The complete history of credit cards, from antiquity to today

Update: Some offers mentioned below are no longer available. View the current offers here.

The Points Guy has been reporting on credit cards since 2010, helping you maximize purchases for future travel. But points and miles are a relatively new offering in the grand scheme of the history of credit cards.

While credit cards haven't always looked the way that they do now, credit has been a key financial tool helping people purchase goods and services for thousands of years. From ancient civilizations to the modern day, credit has been a sustaining driver of economies and one that will continue to evolve well into the future.

Ancient credit cards

When you think of "credit cards," you probably consider them to be a modern financial innovation. However, the concept of a credit card dates back to ancient times. Credit has been around for almost as long as money itself.

The Mesopotamian and Harappan civilizations used clay tablets to track their trade and transactions, much like modern-day credit cards. According to Jonathan Mark Kenoyer, an archaeologist and professor of anthropology at the University of Wisconsin-Madison, earthen tablets bore seals from the two civilizations and were used out of necessity. The volume of goods being traded between them was so large that paying with physical money would have been too cumbersome.

Later, in the Babylonian empire, some of the first written rules regarding lines of credit appeared in the Code of Hammurabi. These lines of credit worked more like modern-day loans rather than credit cards. Interestingly enough, many of the rules around delinquencies and fraud are still mirrored in modern credit card protections and regulations.

