Clearing up confusion: Why your credit score may be different depending where you look

Keeping track of your credit score is important. Before you apply for a credit card, car loan or other type of credit, you likely want to know your score.

But with all of the sites offering credit scores these days, which ones can you trust?

As you'll see, some scores might make your heart stop.

Let's go through the types of credit scores. I'll explain why they can look so different, along with where you can get your scores for free.

Your bank likely offers free credit monitoring services

If you aren't yet aware of it, know that your bank likely offers free credit monitoring services. Some of these are nothing more than alerts when certain things happen, such as new credit inquiries or new accounts appearing on your report.

Other services may be more robust. These can include daily or weekly emails updating you on any changes to your credit report or credit score, tips on how to improve your score and even a credit score available for your viewing. It might even include searching for your personal information being sold online.

If your bank provides a service with a free credit score, be sure to check what this score is and how it's composed, though, to understand what you are seeing.

Related: How to check your credit score for absolutely free

Understanding the different types of scores

Not all credit score systems are created equal. Let's look at an example before talking about the types of scores.

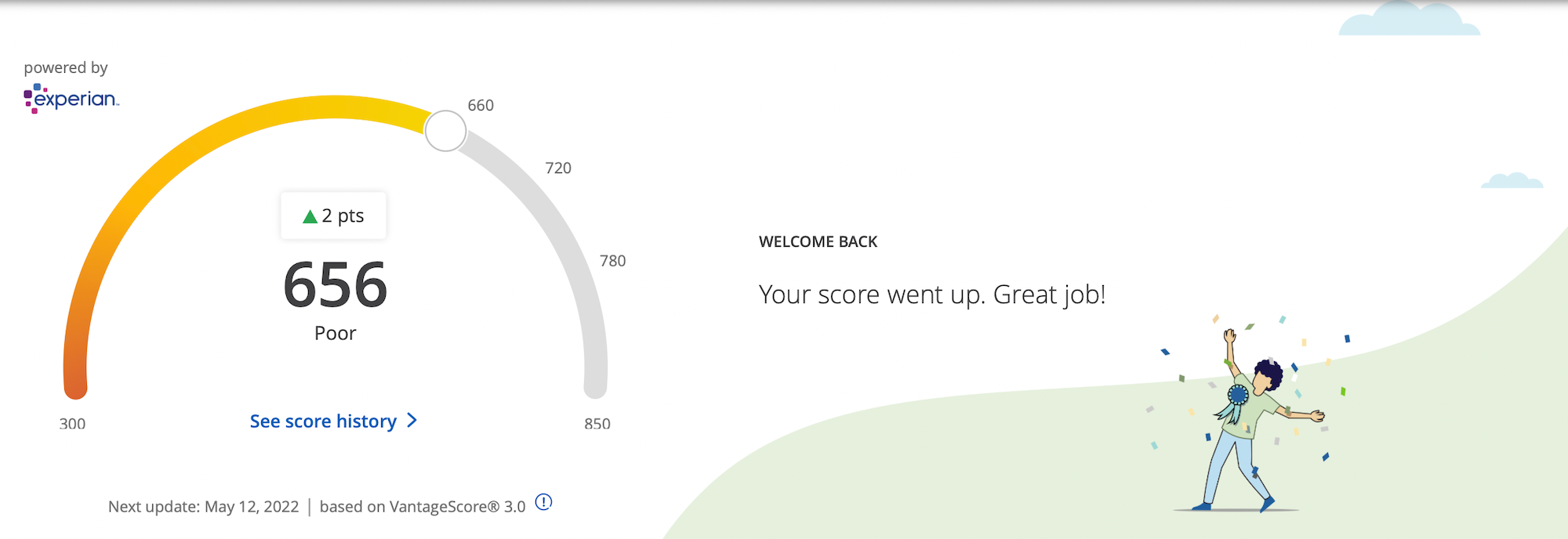

Last week, The Points Guy himself, Brian Kelly, had quite a shock when Chase Credit Journey showed him a "Poor" score of 656.

