You can do both: 3 strategies I used to perfect my credit score and still earn points

Update: Some offers mentioned below are no longer available. View the current offers here.

When I first started my points and miles journey, I was a 20-year-old college sophomore who'd never held a credit card in my name before. I had big dreams of fancy first-class suites and luxury hotels, but I was also playing the long game.

While I was primarily interested in racking up as many points and miles as humanly possible, I also wanted to build a sustainable credit score that would benefit me later in life when I needed a mortgage or car loan. Here are the decisions I made that helped me out long term, even after those early welcome bonuses had come and gone.

Being added as an authorized user on my dad's credit card

Before I left for college, my dad added me as an authorized user on his more-than-20-year-old United Explorer Card so that I'd have it in case of emergencies. I put it in the back of my (mostly empty) wallet, not thinking much of it, and sort of forgot about it until my sophomore year, when I went to apply for my first credit card. I went to go check my credit score, not even sure if I'd have one at this stage of my life, and was shocked to see that Credit Karma was showing 20-plus years of on-time payments for me and a score in the 740s.

This was how I learned the massive advantage that comes with being added as an authorized user — you essentially get to "borrow" the credit history of whoever adds you. Here I was, not old enough to legally drink, with a very good credit history that stretched back all the way to the year I was born!

Using this springboard, I was able to get approved for several amazing travel rewards cards in my first year, including the Chase Sapphire Preferred Card and the American Express® Business Gold Card. Instead of using my early applications to try and build credit with starter cards, which generally come with lower bonuses and fewer perks, I was able to start off with some heavy hitters.

Nowadays, a lot of people are nervous about this approach, especially since it requires asking their parents (or any older individual they trust who has good credit) to add them to their credit cards. However, doing so helps boost your average age of accounts, which goes a long way toward building credit. That's why it's important to ask the person in your life who has had their card open the longest.

Related: Credit cards with the greatest value for authorized users

Many people are worried that adding someone as an authorized user is risky because they can rack up charges and leave you on the hook, but there's an easy way around that: Just don't give them the card. In order for your credit score to benefit, the authorized user account simply has to be open. You never need to spend anything on the card, and you don't even need to have it in your possession for this to work. So parents, add your children as authorized users to help boost their credit, and either set a limit on what can be spent on that card or simply put it in a sock drawer or rip it up.