The 1800s: Charge coins and the birth of American Express

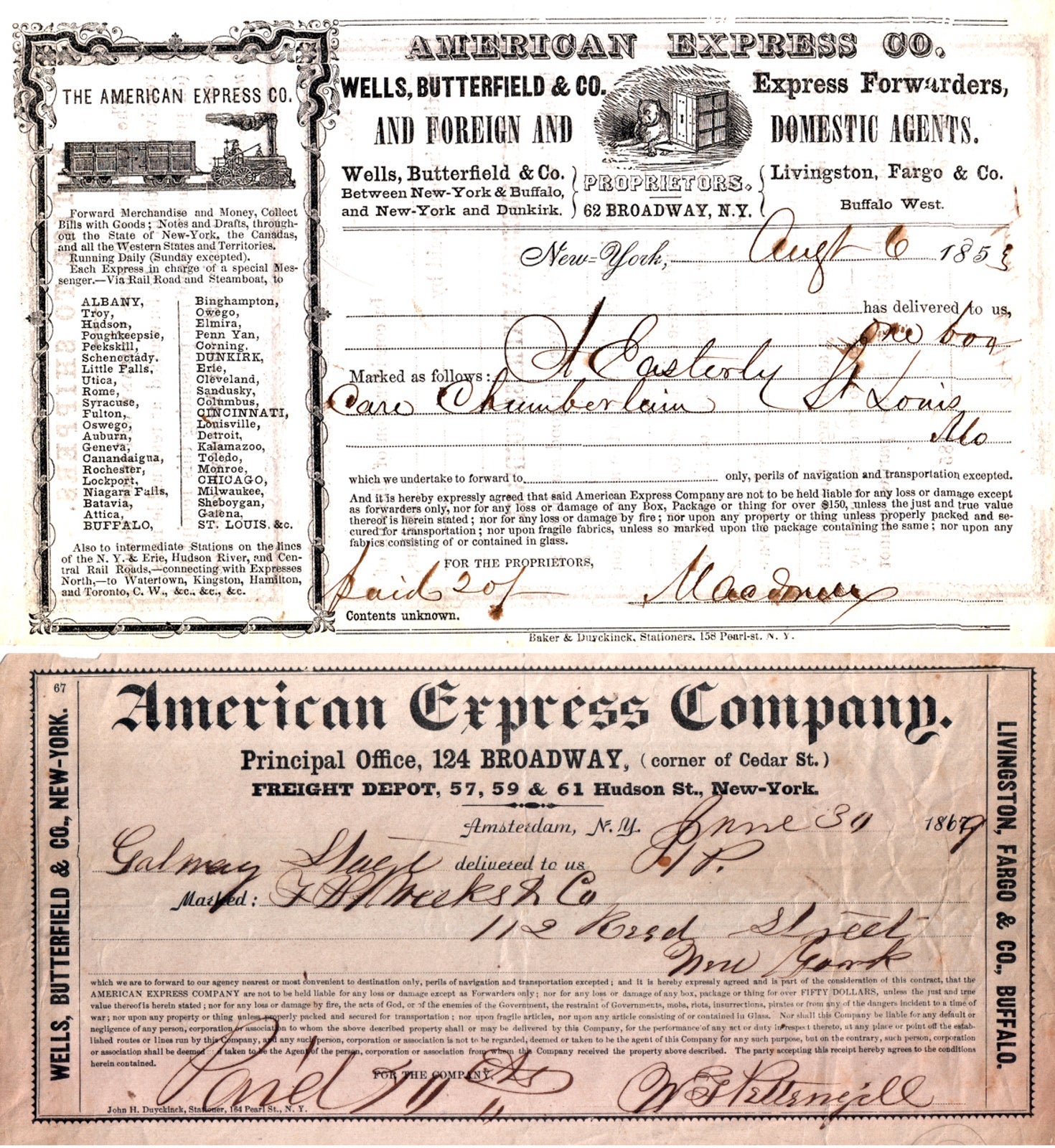

It's only fitting that card giant American Express should be an important part of the financial industry's history. American Express was the product of a merger among three companies — Wells & Co.; Livingston, Fargo & Co.; and Wells, Butterfield & Co. — on March 18, 1850. Since then, the company has become a globally integrated payments company that reported $72.7 billion in revenue in 2024.

By 1865, the company boasted more than 900 offices in 10 states. That same year, American Express introduced the first charge coin. These were mainly issued by department stores and displayed a customer's identification number and an image connected with the merchant.

Meanwhile, in 1868, the company merged with Merchants Union Express Co. to become American Merchants Union Express Co. Five years later, it took on the name American Express Co.

Also in the 19th century, American Express created its first money orders and traveler's checks (institutions in the U.K. are credited with creating the first versions of these two financial instruments in the late 18th century). In 1895, Amex's first European office opened in Paris, with expansions to England and Germany occurring by 1898.

1900-1940: Shopper's plates and the first travel rewards credit card

The period between 1900 and 1940 saw an increase in credit as a payment form. Many department stores and gas stations began offering shopper's plates to regular customers. These metal plates were similar to modern credit cards, measuring 2 1/2 by 1 1/4 inches and containing customers' names and billing addresses.

Merchants kept shopper's plates in-store and used them to generate receipts and track the amount each customer owed.

The first airline credit card

The first travel credit card that looks more like today's models debuted in 1934 when American Airlines introduced the Air Travel Card. The card contained a unique number tied to each customer's account — just like modern-day credit cards.

The Air Travel Card was valid for American Airlines purchases. Eventually, 17 other airlines began accepting it as a payment form for airfare. In place of earning points on flights, cardholders received a 15% discount on airfare purchases charged to the card.

How does that stack up against the modern-day Citi® / AAdvantage® Platinum Select® World Elite Mastercard® (see rates and fees) If you charged a $500 fare to the Air Travel Card, you would have earned a $75 discount. Meanwhile, charging $500 in American Airlines airfare to the Citi AAdvantage Platinum card earns 1,000 miles, which, according to TPG's November 2024 valuations, are worth $16.

While the Air Travel Card from 1934 was more rewarding on airfare purchases, it didn't offer a sign-up bonus or earn rewards on nonairfare purchases. In that regard, we're much better off today.

The information for the Citi / AAdvantage Platinum Select has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.

