Everything you need to know about credit card merchant offers

Update: Some offers mentioned below are no longer available. View the current offers here.

Remember extreme couponing? Avid couponers would pour over weekly ads and find ways to maximize their savings by stacking coupons on top of other offers.

Merchant offers are a more convenient version of couponing. These programs are entirely online and allow you to save money on the things you're buying anyway, with no scissors required.

Every issuer's merchant offer follows the same basic structure: Log into your card account online or through your banking app, review the offers available to you, add the ones you want and make a qualifying purchase using the card the offer is registered to.

Offers are typically targeted, but someone with multiple cards will have access to dozens of offers from various retailers at any given time. Though every little bit helps, some programs are more valuable than others. Here's how the programs stack up.

Amex Offers

Nearly everyone with an Amex card is familiar with Amex Offers, where you'll often find 100 or more potential discounts for each card you have. Not all of them will be relevant to your purchasing needs, but the law of large numbers says a few will probably make sense.

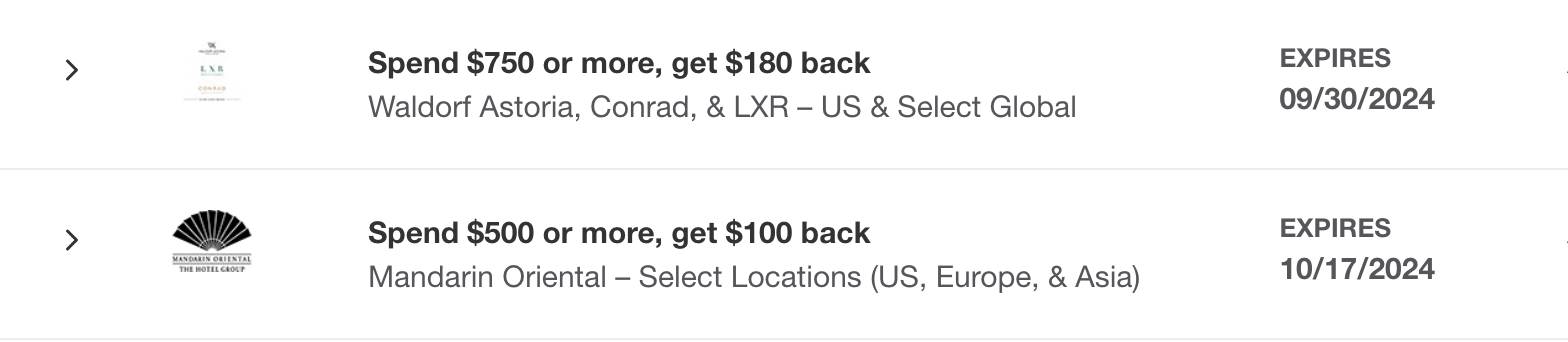

From a traveler's perspective, Amex Offers are frequently a good fit. Hotel offers are relatively common and often span multiple brands. For instance, here's one that can save you $180 on select luxury Hilton properties or $100 at select Mandarin Oriental properties:

In addition to the sheer quantity of offers available, Amex also tends to field some of the highest cash-back deals. Rebates of $100 or more are relatively common, and you can sometimes stack Amex Offers with other discounts and promotions as long as your final purchase price is high enough to trigger the deal.

Another great advantage to these offers is that Membership Rewards-earning cards sometimes proffer bonus points on eligible purchases rather than cash back. For example, you may find an offer for 10,000 bonus points instead of $100 or 5 extra bonus points per dollar instead of 5% cash back on certain types of purchases or from specific retailers.

Since TPG's July 2024 valuations peg Membership Rewards points at 2 cents each, earning your rebate in points can make it an even sweeter deal.

One major downside is that Amex usually structures deals to require a minimum spending amount (as you might imagine, the higher rebates require higher spending to qualify), and taxes and fees are generally not included in that amount. So, if you spend even just one penny short of the amount stated in your Amex Offer, you could miss out on the deal entirely.

Further, note that some Amex Offers have restrictions around what purchases are eligible, so read through the terms and conditions before you make a purchase. Also, note that you can only add a particular Amex Offer to one Amex card, so try adding it to the card that earns the most points on your purchase.

Another tip — check your Amex app if some of your added offers aren't showing up in a web browser. We've heard reports of some people thinking they had lost their offers only to find them neatly listed in the app.

