurants and groceries at U.S. supermarkets, this is definitely a card to consider. However, if you're looking for an Amex Membership Rewards card that earns bonus points on a wide variety of travel expenses, you may be better off with the American Express® Green Card.The information for the Amex Green Card has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.

For more details, check out our full card review for the Amex Gold.

Apply here: American Express® Gold Card

Blue Cash Preferred® Card from American Express: Best cash-back card for gas, groceries, and streaming

Welcome bonus: Find out your offer and see if you are eligible for as high as $300 cash back after spending $3,000 on purchases in the first six months of card membership. Welcome offers vary, and you may not be eligible for an offer. Cash Back is received in the form of Reward Dollars that can be redeemed as a statement credit or at Amazon.com checkout.

Rewards rate: Earn 6% cash back at U.S. supermarkets (on up to $6,000 annually, then 1%) and select U.S. streaming services, 3% cash back on transit and at U.S. gas stations and 1% cash back on everything else.

Annual fee: $0 intro annual fee for first year, then $95 (see rates and fees)

Who should apply: The Blue Cash Preferred Card has bonus categories that are well-aligned with many consumers. With many people spending a decent amount on streaming services, earning 6% in this relatively rare bonus category can provide solid value. Plus, you can earn $360 back on purchases at U.S. supermarkets each year if you reach the $6,000 spending cap; afterward, you will earn 1% back on these purchases.

You'll also earn 3% cash back on commuting expenses involving gas and transit (which includes taxis, ride-shares, tolls, trains, buses and more). Although the card does not earn Membership Rewards points, it provides a simple way to earn rewards on common everyday spending categories.

Cash back is received in the form of Reward Dollars that can be redeemed as a statement credit and at Amazon.com checkout.

For more details, check out our full card review for the Blue Cash Preferred.

Apply here: Blue Cash Preferred® Card from American Express

Capital One Venture Rewards Credit Card: Best for rewards with fixed-rate and transfer partner options

Welcome bonus: Earn 75,000 bonus miles when you spend $4,000 on purchases in the first three months from account opening.

Rewards rate: Earn 5 miles per dollar spent on hotels, vacation rentals, and car rentals booked through Capital One Travel and 2 miles per dollar on other purchases. TPG's September 2024 valuations place Capital One miles at 1.85 cents apiece.

Annual fee: $95

Who should apply: The Capital One Venture is a great card if you're looking for simplicity and flexible redemptions. You know you're getting at least 2 miles per dollar on every purchase, so you don't need to worry about how a purchase will code. The miles you earn can then be used to reimburse eligible travel purchases from your credit card bill or they can be transferred to one of Capital One's transfer partners. As an added perk, you'll also get a statement credit of up to $120 every four years for your Global Entry or TSA PreCheck® application fee, which isn't a benefit commonly found on low-fee cards.

This card is often marketed as a beginner card, but anyone can take advantage of the card's rewards structure and benefits. Beginners often enjoy the simplicity of using the Venture, but experts can utilize it as a great card for non-bonus spending. TPG's founder, Brian Kelly, even said the Capital One Venture was the one card he'd keep if he could only keep one card.

For more details, check out our full card review for the Capital One Venture.

Learn more: Capital One Venture Rewards Credit Card

Capital One Venture X Rewards Credit Card: Best for rewards and perks for authorized users

Welcome bonus: Earn 75,000 bonus miles after spending $4,000 on purchases in the first three months from account opening.

Rewards rate: Earn 10 miles per dollar on hotels and car rentals booked via Capital One Travel, 5 miles per dollar on flights and vacation rentals booked via Capital One Travel and 2 miles per dollar on other purchases. TPG's September 2024 valuations put Capital One miles at 1.85 cents apiece.

Annual fee: $395

Who should apply: The Venture X card has the same welcome offer and earns the same type of Capital One miles as the Venture card. The difference comes in the annual fee ($395, instead of $95) and the plethora of perks added to the Venture X. Along with reimbursement for your Global Entry or TSA PreCheck application fee, you can enjoy a $300 annual travel credit with Capital One Travel and 10,000 bonus miles on your account anniversary.

The real benefits come with adding several authorized users on the account, as they will enjoy these perks that aren't reserved just for the primary account holder: complimentary access to Capital One lounges and Priority Pass™ lounges and complimentary Hertz President's Circle status*.

*Upon enrollment, accessible through the Capital One website or mobile app, eligible cardholders will remain at that status level through the duration of the offer. Please note, enrolling through the normal Hertz Gold Plus Rewards enrollment process (e.g. at Hertz.com) will not automatically detect a cardholder as being eligible for the program and cardholders will not be automatically upgraded to the applicable status tier. Additional terms apply

For more details, check out our full card review for the Capital One Venture X.

Learn more: Capital One Venture X Rewards Credit Card

Chase Sapphire Preferred Card: Best for travel rewards with a low annual fee

Welcome bonus: Earn 100,000 bonus points after spending $5,000 on purchases in the first three months from account opening.