Related: The best airline credit cards

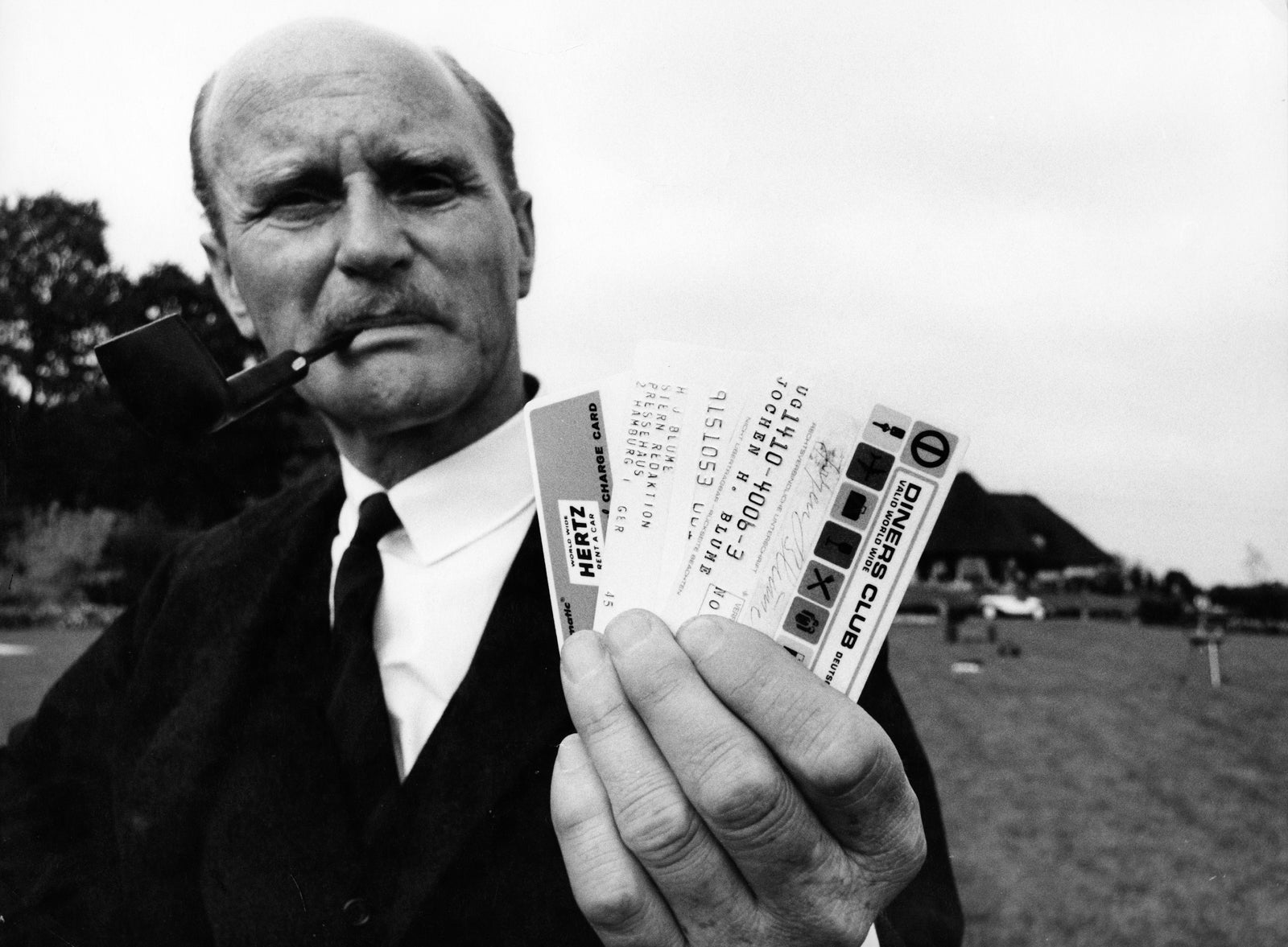

The 1950s: Diners Club introduces the first charge card

The Diners Club Card, introduced in 1950, was the first multipurpose charge card that consumers could use at various merchants. Legend has it that it was created by a businessman named Frank McNamara, who forgot his wallet while dining out in New York City and resolved never to face the same embarrassment again. A year later, he returned to that same restaurant and paid with the first cardboard Diners Club Card. The story is apocryphal, but McNamara did indeed co-found the first modern charge card.

Initially, the Diners Club Card was valid at a few dozen restaurants in New York and had around 200 cardholders. The company made money by charging customers an annual fee of $3 and restaurants a 7% transaction fee. By 1953, the Diners Club Card was accepted in the U.K., Canada, Cuba and Mexico.

1958 was a monumental year for the Diners Club Card. The company had its first TV ad as a sponsor of the New York Giants. Diners Club then entered the travel market, partnering with travel agencies in major cities that accepted the card for the purchase of airline, steamship (the jet age was just starting!) and cruise tickets.

American Express and Bank of America join the competition

Meanwhile, American Express launched its first charge card in the U.S. and Canada. At first, the card was purple cardboard, but by 1959 it had become the green plastic card we know today.