Interested in using Amex Offers? Consider applying for one of these Amex cards:

- American Express® Green Card: Earn 40,000 Membership Rewards points after spending $3,000 on purchases in the first six months of card membership. Earn 3 points per dollar on dining at restaurants, travel and transit (including flights, hotels, cruises, taxis, tours and more) purchases and 1 point per dollar on other purchases ($150 annual fee.)

- American Express® Gold Card: Find out your offer and see if you are eligible for as high as 100,000 Membership Rewards points after spending $8,000 on eligible purchases in your first six months of card membership. Welcome offers vary and you may not be eligible for an offer. Earn 5 points per dollar spent on prepaid hotels booked on amextravel.com or the Amex Travel App™, 4 points per dollar at restaurants worldwide (up to $50,000 in purchases per calendar year, then 1 point per dollar) and at U.S. supermarkets (up to $25,000 in purchases per calendar year, then 1 point per dollar), 3 points per dollar spent on flights booked directly with the airline, amextravel.com or the Amex Travel App, 2 points per dollar spent on car rentals booked through amextravel.com or the Amex Travel App, and on cruises booked through amextravel.com, and 1 point per dollar spent on other eligible purchases ($325 annual fee; see rates and fees).

- The Platinum Card® from American Express: Find out your offer and see if you are eligible for as high as 175,000 Membership Rewards Points after spending $12,000 on purchases within the first six months of cardmembership. Welcome offers vary and you may not be eligible for an offer. Earn 5 points per dollar on airfare purchased directly from airlines or through American Express Travel® (on up to $500,000 on these purchases per calendar year, then 1 point per dollar), 5 points per dollar on prepaid hotels booked with American Express Travel and Amex Fine Hotels + Resorts and 1 point per dollar on other purchases ($895 annual fee; see rates and fees).

The information for the American Express Green Card has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.

Related: These Amex Offers will help you save money and make life easier right now

