Why never using some of your credit cards may cause you to lose them

Update: Some offers mentioned below are no longer available. View the current offers here.

Credit card issuers want you to use your cards. After all, a no-annual-fee credit card sitting unused in your sock drawer won't generate revenue for the financial institution that issued the card.

On top of this, unused credit cards can present risks. If you aren't using the card, you probably aren't checking the bill regularly, and that means criminals who gain access to your card could make a significant amount of purchases before you notice it and notify the bank. Thus, banks are in the habit of reducing credit limits or closing accounts on unused credit cards.

However, even if you don't use some of your cards frequently, you may not want the issuer to close your account or reduce your credit line. Here's why you may want to keep rarely used accounts open and how to do so responsibly.

Why banks close card accounts

Don't be surprised if a credit card issuer closes a card you keep tucked away in your wallet or a kitchen drawer. After all, issuers generally make money from consumers in three ways:

- Interest payments: You'll be charged interest when you carry a balance from month to month. You can avoid interest by paying off your balance in full each month

- Fees charged to consumers: Charges such as annual fees, late fees, cash advance fees and balance transfer fees are generally avoidable but may be worth paying for the benefits and convenience some of those fees provide

- Processing fees paid by merchants: When you use your credit card for a purchase, the merchant pays a processing fee

Issuers want cardholders who make profits for the bank, achieved through these fees. As such, issuers want to continue offering credit to cardholders who will use their card and not default on their payments.

But issuers also need to minimize the risk on cardholders who aren't profitable, such as those who don't use their card but have a high credit limit. Therefore, issuers may choose to decrease the credit line on underused accounts or completely close unused accounts.

Related: Does canceling a credit card hurt your credit?

Why you should try to keep card accounts open

When one of your card accounts closes, your credit score will usually decrease. For example, when my mother-in-law closed her cobranded Southwest credit card last year, her credit score dropped by about 20 points.

Five factors go into calculating your credit score, and closing a card can negatively impact two of them: credit utilization and the length of credit history.

Credit utilization

Once an account is closed, you'll have less credit available to you. Having less available credit hurts your credit utilization ratio. For example, if you have $3,000 in credit card debt and four cards, each with a $5,000 credit limit, you are using $3,000 of your $20,000 overall limit — 15%. But if an issuer closes one of your cards, you are now using $3,000 of a $15,000 overall limit, which is a higher 20% utilization. In this case, your credit utilization ratio will jump, despite your debt remaining the same.

Generally, you want to keep your credit utilization ratio under 20-30%. Suppose an issuer closes your account or decreases your credit line. In that case, you'll need to reduce your credit card debt or increase your available credit to keep the same credit utilization ratio. To do this, you'll either need to pay down debt or ask one of your other issuers for an increase in your credit line. Doing so will allow you to reduce the impact on your credit score of having a card closed.

Related: What is a good credit score?

Length of credit history

Your credit score could also dip if the credit card that is closed is one of your oldest. One factor that makes up your credit score is the length of your credit history. If your credit history's average length falls because of a closed account, your credit score might decrease. So, it's best to work extra hard to keep your oldest accounts open.

Related: 6 things to do to improve your credit

How to keep infrequently used card accounts open

There are many reasons you may not use a card very frequently. However, you'll likely want to keep all of your cards active, especially if the card in question may be useful in the future or is one of your oldest accounts. Here are two things to do.

Spend on each card at least once every six months

Generally, you should use an account at least once every six months to keep your account active. My husband and I review all our accounts at least twice a year and load $5 from each rarely used account onto my Amazon Gift Card balance. Doing so keeps the accounts active. We use our Amazon balance to purchase gift cards and other products we need.

There are other ways to spend regularly on your cards. For example, you could set up at least one subscription service — such as Hulu or Spotify — on each of your cards. You could also designate each card for a specific category of spending, such as gas, groceries, restaurants, travel purchases and charity donations. But, if you take this approach, be sure you align the cards with the categories in which they earn the most rewards.