That same year, Bank of America launched what became the first nationally licensed credit card program, BankAmericard. The card was valid at a variety of merchants and pioneered the 25-day grace period and installment payments. Following rapid adoption and growth, the program expanded around the globe and eventually became known as Visa.

Also in the late 1950s, Chase and many other banks started credit card programs, but most quickly failed. By 1959, Diners Club reached a million cardholders and was listed on the New York Stock Exchange.

The 1960s: The growth of the credit card industry

The 1960s were a watershed decade for the credit card industry.

Following the launch of the BankAmericard in California, almost a million BankAmericards were in circulation by the end of 1960. Just six years later, Bank of America began licensing it as the first general-purpose credit card across the country. By June 1966, 61,000 merchants across 42 states accepted the BankAmericard.

Citi and American Express also launched new cards during this time. First National City Bank (now Citi) began issuing the "Everything Card." Meanwhile, Amex established its first corporate card program for commercial customers in 1966. First National City Bank would eventually join a new association of banks — the Interbank Card Association — to launch Mastercard.

The information for the BankAmericard has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.

The Truth in Lending Act

In response to the boom of credit card accounts, the Truth in Lending Act was enacted in 1968. The Federal Reserve Board implemented this set of regulations in the hopes of protecting consumers as they dealt with creditors. Most notably, the TILA requires card issuers to disclose certain information before issuing a consumer a credit card, including the annual percentage rate and fees associated with the card account.

The same year the TILA went into effect, the Interbank Card Association formed partnerships with banks from around the world. In the following decade, the ICA would revamp its brand to Mastercard.

From 1966 until 1970, more than 100 million credit cards were produced and mailed, unsolicited, to customers the banks had deemed creditworthy — a far cry from the sometimes stringent application process of the current credit card landscape. Not surprisingly, this mass distribution invited a wave of white-collar crime, privacy concerns and legislative debates.

By 1970, the practice of issuing unsolicited credit cards had been banned. Issuers could only send out application requests — a practice that has continued in full force ever since, as mailboxes full of application solicitations can attest.

Finally, in 1969, IBM developed magnetic-stripe technology, which would play a large role in the evolution of credit card tech as a whole in the 1970s and beyond.

The 1970s: Credit cards evolve

The 1970s were a decade of improved regulation, technological advances and rebranding of some credit card networks into names that we recognize today. Now, let's consider each of these three advancements in slightly more detail.

Regulation

Until the 1970s, many credit card issuers would simply mail credit cards to consumers whether they had requested them or not. Folks were left to destroy or mail back the cards they didn't want. The Unsolicited Credit Card Act of 1970 stopped the unsolicited distribution of credit cards issued by oil companies, retailers and most other creditors — but common carriers and banks were both exempted due to jurisdiction issues.

The 1970s saw various other credit card regulations, including the:

- Fair Credit Reporting Act (1970) to ensure the accuracy and fairness of credit reporting as well as require consumer reporting agencies to adopt reasonable procedures such as consumer access to their credit reports.

- Equal Credit Opportunity Act (1974) to prohibit lending discrimination based on sex or marital status. This act was amended in 1976 to also prohibit lending discrimination based on race, religion, national origin, age, the receipt of public assistance income or exercising one's rights under certain consumer protection laws.

- Fair Credit Billing Act (1974) to protect consumers from unfair credit billing practices and provide a pathway for consumers to dispute charges from credit card issuers.

- Fair Debt Collection Practices Act (1977) to eliminate abusive debt collection practices by debt collectors and to promote consistent state action to protect consumers against debt collection abuses.

Related: Why a credit card is a smarter choice than a debit card

Technological advances

In 1971, IBM partnered with the banking and airline industries to develop an international standard for magnetic-stripe credit cards. This would soon allow cardholders to use their credit cards worldwide. Likewise, throughout the 1970s, various credit card networks implemented electronic authorization systems, which could then facilitate the use of electronic clearing and settlement systems; for example, National BankAmericard debuted this technology in 1973.

Rebranding

First, BankAmericard rebranded to Visa in 1976; then, the Interbank Card Association became Mastercard in 1979. Both credit card networks rebranded to facilitate international growth and acceptance.