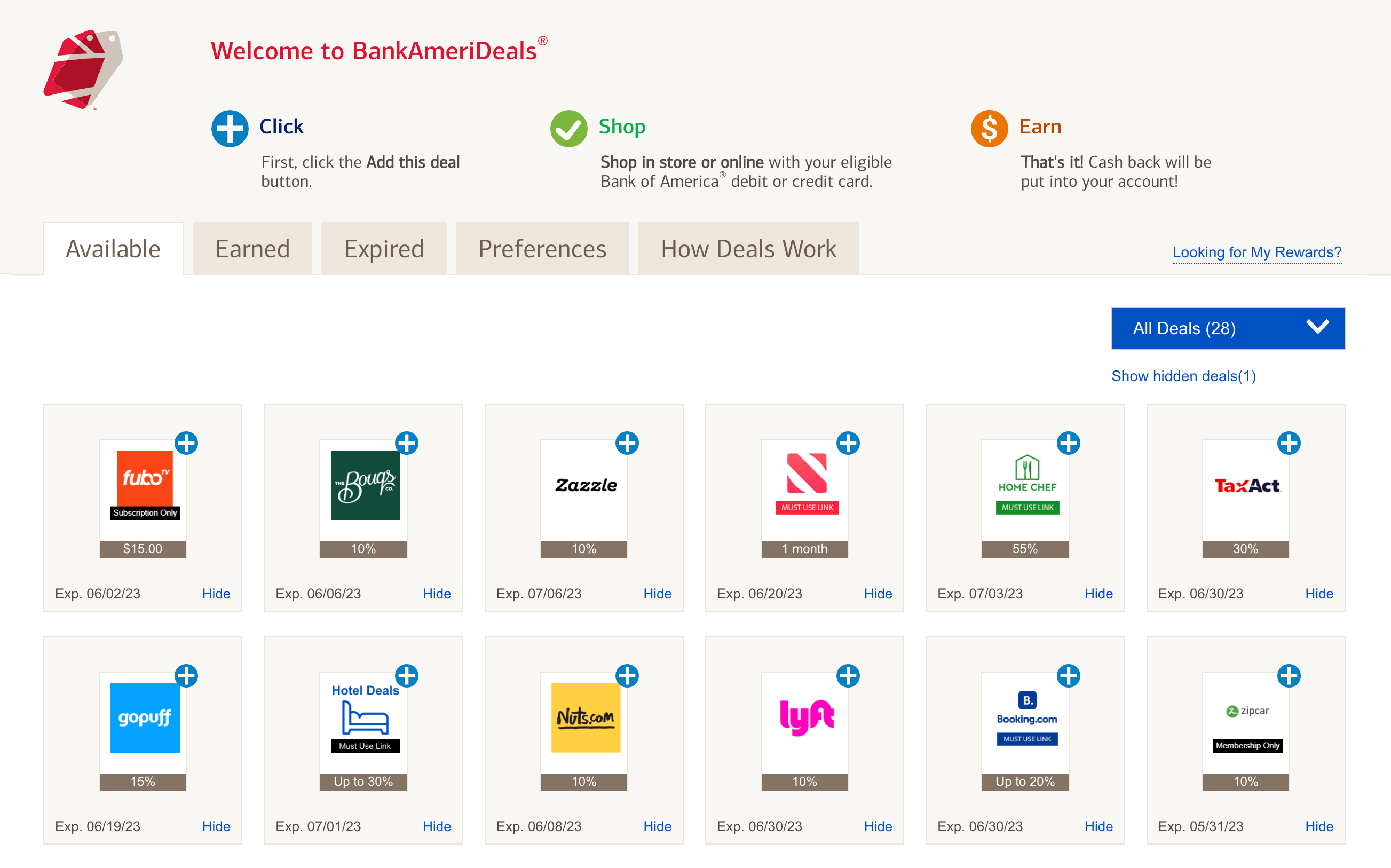

BankAmeriDeals

Bank of America also has a cash-back program with a great extra twist: Bank of America debit cards can also activate offers on their account (though we at TPG think credit cards are usually the smarter choice for most). Either way, it can take up to 30 days to see offers on your account after enrolling, so you'll need to be patient before you can start saving.

The offers on your Bank of America cards may overlap with your Chase Offers since the same backend system seemingly powers both programs. Bank of America does have an extra way to save through their BankAmeriDeals.

Note that these bonuses post to your account later than the initial earnings — but they can be a nice bonus if you regularly use your Bank of America credit card.

Related: How to maximize your earning with the Bank of America Premium Rewards card