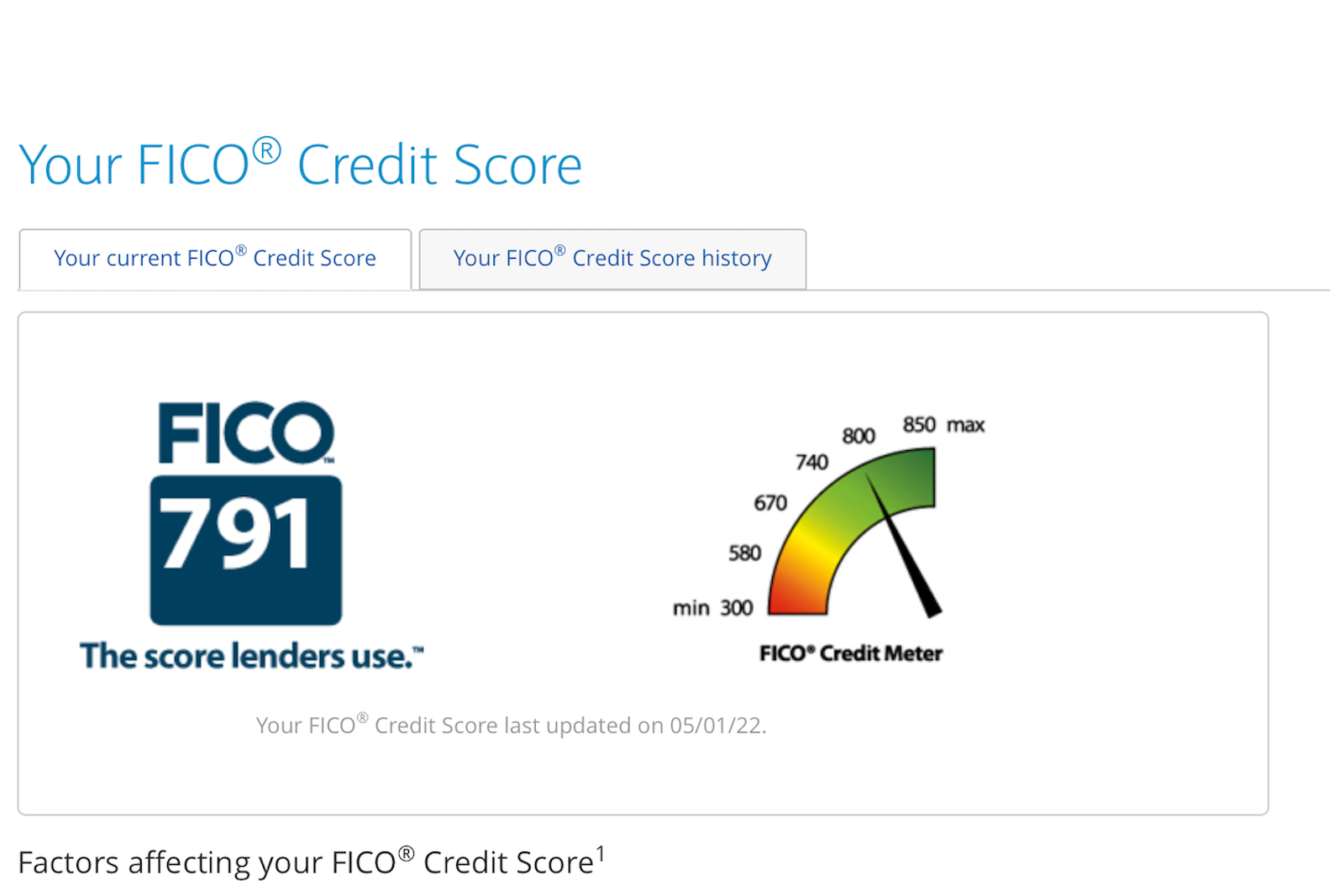

He immediately checked his score from his Barclays account. The score of 791 was 135 points higher than what Chase showed and more in line with what he expected to see.

So what's the difference? Barclays uses a FICO score — the score most lenders use. Chase Credit Journey uses VantageScore 3.0® by Experian. While it's a product from one of the three main credit agencies in the U.S. (the other two are TransUnion and Equifax), it's not the same as a FICO score, which is what lenders use when they pull your credit report.

As you will see, some estimates are better than others.

Moreover, the credit agency your score comes from will make a difference. Usually, your score won't be exactly the same from all three agencies because the information each agency has access to may vary. For example, if you applied for a card with an issuer that only reported your application to TransUnion — but not Equifax or Experian — that may result in different scores.