The 1980s: The travel loyalty boom

In the 1980s, the financial services industry boomed, making it a competitive time for credit card issuers as they introduced new products. The '80s also ushered in the era of travel loyalty programs as we know them today, including frequent flyer, hotel and car rental rewards programs.

American Express, Visa, and Mastercard all introduced premium card products in the early-to-mid-1980s. Amex already appealed to a more affluent customer base, and the 1984 debut of The Platinum Card® from American Express solidified this notion. At the time, the card carried a $250 annual fee and offered 24-hour concierge service, travel insurance, and access to private clubs around the world. Adjusted for inflation, the annual fee would be $630 — significantly less than the $895 you'd pay today (see rates and fees).

While most credit cards up to this point were aspirational products aimed at premium customers, Discover bucked this trend in 1983 by introducing the no-annual-fee Discover Card by Sears, Roebuck and Co. The card was widely promoted in an ad during the 1985 Super Bowl.

The mid-to-late 1980s also saw the launch of affinity and cobranded credit cards. In 1986, Continental Airlines teamed up with Marine Midland Bank (now part of HSBC) on the Continental TravelBank Gold MasterCard, and American Airlines partnered on a card with Citi a year later.

Finally, the mid-1980s saw the first credit card rewards program, Diners Club Rewards.

The 1980s was a huge decade for card issuers and consumers alike. These new products and loyalty programs set the tone for the ensuing decades and for the current iteration of cards, points, and miles that we know and love today.

The 1990s: Credit cards get high-tech (and high-end)

The 1990s saw two of the biggest changes to the world of credit card rewards: the programs we use to redeem our miles and the physical cards themselves. Amex kicked off the decade by launching Membership Miles in 1991, the precursor to today's hugely popular Membership Rewards program.

You can tell how much has changed by looking at the original seven Amex transfer partners, only two of which are still in business: Delta Air Lines and Southwest Airlines. Continental, Northwest Airlines, Pan Am, Midway Airlines, and MGM Grand Air are all gone. While the program has changed a lot over the years, Amex struck gold with the idea of transferable points. Nowadays, several other major issuers have followed suit in some form or another.