Rewards rate: Earn 5 points per dollar on travel booked through Chase Travel℠, 5 points per dollar spent on Lyft purchases (through Sept. 2027), 5 points per dollar spent on Peloton equipment and accessory purchases of $150 or more (through Dec. 2027, with a limit of 25,000 bonus points), 3 points per dollar spent on dining, including eligible delivery services, takeout and dining out, 3 points per dollar spent on select streaming services, 3 points per dollar spent on online grocery purchases (excluding Target®, Walmart® and wholesale clubs), 3 points per dollar spent on vacation homes, 3 points per dollar spent on gas & EV charging, 2 points per dollar spent on all other travel and 1 point per dollar spent on all other purchases.

Annual fee: $95

Who should apply: The Chase Sapphire Preferred is one of the best beginner travel cards available. Plus, it offers a welcome offer worth $2,050 based on TPG's June 2026 valuations. The Chase Sapphire Preferred earns Chase Ultimate Rewards points, which you can redeem for up to 1.75 cents each (depending on the specific redemption) through the Chase Ultimate Rewards portal (see your rewards program agreement for full details). Or, you can transfer your points to one of Chase's airline or hotel partners and then redeem through these programs.

If you're looking for a solid travel rewards card with travel protections but can't quite justify the $795 annual fee on the Chase Sapphire Reserve, the Chase Sapphire Preferred is a great option.

For more details, check out our full card review for the Chase Sapphire Preferred.

Apply here: Chase Sapphire Preferred

Chase Sapphire Reserve: Best for travel rewards with premium travel protections

Welcome bonus: Earn 100,000 bonus points after spending $6,000 on purchases in the first three months from account opening.

Rewards rate: Earn 8 points per dollar on purchases through Chase Travel, 5 points per dollar on Lyft rides through Sept. 30, 2027, 4 points per dollar on flights and hotels purchased direct, 3 points per dollar on dining purchases worldwide and 1 point per dollar on everything else.

Annual fee: $795

Who should apply: The Chase Sapphire Reserve is one of the top premium travel rewards cards available. Although recent changes to the card have upset some cardholders, the card remains a staple in many wallets due to strong earning rates on travel and its top-shelf travel protections.

The Chase Sapphire Reserve earns valuable Chase Ultimate Rewards points and offers perks including an annual $300 travel credit, Priority Pass lounge access, a TSA PreCheck/Global Entry application fee credit every four years, at least one complimentary year of DashPass membership through DoorDash (activate by Dec. 31, 2027) and an impressive array of travel protections. All of these perks and benefits make the Chase Sapphire Reserve a great option for frequent travelers. But, if you can't quite justify the $795 annual fee, you may find that the Chase Sapphire Preferred Card is a better fit.

For more details, check out our full card review for the Chase Sapphire Reserve.

Apply here: Chase Sapphire Reserve

Citi Double Cash Card: Best for everyday earning rate and balance transfers

Welcome bonus: Earn $200 cash back after spending $1,500 in the first six months of account opening.

Rewards rate: Earn 2% back on all purchases — 1% back when you buy purchases and 1% back when paying your bill.

Annual fee: $0

Who should apply: Those looking for a great card for everyday spending — or even those who don't want to deal with bonus categories — will love this card. Double Cash rewards are earned as ThankYou points that you can redeem for cash at 1 cent each or use with limited transfer options: just Choice Privileges, JetBlue TrueBlue and Wyndham Rewards. If you're in the market for a simple card that earns flexible rewards, however, it doesn't get much better than the Citi Double Cash.

For more details, check out our full card review for the Citi Double Cash.

Apply here: Citi Double Cash Card

The Platinum Card from American Express: Best for premium perks and benefits

Welcome bonus: Find out your offer and see if you are eligible for as high as 175,000 Membership Rewards Points after spending $12,000 on purchases within the first six months of card membership. Welcome offers vary and you may not be eligible for an offer.

Rewards rate: Earn 5 points per dollar on airfare purchased directly from airlines or with American Express Travel® (on up to $500,000 of airfare purchases per calendar year), 5 points per dollar on prepaid hotels booked with Amex Travel and 1 point per dollar on other purchases. TPG's September 2024 valuations place American Express Membership Rewards at 2 cents apiece.

Annual fee: $895 (see rates and fees)

Who should apply: Although the welcome bonus can provide significant value — and earning 5 points per dollar on select airfare and hotel expenses is nice — The Platinum Card from American Express is a card that you keep for its benefits and perks. You can earn up to $200 in airline fee statement credits*, up to $200 in Uber Cash (up to $15 each month and a bonus up to $20 in December for Uber rides and Uber Eats orders in the U.S. after adding your Amex Plat to your Uber account and redeeming with any Amex card), along with an annual up to a $120 statement credit that fully covers an auto-renewing $96 annual or $9.99 monthly membership. Plus, you'll get access to Centurion Lounges, Delta Sky Clubs** when flying Delta, Priority Pass lounges and many more lounges through Amex's Global Lounge Collection for eligible card members. Enrollment is required for select benefits.