Sample score using FICO

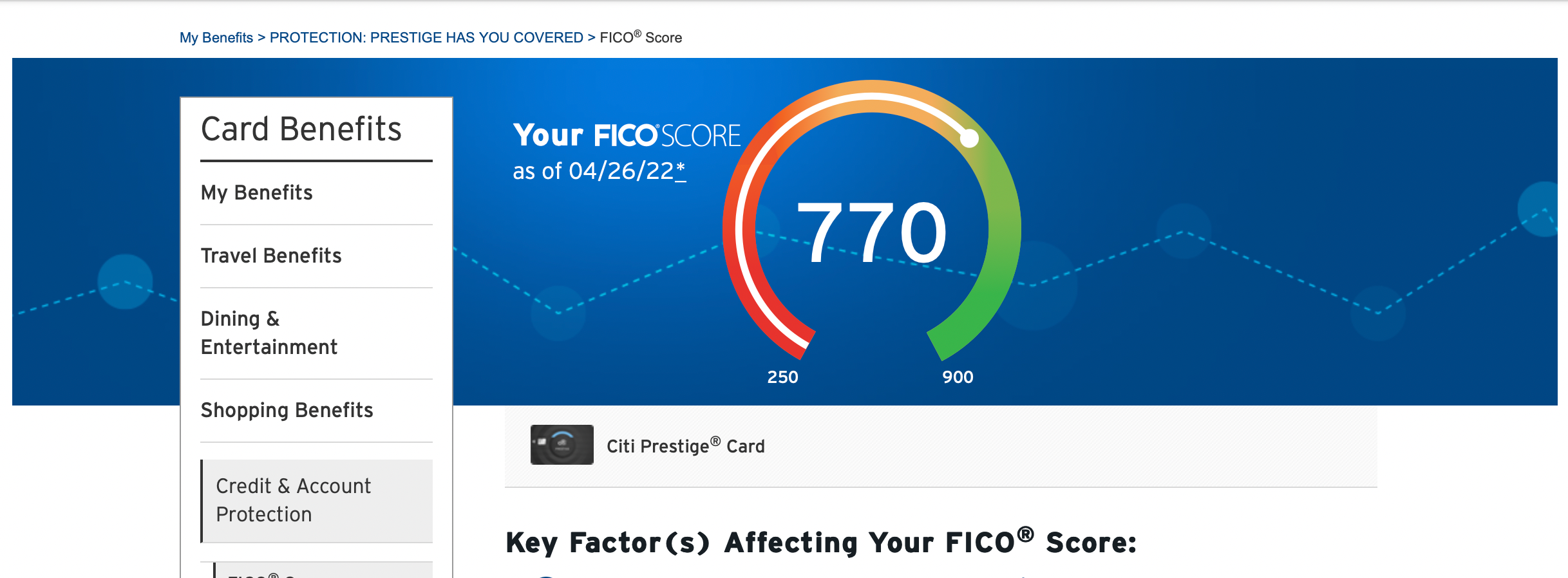

Citi also uses a FICO-based score, though you'll notice a difference in the score compared to what Barclays showed. Citi's score of 770 is 21 points lower, and it last updated 5 days prior to Barclays' update. Checking when your score was updated can make a difference due to what may have happened in that time. Perhaps a credit card statement with a large balance posted, or maybe you had a new inquiry on your credit report after applying for credit.

You can get a free FICO-based score from Barclays, Citi, Discover, Experian and Wells Fargo.