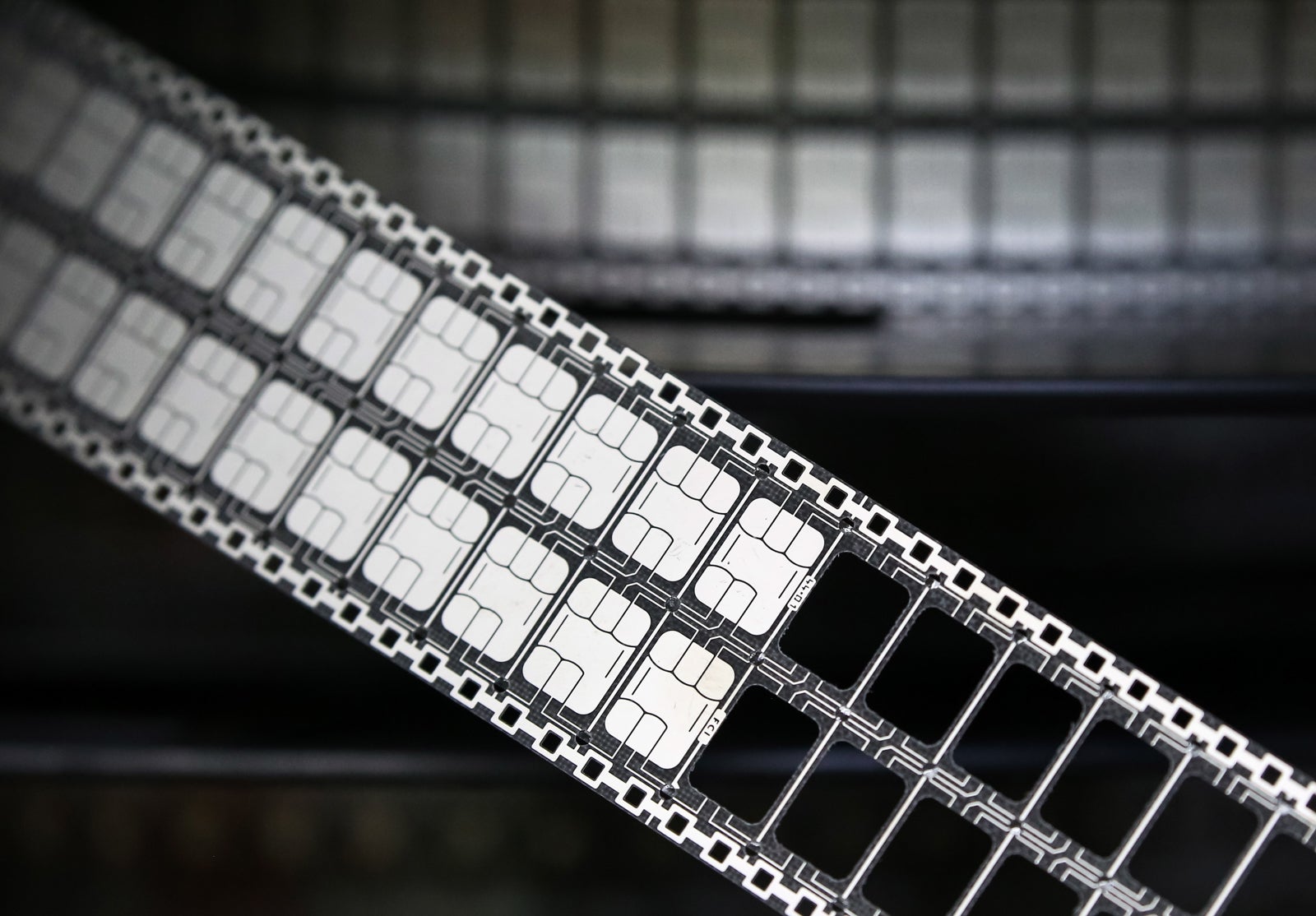

Combating fraud with EMV technology

As credit cards continued to gain popularity around the world, fraud became a larger concern. EMV chip technology — the "EMV" stands for Europay, Mastercard, and Visa — debuted in Europe in the mid-90s. This technology, which has since become commonplace on credit cards, creates a unique transaction code for each purchase to help mitigate the risk of fraud. While most cards continue to offer the traditional magnetic stripe on the back, many payment processors insist that you use your card's chip instead of swiping.

The Black Card hits the market

Building on the success of its premium Platinum Card and Membership Miles program, Amex recognized an opportunity to further segment the premium credit card market. The company began targeting ultrawealthy and high-spending businesses and individuals.

The exclusive Amex Centurion Card was launched in the late '90s. According to an urban legend, we may have Jerry Seinfeld to thank for it. We tried to confirm this, but he was likely one of several clients. The invitation-only Centurion Card has remained highly secretive, but TPG was able to collect some intel on the perks Centurion cardholders enjoy — and what they pay for the privilege.

The 2000s: The competition grows

In the 2000s, competition among issuers intensified, forcing banks to step up their game and make credit cards more rewarding than ever. During this time, issuers introduced completely new rewards programs, bonus spending categories, unique card benefits, and all-time-high welcome bonuses.

Rewards programs shifted to be more travel-specific. Many of the biggest card issuers introduced airline and hotel transfer partners. Some even made travel benefits like automatic elite status and complimentary entrance into airport lounges more accessible.

By the early 2000s, American Express Membership Rewards, Chase Ultimate Rewards and Citi ThankYou Rewards each offered over a dozen airline and hotel partners. All three issuers also offered multiple credit cards, ranging from basic to premium. Capital One followed suit shortly after.

The 2010s: The golden age of credit cards

The 2010s marked the beginning of the golden age of credit cards. Citi made a splash in 2011 by introducing the Citi Premier® Card — now the Citi Strata Premier® Card (see rates and fees) — and the Citi Prestige® Card (no longer available). But what really shook up the industry was the launch of the Chase Sapphire Reserve® in 2016. It debuted with a whopping 100,000-point sign-up bonus (the current offer is 150,000 bonus points after spending $6,000 on purchases in the first three months from account opening). At the time, it earned 3 Ultimate Rewards points per dollar spent on dining and offered a flexible $300 annual travel credit as well as other perks. The response was overwhelmingly positive — to the point that Chase temporarily ran out of the metal used to make the cards.

The information for the Citi Prestige Card and Citi Premier Card has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.

