Will non-travel redemption options stick around on travel cards?

Update: Some offers mentioned below are no longer available. View the current offers here.

In 2020, the pandemic completely reshaped the priorities of credit cardholders who traditionally earned and redeemed points and miles predominately for travel. Suddenly, travel became the last thing on most people's minds as words like sheltering in place and social distancing enter the equation. For many, that meant holding on to your card's award earnings -- or perhaps spending rewards on items that weren't travel-related.

But as we delve deeper into 2021, a top question that many cardholders have is whether we'll continue to see lucrative ways to redeem points and miles outside of travel purchases -- even as travel continues its rebound.

This includes ways to redeem points at elevated rates on everyday categories such as groceries and dining. Chase's Pay Yourself Back program -- letting you use Ultimate Rewards points to offset certain purchases -- won TPG's 2020 Editor's Choice Award as the top innovation in credit card benefits. But will that stick sort of redemption option around or will it become one of those pandemic-era offerings that eventually fade away?

Let's take a closer look at what elevated non-travel redemptions (including dining) on top travel rewards cards might remain longer-term, and what we can look forward to later this year.

Flexible redemption options extended

Both Chase and Capital One have extended the period in which certain cardholders can use their points or miles to offset certain everyday purchases. Most notably, the redemption rate is the same as if you were to use those points or miles on travel purchases.

That's certainly not a coincidence. With many international destinations still restricted and COVID-19 variants flaring up, cardholders are still fairly limited in their travels compared to normal times. Therefore, having the option to use points or miles on other categories of spending remains a valuable benefit for many.

Related: When will international travel return? A country-by-country guide to coronavirus recovery