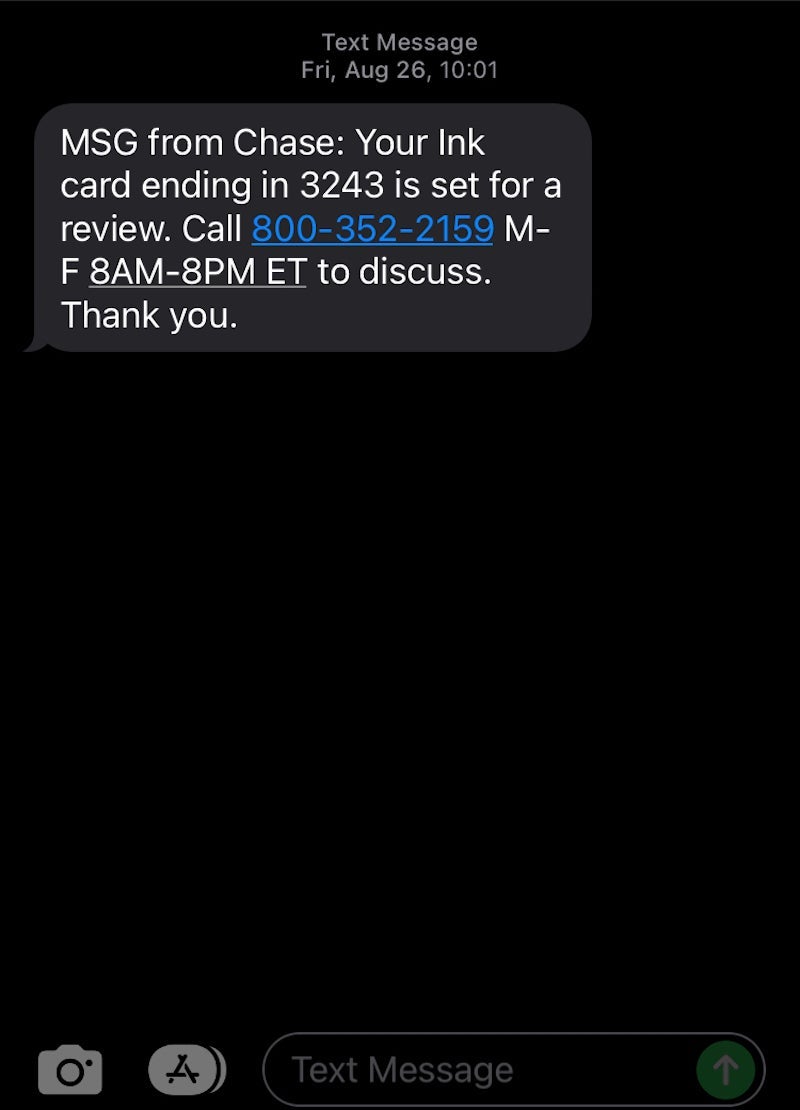

However, if this notice that two TPG employees received is anything to go by, you may want to spend on your cards more frequently than once per year.

In August 2022, TPG contributor Ryan Smith received a text message from Chase stating that one of his Ink business cards was slated for review and possible closure due to inactivity. Despite a calendar reminder to use his old credit cards every 90 days, Ryan had overlooked this card and not used it at all in 2022 — a gap of nearly nine months of inactivity prior to this text message.