In sum, the 2010s were a decade marked by the debut of many new cards on the market, as issuers tried to one-up each other with better welcome offers and earning rates. Coupled with the golden age of air travel — with passenger numbers soaring in 2019 — the credit card and travel industries were certain that it would only go up from there.

The 2020s: Pandemic era and beyond

Then, the coronavirus pandemic hit. By mid-March 2020, nearly all travel had come to a complete stop. For many, this meant their travel rewards cards were going straight to their sock drawers — and cash-back cards became king.

While issuers tried to adapt — adding useful statement credits to encourage cardholders to keep spending while staying at home — many people downgraded or outright canceled their cards. Issuers even cut credit limits to mitigate financial risk. 2020 was a challenging year for everyone.

It wasn't all bad news, though. Technology also evolved. Before the coronavirus pandemic, almost all credit cards had an embedded smart chip for greater security. Then, the pandemic actually sped up the implementation of contactless payments nationwide. While Google pioneered the idea of digital wallets with the launch of Google Pay, both Apple Pay and Samsung Pay started to become popular options as consumers increasingly turned to digital wallets.

The rebound in travel after this period has been astounding, and today, we're seeing demand for travel as strong as ever. There continues to be heavy demand for premium cabins on airlines, so much so that it's tough to find availability due to less seat availability and more people vying for a redemption.

There have also been some changes in the credit card landscape, with more issuer-based lounges offered. For example, in 2023, Capital One opened a lounge at Denver International Airport (DEN), and in 2024, a Capital One Landing debuted at Ronald Reagan Washington National Airport (DCA). Likewise, both Chase and American Express have expanded their lounge footprints, with Chase Sapphire lounges opening in Phoenix Sky Harbor International Airport (PHX) and San Diego International Airport (SAN) and a new Centurion Lounge in Hartsfield-Jackson Atlanta International Airport (ATL).

Credit card issuers continue to compete for more users, and several cards have seen refreshes of their benefits and earning rates and, of course, increases in annual fees. The American Express® Gold Card was refreshed to include new statement credits, spending caps, and an increase in the annual fee. Capital One discontinued the popular legacy Capital One Savor Cash Rewards Credit Card, and the no-annual-fee Capital One SavorOne Cash Rewards Credit Card was rebranded as the Capital One Savor Cash Rewards Credit Card. Furthermore, the cobranded Hilton credit cards issued by American Express saw significant changes, such as the Hilton Honors American Express Surpass® Card and the top-tier Hilton Honors American Express Aspire Card.

With more and more individuals applying for credit cards for elevated perks and benefits, we continue to see a trimming or removal of benefits that have been longstanding. Just this year alone, several premium credit cards lost access to Priority Pass restaurants, including the Chase Sapphire Reserve (see rates and fees) and the Capital One Venture X Business.

We can speculate that in order to curb overcrowding in lounges, credit cards may start to cut their generous guest policies, such as the Capital One Venture X Rewards Credit Card, which offers cardholders and authorized users the ability to bring up to two guests for no additional fee. American Express limits guests to Centurion Lounges for The Platinum Card from American Express cardmembers — requiring that they spend at least $75,000 on eligible purchases on their card within a calendar year to qualify for complimentary guest access for up to two guests per visit. In addition, Delta SkyMiles® Reserve American Express Card and Delta SkyMiles® Reserve Business American Express Card cardmembers have a cap on Sky Club lounge visits as a means to combat lounge overcrowding.

The credit card industry is known for one thing: remaining resilient despite times of change. As we look ahead, we can expect card rebrands and new card unveilings that will likely come with increased annual fees and perhaps even fewer valuable benefits and generous welcome offers.

The information for the previously named Savor and the no-annual-fee SavorOne cards has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.

Bottom line

Over the past century, credit cards have advanced tremendously. In 2022, 82% of Americans carried at least one credit card, making credit an essential part of personal finance and of participating in our economy. With so many advancements, it will be interesting to see how technology continues to shape the industry.

Pretty soon, we may ditch our beloved plastic and metal cards altogether, as credit card technology will provide improved smartphone integration. While cards may look different, the TPG team is optimistic that the future will bring even better rewards and value for customers.

Related: The best credit cards

For rates and fees of the Amex Platinum card, click here.