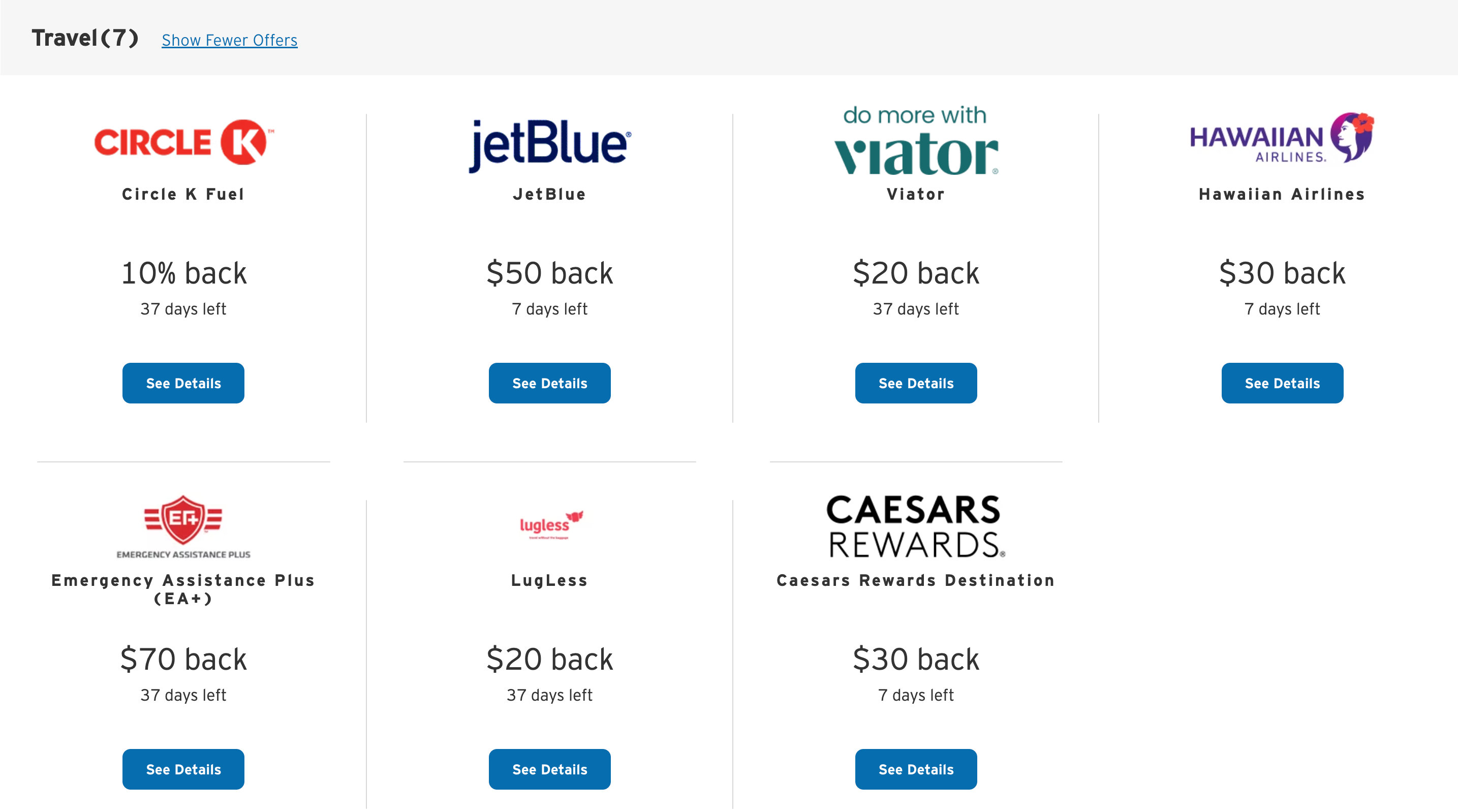

Chase Offers

Since so many of our favorite travel cards are issued by Chase, there's a good chance you have access to Chase Offers in your wallet.

Chase Offers are targeted and may vary by card. You'll need to check each card in your account to see which ones you can access. Sometimes, you'll find the best deals on cards you rarely use, which might give you an incentive to pull them out of the sock drawer.

Chase Offers are nearly always a percentage back instead of a flat rate dollar amount, with a few exceptions for subscription-based products. That makes these offers easier to use since you can spend normally without worrying about hitting a minimum threshold in your shopping cart. Everyday brands (rather than stores you've never heard of) are often featured, with recent offers from places like Starbucks, McDonald's and Best Buy.