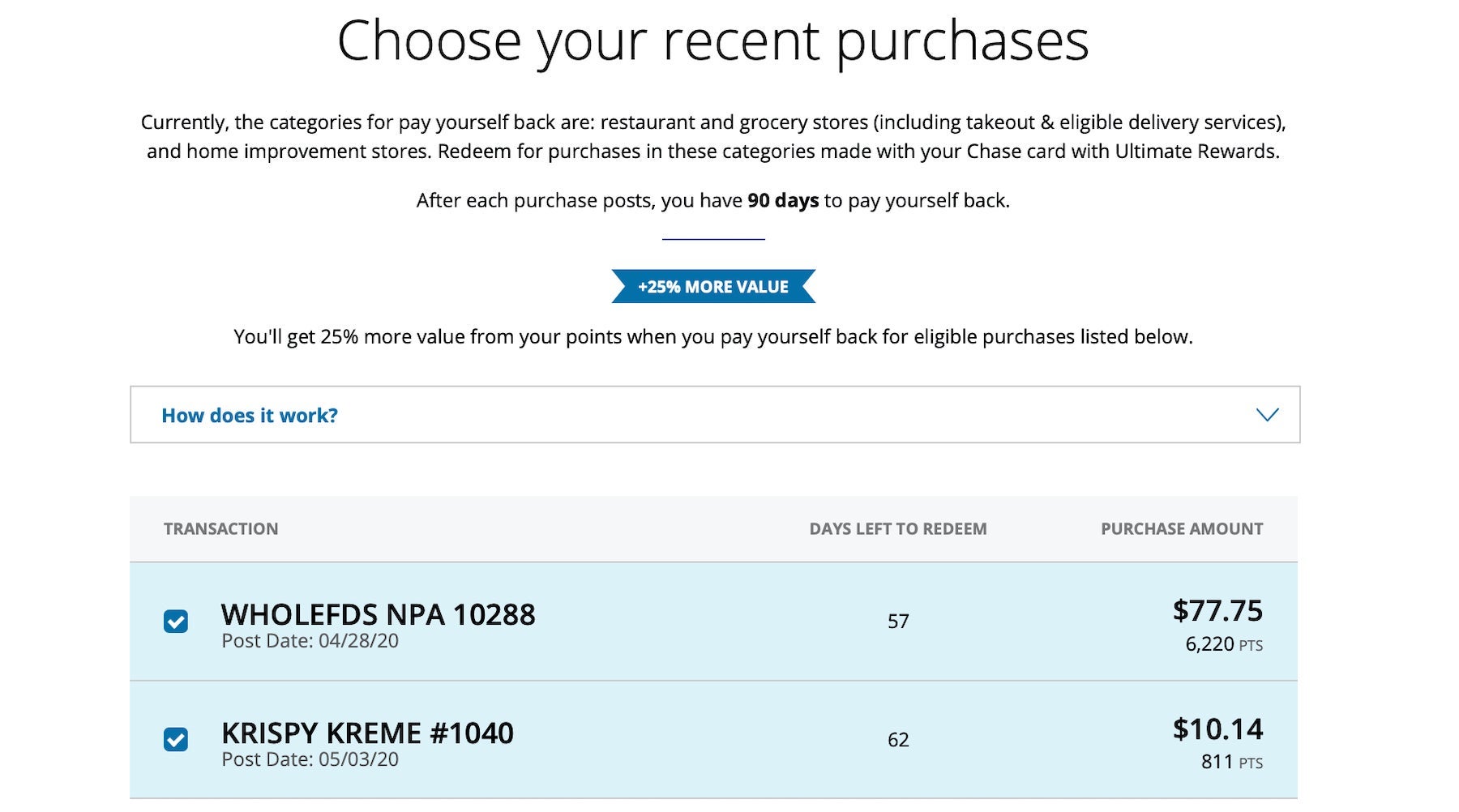

Chase Pay Yourself Back extended

The Chase Pay Yourself Back categories on both the Chase Sapphire Preferred Card and Chase Sapphire Reserve are now valid through Sept. 30, 2021. This redemption option was originally set to expire on April 30, 2021.

Related: Chase Sapphire cards make it easer to use annual travel credit and points into 2021

Chase Sapphire Reserve customers can redeem points at 1.5 cents apiece, while Chase Sapphire Preferred customers can redeem Ultimate Rewards at 1.25 cents each to offset purchases made at grocery stores, home improvement stores and dining establishments, including take-out and delivery services.

Capital One extension

Through the end of June 30, 2021, you can redeem Capital One miles for purchases made in the past 90 days on food delivery and streaming services on both the Capital One Venture Rewards Credit Card and Capital One VentureOne Rewards Credit Card. This was originally set to expire on April 30, 2021.

The redemption rate is the same as for travel -- 1 cent per point.

... but travel is recovering

Related: Domestic leisure travel demand back to pre-pandemic levels, airline CEOs say

The fact of the matter is that travel demand is recovering, so will issuers still make an effort to encourage you to redeem points on non-travel purchases going forward?

While most issuers will likely shift some of the focus of travel rewards cards back to travel, there's at least one company that may buck the trend. And we actually wouldn't be surprised to see other issuers and cards permanently flex a bit more into the lifestyle realm.

Issuers want you to use your points

Ted Rossman, industry analyst at Bankrate and Creditcards.com (owned by Red Ventures, the same parent company as TPG) says that when it comes to redemptions, issuers have an incentive for you to use your points -- and not have you sit on them.

"It's not great for issuers when people hoard points, because these show up as liabilities on their books. Since most credit card points don't expire quickly (if at all), issuers want you to use them."