Related: Your FICO score and which credit issuers offer it for free

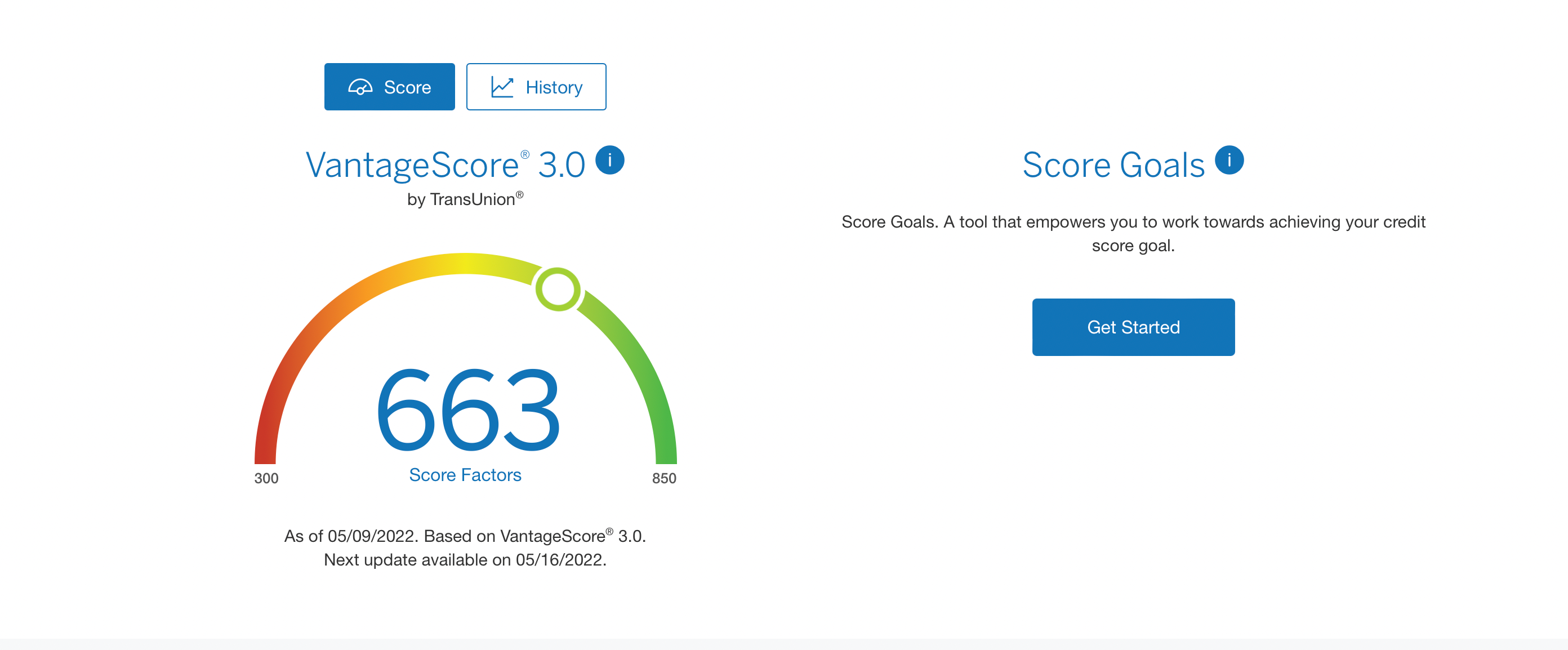

Sample scores using VantageScore

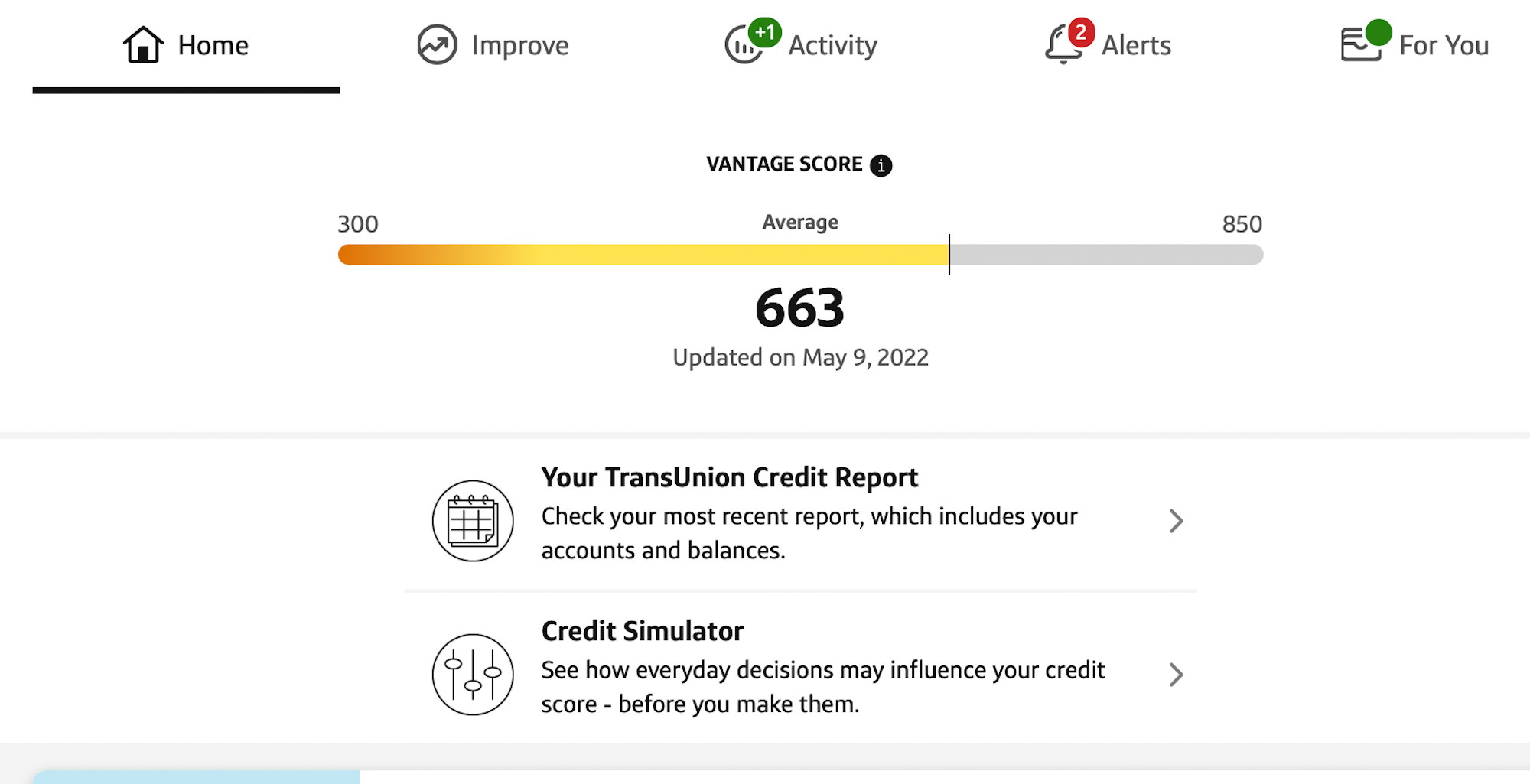

Brian's scores of 663 from both Capital One and American Express — which were calculated using VantageScore 3.0 — are also more than 100 points lower than the FICO score from Barclays.

You can get a free VantageScore from numerous places, including Bankrate.com, Capital One, Chase, Credit.com, Credit Karma, Credit Sesame, Mint and USAA.

Differences between FICO and VantageScore

Credit Karma, which uses VantageScore 3.0, has a full page explaining the differences in the scoring models.

The key takeaway is this: Roughly 90% of lenders in the U.S. continue to use your FICO score (though an industry-specific version for that specific type of credit), and the way your score is calculated between FICO and VantageScore is not the same. The information they use and the weight assigned to each item is different in these scoring models.

Monitoring your score for changes can be useful, as long as you understand that the two score types likely won't ever match.

In Brian's experience, scores based on VantageScore are 100 points lower than FICO-based scores, which are what lenders tend to use. This is because the scores are composed in a different way.

However, not everyone will experience such large differences between their FICO and VantageScore numbers. My VantageScore number is 41 points lower than my FICO score -- still lower, but a less drastic difference than what Brian saw.