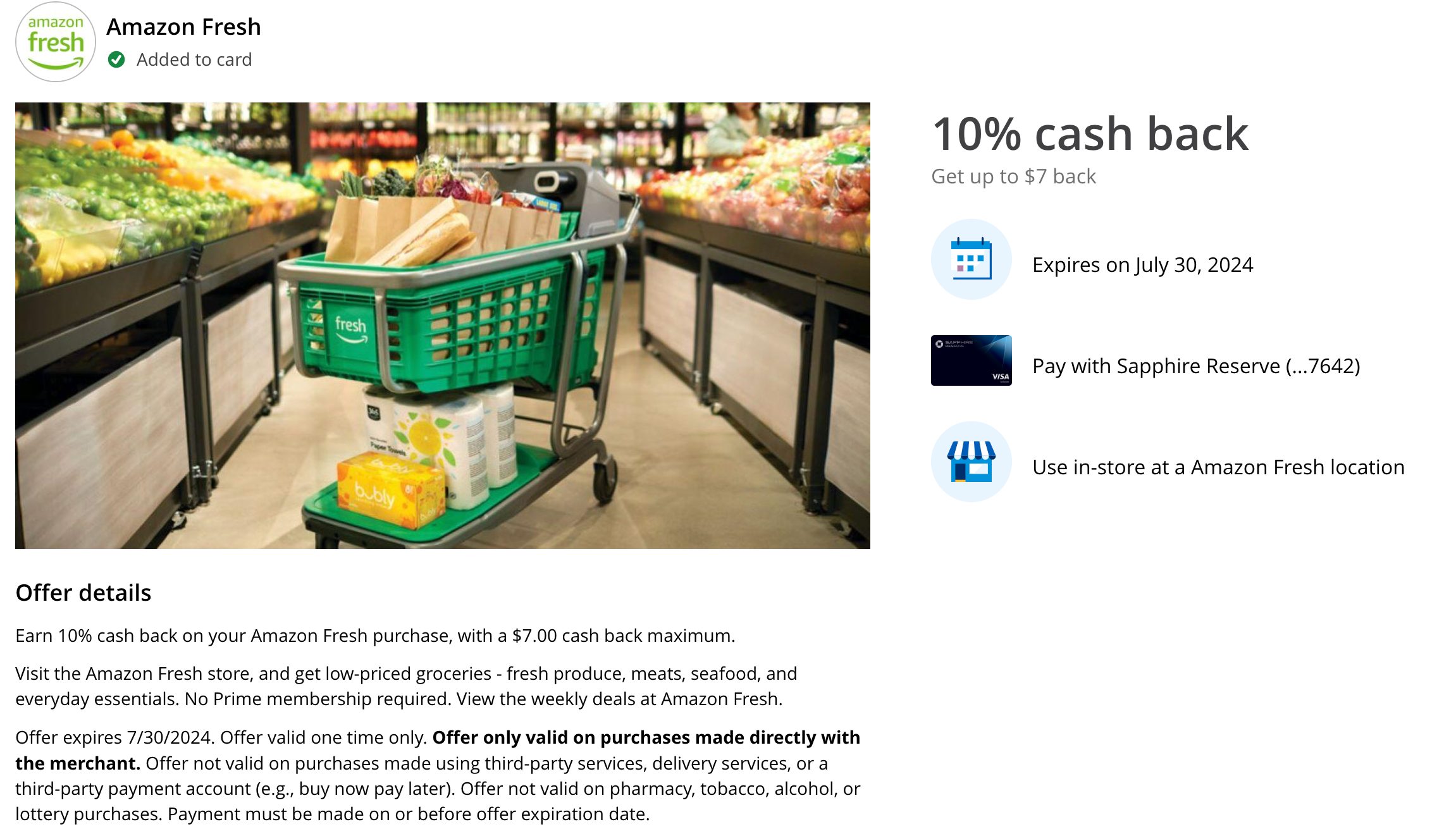

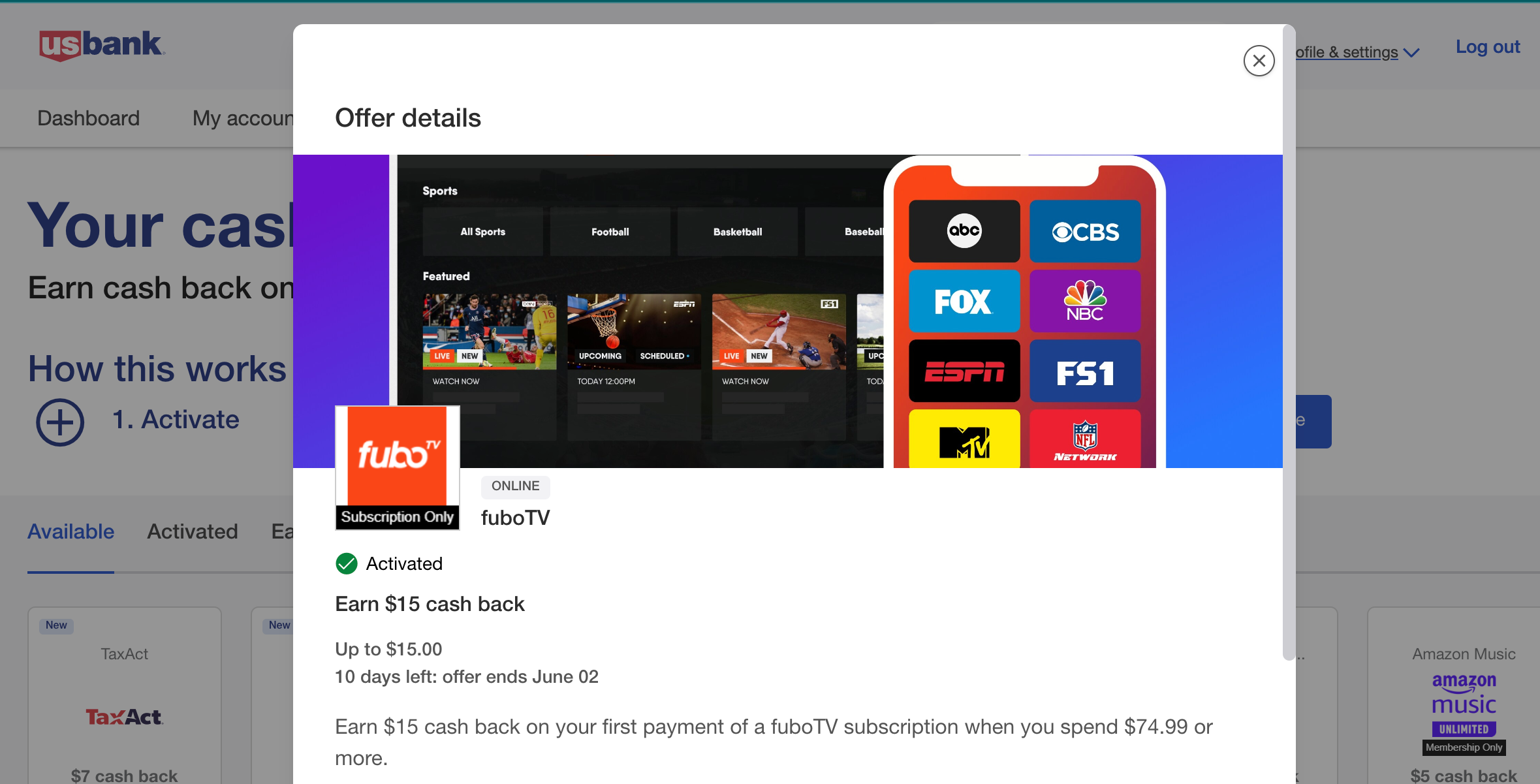

On the flip side, Chase Offers are generally less valuable than Amex Offers. Instead of getting triple-digit rebates, you'll find quite a few that are far less exciting. For example, this Amazon Fresh offer has a maximum savings of $7:

Here are some of our favorite Chase cards:

- Chase Sapphire Preferred® Card (see rates and fees): Earn 75,000 Ultimate Rewards points after you spend $5,000 on purchases in the first three months of account opening. Earn 3 Ultimate Rewards points per dollar on dining and 2 Ultimate Rewards points per dollar on travel purchases.

- Chase Sapphire Reserve® (see rates and fees): Earn 150,000 bonus points after spending $6,000 on purchases in the first three months of account opening. Earn 3 Ultimate Rewards points per dollar on dining purchases.

Related: Your ultimate guide to Chase Offers

Citi Merchant Offers

Like Amex, the Citi Merchant Offers program includes offers from a huge volume of merchants. Offers are conveniently sorted by category, making it easy to scroll through and add anything that catches your eye.

With Citi offers, the devil is in the details. The fine print of each offer is often very specific, so make sure your purchase is in line with the terms and conditions. For example, chain restaurants may only be valid at specific locations rather than nationwide and sometimes travel discounts only apply to prepaid bookings. Still, if you see a deal like $250 off a $1,000 Carnival cruise purchase, the savings are significant enough to be worth your time.

Additionally, you can download the Citi Shop desktop browser extension if you have an eligible U.S. Citi credit card. When you're shopping online, the Citi Shop extension automatically searches for offers that can save you money on your purchase — either as a percentage off or an amount you'll receive back as a statement credit on your card. Just activate the offer and use your eligible Citi card to pay for your purchase.

If you're looking for a new Citi card, consider applying for the Citi Strata Premier® Card (see rates and fees). It's currently offering 60,000 ThankYou points after you spend $4,000 on purchases in the first three months of account opening, which you can use for many great redemptions.

U.S. Bank cash-back deals

U.S. Bank's version of a merchant offers program uses the same backend system as you see on Chase and BankAmeriDeals.

Though that means you might not see something new or noteworthy, it does mean you have another opportunity to load an offer to your account, especially since so many discounts are capped at low dollar amounts.

Unlike Chase, U.S. Bank doesn't require you to load an offer to a specific U.S. Bank-issued card. Once you activate an offer, it's valid for any of the cards on your account, but you can only use it once.