You'll also get automatic Marriott Gold status and Hilton Gold status (enrollment required). Plus, you can book exceptional hotel stays at select properties through Amex's Fine Hotels and Resorts program. And, you can add authorized users for just $195 each per year (see rates and fees). In terms of redeeming, the American Express Membership Rewards program has many airline and hotel partners to which you can transfer your reward points.

For more details, check out our full card review for The Platinum Card from American Express.

*Enrollment required for select benefits.

**Eligible Platinum Card Members will receive 10 Visits per Eligible Platinum Card per year to the Delta Sky Club or to Grab and Go when traveling on a same-day Delta-operated flight.

Apply here: The Platinum Card® from American Express

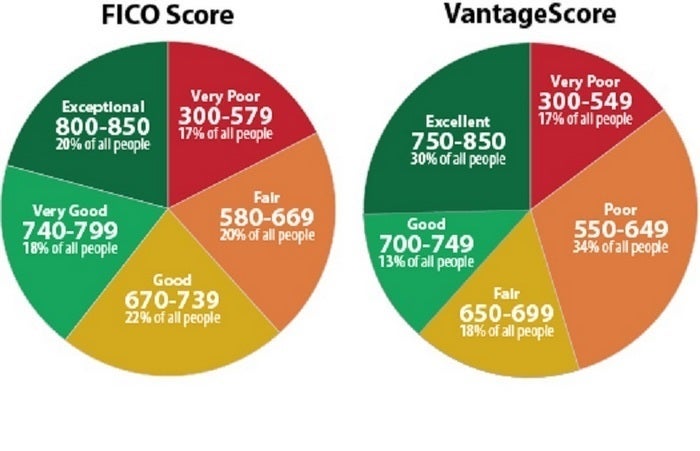

What is an excellent credit score?

FICO Score and VantageScore credit scores range from 300 to 850. An excellent credit score is generally considered to be a score that is 760 and above.* With a credit score in this range, you should be able to get accepted for most of the best rewards cards on the market.

Related: How to check your credit score for free

*The Points Guy credit ranges are derived from FICO® Score 8, which is one of many different types of credit scores. If you apply for a credit card, the lender may use a different credit score when considering your application for credit.

But, it's important to realize that you don't have just one credit score. There are three main credit reporting agencies (Experian, Equifax and TransUnion) as well as two primary methods for calculating credit scores (FICO Score and VantageScore). So, you'll likely have slightly different credit scores from one credit reporting agency to another.

For more details, see our guide to how credit scores work.

Related: Why your credit score may be different depending where you look

What credit cards are only available if you have excellent credit?

There are two types of cards that are generally only available if you have very good or excellent credit:

Amex cards with no preset spending limits

These cards aren't actually credit cards. Amex cards like The Platinum Card® from American Express and the American Express® Gold Card don't come with a credit limit or preset spending limit like you're used to with credit cards. Instead, purchases are approved on a case-by-case basis and the amount you can spend adapts based on factors like your purchase, payment and credit history.

This means that, in the wrong hands, they could be very dangerous. Someone could spend tens of thousands of dollars on these cards before Amex caught on and started declining the charges. To stop this from happening, Amex will generally only approve applicants with excellent credit.

Related: Choosing the best American Express credit card for you

Premium credit cards

Even if they come with a fixed spending limit, you can expect to face stricter approval requirements for the ever-growing list of premium credit cards. These cards offer valuable perks and are generally marketed toward higher spenders who, in turn, need a larger credit limit. To be trusted with high spending capabilities, these cards typically require you to have a high credit score.

Related: Why a $500+ per year credit card isn't crazy

Tips to maintain excellent credit

FICO and VantageScore scores are designed to predict the likelihood that you will become 90 days late on any of your credit obligations within the next 24 months. So, in short, to maintain excellent credit you should avoid moves that may increase the perceived likelihood that you will become less financially stable during the next two years. But, you don't need to work toward a perfect 850 score.

To maintain excellent credit, you should generally continue to pay your bills on time, keep your debt-to-credit ratio low, avoid closing any accounts you've kept open for a long time and avoid opening an excessive amount of new accounts within a short period. If you're looking to maintain your excellent credit, you should also check your credit score regularly.

Related reading: 8 biggest factors that impact your credit score

Bottom line

Having excellent credit can help you be approved for some of the best premium rewards credit cards, but excellent credit can also unlock various other benefits. For example, higher credit scores can often help you to qualify for lower interest rates on your mortgage.

That's just one more reason why we at TPG believe your credit history is of the utmost importance. And if you look after it well, you'll be well on your way to one of the cards listed above.

Related: How much money can good credit really save you?

For rates and fees of the Amex Platinum card, click here.

For rates and fees of the Amex Gold card, click here.

For rates and fees of the Blue Cash Preferred, click here.