Do these score differences matter? It depends. Technically, the only score that really matters will be the score a lender sees when deciding whether to extend credit to you. However, seeing a large change in your credit score may be an indication of something else — missed payments, outstanding balances, an unauthorized person applying for credit in your name, etc. — that needs your attention.

Seeing such a huge difference in score from one site to another can be confusing, so what should you do?

How to make sure you see an accurate credit score

If you just want to see how many recent inquiries you have or other data, any of the models can likely provide this. If the score number is what's important to you, look for a site offering a FICO score. This will more closely mirror what a lender sees, since the vast majority of lenders in the U.S. still use FICO scores in credit decisions.

Second, look at the date or "last updated" reference on the score in front of you. What's happened between then and now? The more recent the score's data, the more accurate it is. If multiple credit card billing statements, mortgage payments and other financial data have updated between then and now, the score won't be worth much. Given that I have credit cards with numerous banks, I receive emails every few days telling me that my score updated. This comes from a statement closing or a payment notification appearing on my credit report.

Third, consider getting your credit report from each of the three major credit bureaus (Experian, Equifax and TransUnion). As the information on your reports directly impacts your credit score, it can be beneficial to check the reports and make sure everything is correct. By law, you are entitled to a full credit report from each bureau once a year for free. To get your full reports, head on over to the annual credit report site and click the "Request your free credit reports" button.