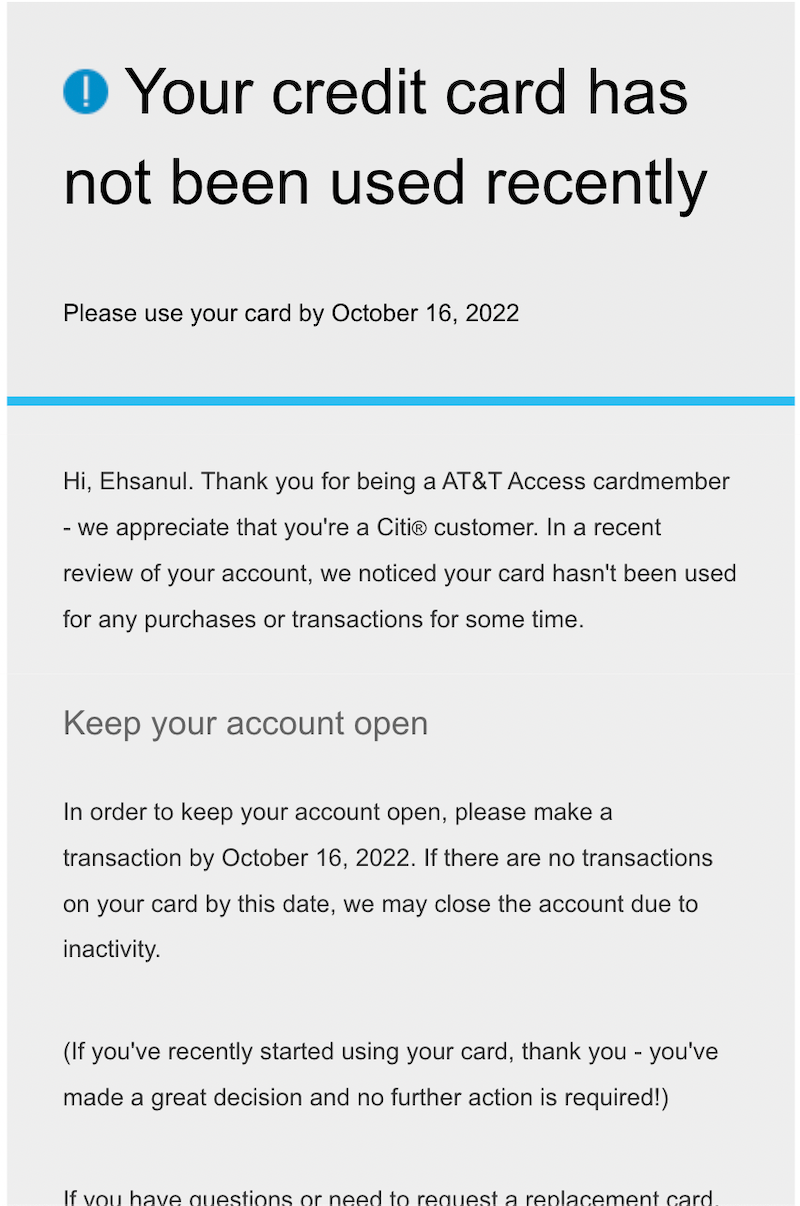

Points and miles contributor Ehsan Haque received a similar notification, giving him a little over a month to use his dormant credit card so they bank wouldn't close it. Prior to receiving this notice, Ehsan hadn't used this particular credit card in more than eight months.

Watch for closure notices

Some credit card issuers will notify cardholders about an impending card closure, while others will just drop the hammer with no warning. So, if you receive a notice that your card account will be — or has been — closed, you may be able to keep the card account open by calling your issuer and pleading your case.

For example, a couple of years ago, I received a notice that my cobranded United Airlines credit card was being closed. I called the number on the back of my card and explained to the agent why I wanted to keep the card. I hadn't used this card in the last year but said that I hoped my travel on United would soon increase, which would mean I'd be using my card more. The agent agreed to keep my account open, but I could have prevented this situation by using my card even just a few times each year.

Make sure you keep your contact information updated with your credit card issuers. That way, you'll receive emails, text messages or letters notifying you of any pending account closures.

Bottom line

As inflation continues, it's vital to recession-proof your credit score. One way to protect your credit score is to periodically spend on rarely-used cards. After all, card issuers are less likely to close active accounts. The ideal frequency to keep your credit cards active is to spend on them at least once every six months.

You'll want to keep your card accounts open to maintain account history and credit utilization, especially on cards with high credit limits or long account history — both of which can help to improve your credit score.

Related: The best credit cards