Picking cards with no annual fee that I could keep open forever

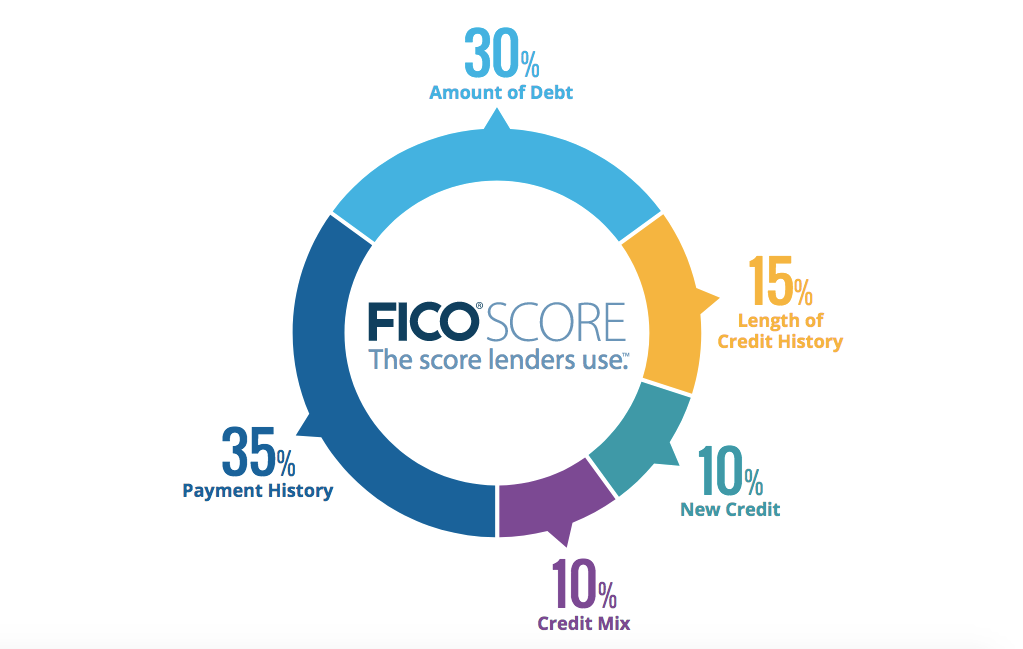

When you're just starting out with your first credit card(s), one of the biggest weaknesses on your credit report is likely to be your low average age of accounts (or length of credit history). This category counts for roughly 15% of your credit score, and if your age of accounts is too low, you might get automatically rejected for a number of cards. In fact, my first two rejections ever, for the Citi Prestige® Card and the old Chase Ritz Carlton Card, were both because my average age of accounts had dipped below one year during my first big application spree.

The information for the Citi Prestige Card has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.

Having your parents add you as an authorized user can help you circumvent this for your early applications, but it's important that you work actively to build a strong credit history yourself. One of the best ways to do this is by opening no-annual-fee cards that you can (and should) keep open forever, even if you don't use them very often. Just make sure you put a small charge on them every nine to 12 months to avoid having the account closed for inactivity.

There are a lot of cards in my wallet that I plan to keep open for a long time, but the only ones that I know with 100% certainty I'll keep open forever are the ones that don't charge an annual fee. Benefits change, loyalty programs get devalued and your favorite card right now might be obsolete in five years. By including a few no-annual-fee cards in your early applications, you can hedge against this and build a sustainable credit score.

Related: The best no-annual-fee credit cards

It just so happens that two of my favorite cards, for beginners and points pros alike, don't carry annual fees. I'm talking about the Chase Freedom and Chase Freedom Unlimited (the Chase Freedom is no longer open to new applicants), which are technically billed as cash-back cards but can earn Ultimate Rewards points if you also hold a Chase Sapphire Preferred Card, a Chase Sapphire Reserve or an Ink Business Preferred Credit Card. The Freedom Unlimited earns 1.5% cash back/1.5 points per dollar spent on purchases with no caps or limits, while the Freedom earns 5 points per dollar spent in rotating quarterly categories on your first $1,500 in purchases. These were two of the first cards I applied for thanks to Chase's 5/24 rule, and they've continued to age well on my credit report and help boost my score.

The information for the Chase Freedom card has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.

Starting with cards that were easier to get approved for

The early days of building credit history are like a game of Chutes and Ladders. Your score inches up ever so slowly, but any mistakes you make can set you back quite a ways. This is why it's very important not to overreach and to focus on cards that you have a good chance of getting approved for.

Getting rejected for a credit card doesn't actively hurt your score (you just get a new inquiry but no additional negative mark), but if your credit report has a lot of recent inquiries and a low number of total accounts or short length of credit history, banks may read between the lines and decide not to approve you the next time you apply.

Related: 8 ways to maximize your chances of being approved for a credit card

What I mean by all of this is that even if you believe firmly in the value proposition of The Platinum Card® from American Express or the Chase Sapphire Reserve, that probably shouldn't be the first card you ever apply for. There are plenty of great starter cards that are easier to get approved for, allowing you to earn points and build credit without dealing with the confusing sting of rejection early on.

Related: Amex Platinum vs. Chase Sapphire Reserve: Which card is right for you?

I was approved for the first seven cards in a row I applied for. It wasn't until I overreached and started applying for premium cards such as the Citi Prestige and Ritz Carlton Rewards cards that I ran into trouble. I learned a lot from those rejections and patiently waited until I had a full year of credit history with Chase specifically before applying for the Chase Sapphire Reserve shortly after it launched.

Bottom line

Your first couple of credit card applications are incredibly important, as they lay the foundation for how your points and miles strategy will shape up in the years to come. If you pick the right cards, you can earn hundreds of thousands of points and miles all while building a sustainable credit score that will reward you for decades to come.

Photo by Rafa Elias/Getty Images.