Even better: Due to the COVID-19 pandemic, you can obtain these three reports for free once a week until further notice.

The annual credit report site does not include credit scores with your reports, but you can check each report for inaccuracies to ensure your score will be based only on correct information.

Bottom line

Staying on top of your credit report is important. There's no harm to checking your own score, either. However, seeing scores that are wildly different can produce some confusion -- as well as some shock.

Hopefully, you now understand why your scores look different, depending on what type of score you're looking at and the different way scores are composed. We looked at scores from VantageScore and FICO (the type used by the vast majority of lenders); since their scores are built in different ways, it can sometimes lead to big differences in the scores you see. The number that matters most will be the one a lender sees during your application, which you can't see in advance. It's ultimately up to you to decide how helpful these score estimates are as you monitor your own credit profile.

To read more about your credit score and how to improve it, see the following resources:

TPG featured card

at American Express's secure site

Terms & restrictions apply. See rates & fees.

| 4X | Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 4X | Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 5X | New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App. |

| 3X | Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines. |

| 2X | Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com. |

| 1X | Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases. |

Pros

- Valuable dining and food-related credits

- Flexible rewards with airline and hotel transfer partners

- Multiple travel and purchase protections

- No foreign transaction fees

- Access to Amex Offers for additional savings (enrollment required)

Cons

- Not as useful for those living outside the U.S.

- Some may have trouble using Uber and other dining credits

- You may be eligible for as high as 100,000 Membership Rewards® Points after you spend $8,000 in eligible purchases on your new Card in your first 6 months of Card Membership. Welcome offers vary and you may not be eligible for an offer. Apply to know if you’re approved and find out your exact welcome offer amount – all with no credit score impact. If you’re approved and choose to accept the Card, your score may be impacted.

- Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year.

- Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year.

- New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App.

- Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines.

- Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com.

- Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases.

- Pay It® lets you tap in the American Express® App to quickly pay for small purchase amounts throughout the month and still earn rewards the way you usually do. Plan It® gives you the option to split up big purchases into equal monthly payments with a fixed fee. You’ll know upfront exactly how much you’ll pay.

- Updated! $120 Dining Credit: Earn up to a total of $10 in statement credits monthly when you pay with the Gold Card at Grubhub (including Seamless), Buffalo Wild Wings, Five Guys, The Cheesecake Factory, and Wonder. This can be an annual savings of up to $120. Enrollment required.

- $100 Resy Credit: Get up to $100 in statement credits each calendar year at over 10,000 qualifying U.S. Resy restaurants after you pay for eligible purchases with the American Express® Gold Card. That’s up to $50 in statement credits semi-annually. Enrollment required.

- $84 Dunkin' Credit: Earn up to $7 in monthly statement credits after you pay with the American Express® Gold Card at U.S. Dunkin’ locations. Enrollment required.

- $120 Uber Cash on Gold: Enjoy up to $120 in Uber Cash annually with your Gold Card. Just add your Card to your Uber account and you'll get $10 in Uber Cash each month to use on orders and rides in the U.S. when you select an Amex Card for your transaction.

- New! As an American Express® Gold Card Member, you can enjoy complimentary Hertz Five Star® Status. Enjoy benefits like skipping the counter at select locations, adding an additional driver at no additional cost*, and vehicle upgrades**. Benefit enrollment and Hertz Gold+ registration are required. *Additional drivers must meet standard rental qualifications and must be a spouse or domestic partner to qualify as complimentary. Other additional drivers subject to fees. **Benefits are subject to availability and vary by location. Additional Hertz program Terms and Conditions including age restrictions apply.

- Take advantage of a $100 credit towards eligible charges* at over 1,300 upscale hotels worldwide when you book The Hotel Collection through AmexTravel.com or the Amex Travel App **. *Eligible charges vary by property. **The Hotel Collection requires a two-night minimum stay.

- Book your travel through the Amex Travel App with added peace of mind – backed by American Express® service and support. Only for American Express® Card Members.

- Whenever you need us, we're here. Our Member Services team will ensure you are taken care of. From lost Card replacement to statement questions, we are available to help 24/7.

- No Foreign Transaction Fees.

- Annual Fee is $325.

- Terms Apply.