Related: How to choose the right credit card for you

Stack with a shopping portal

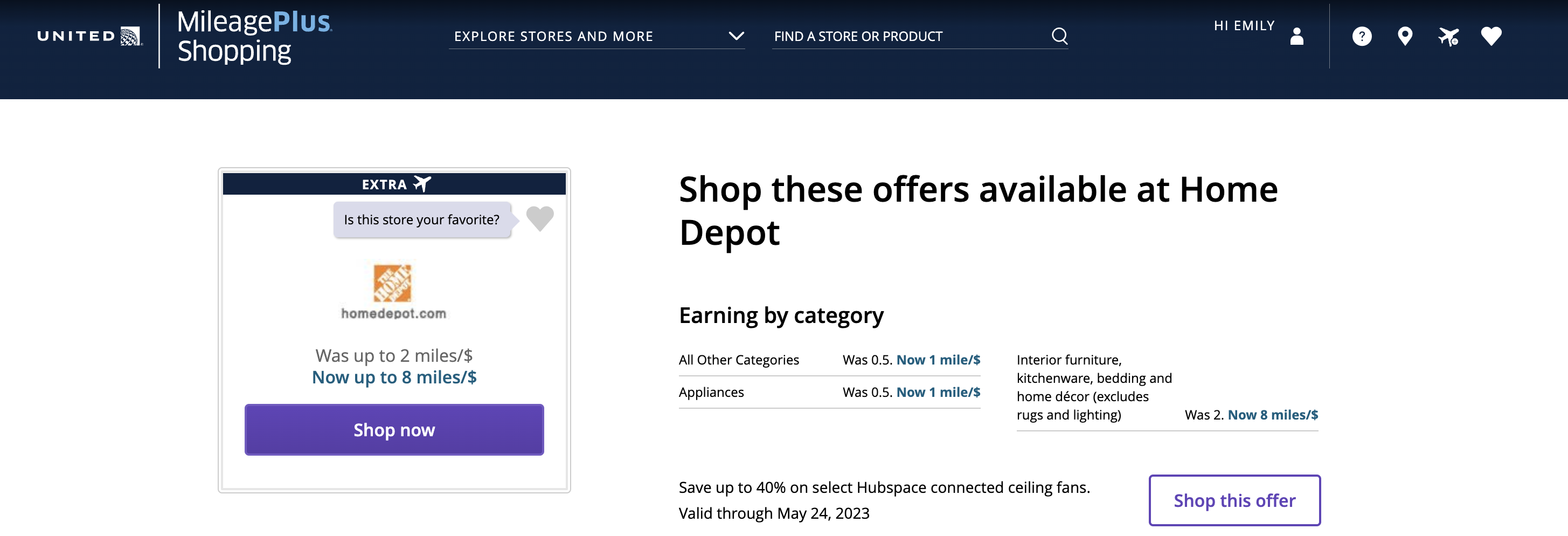

Barring some specific Amex Offers, the bulk of these merchant-specific offers trigger when you make an eligible purchase with your credit card. You do not always need to click through a special link to use your offers, meaning you can stack with a popular airline, hotel or cash-back shopping portal to earn even more points.

Shopping portals reward you with bonus points when you click through the portal before making a purchase with a specific merchant. For example, the United shopping portal might be offering 1 mile per dollar at Home Depot. So if you have a Home Depot Amex Offer, you can click through the United portal first, pay with your Amex and earn bonus United miles and Membership Rewards points on your purchase.

Most major airlines, hotels, and even some transferable points currencies have their own shopping portals. One of our favorites is Rakuten — it's technically a cash-back portal, but you can opt to earn Amex Membership Rewards points instead. The portal sometimes offers new members up to $40 bonus after spending a certain amount within 90 days of opening your account.

Consider using a shopping portal aggregator to earn the most rewards on your purchases. These will show you earning rates for all the major portals side-by-side, so you always get the highest possible return on your purchases.

Related: Don't want to miss out on earning bonus points? There's an extension for that

Bottom line

You might have access to a plethora of different discounts or bonuses to enjoy across your credit card portfolio. Amex tends to have the most headline-worthy rebates, but realistically, the best offers will be those at retailers you shop with anyway.

Try and make it a habit to look through all your available offers and add the ones you might use. There's no harm in not using a linked offer; you might as well save money where possible. Just make sure to use the card with the linked offer when you pay for your purchase.

Learn more: The best credit cards

For rates and fees of the Amex Green, click here.

For rates and fees of the Amex Gold card, click here.

For rates and fees of the Amex Platinum card, click here.