Related: Why points and miles are a bad long-term investment

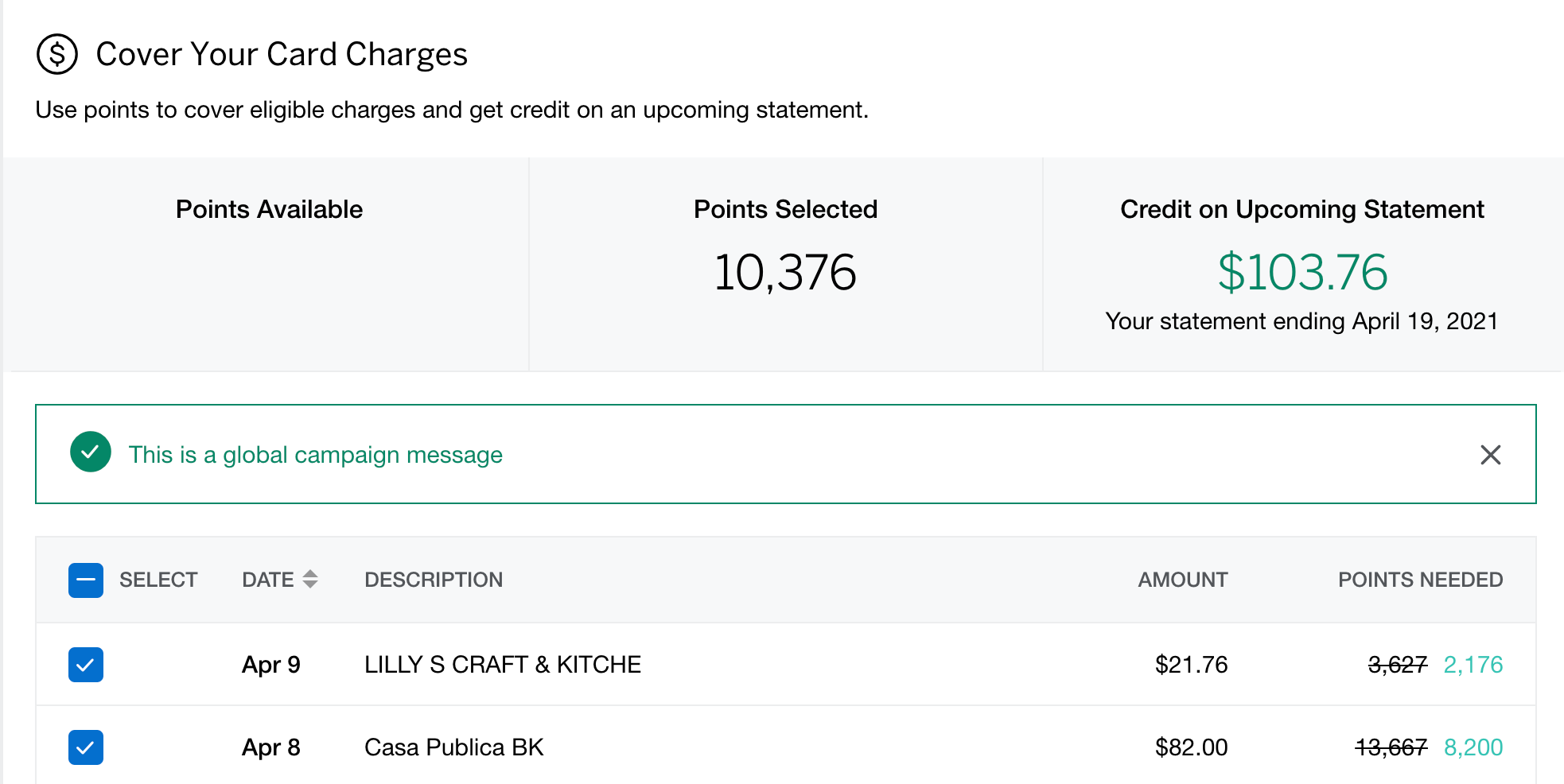

Additionally, TPG recommends that you don't hoard points, since devaluations can and do happen at any time. Several staffers took advantage of Pay Yourself Back, including TPG's Executive Editorial Director, Scott Mayerowitz, who cashed in a whopping 322,121 Ultimate Rewards points for $4,831.82 in statement credits to cover meals out and groceries.

As Mayerowitz said, "points and miles give savvy travelers unmatched flexibility."

Related: Delta devalues SkyMiles again, partner award rates skyrocket

Chase is in a unique position

Capital One has already indicated that its non-travel redemptions are only a temporary feature. And during the pandemic, American Express didn't offer any notable elevated redemption offerings using Membership Rewards points, although it did offer temporary credits and some targeted opportunities.

However, Chase has stated that Pay Yourself Back will be around, in some shape or form, for the long haul. The existing categories may change and the elevated redemption options may fluctuate but this benefit seems to be one that isn't likely to disappear in the near term.

Chase is likely aware that Pay Yourself Back even further enhances the Chase "Trifecta," a combination of three powerful cards -- the Chase Sapphire Reserve, Ink Business Preferred Credit Card and Chase Freedom Unlimited.

Rossman added that programs such as Pay Yourself Back "could be a great way to incentivize loyalty and appeal to seasoned travel hackers as well as those who only travel occasionally and mostly prefer cash back."

The only question then is whether the economics work for Chase for the long term.

"It might be a stretch, because the [up to] 50% [redemption] bonus is generous, but it could work if it attracts and retains enough spending. I'm sure Chase would look at spending and customer acquisition and retention data closely," Rossman told TPG.

Other issuers are dabbling

In recent days, we've seen both Amex and Citi further increase their options for non-travel redemptions.

Amex is targeting select cardholders with an offer to use 40% fewer Membership Rewards points to cover everyday charges. Instead of a value of 0.6 cents per point each point is worth 1 cent when redeeming towards your bill in this manner. That's still a full cent less than what TPG values Membership Rewards points when maximized with travel partners, but it makes the redemption more tempting than before.

Related: Here are 5 Amex Platinum benefits you can use from home

Meanwhile, Citi appears to have added an option to the Citi Premier® Card to cash out ThankYou points at a 1 cent per point value, similar to the Citi Prestige® Card. Previously, points were worth only 0.5 cents apiece when applied against your statement. Again, this is still less than our own TPG valuation for ThankYou points, at 1.7 cents each, but it's a non-travel redemption that Citi is clearly thinking about.

The information for the Citi Prestige card has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.

Bottom line

Both Chase and Capital One are continuing their non-travel redemptions programs for at least the next several months beyond the previously stated expiration dates. We've also seen some cards and issuers branch out more into everyday rewards and benefits beyond the traditional travel-heavy focus areas.

Even though transferring credit card points to travel partners may be the most "lucrative" way to use points, more redemption options at increased valuations benefit cardholders. After all, some might argue that flexibility is the current and future king in the credit card rewards landscape.