Chase recently made changes to its credit card lineup - here's everything you need to know

Update: Some offers mentioned below are no longer available. View the current offers here.

If you've been looking into applying for a Chase credit card recently, you may have noticed some differences in the process. For one, some of Chase's credit cards are not currently showing up on the site. Additionally, other cards are requiring a sign-in before you can apply.

Today, I'm walking through some of those changes and how they might affect cardholders looking to apply for new Chase credit cards in the coming months.

Want more credit card news and advice? Sign up for the TPG daily newsletter

Removal of some cards from the Chase site

We've received a few tips from TPG readers that some cards have disappeared from the Chase site. These include the Chase Slate, the United Club Business Card, Southwest Rapid Rewards® Premier Business Credit Card and the United TravelBank Card. (The information for the Chase Slate, United Club Business Card, and United TravelBank Card has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.)

We did get clarification from Chase about the Slate and the United TravelBank Card, the two personal credit cards missing from the Chase site. The Slate is currently still available at Chase branches, but not online. The webpage application is temporarily unavailable, but it will return in the future. As for the United TravelBank Card, I was told that at present, Chase will not be offering it to new customers.

It's unclear if you are still able to product change to the United TravelBank Card, but current cardholders will still keep full use of the card, so it's a possibility.

There's been no official notification from Chase that any of the business credit cards currently not on site are actually discontinued, meaning you should theoretically be able to product change to these cards as normal. When we first received reports about the missing cobranded business cards in April 2020, I could still find application landing pages for both through Google. However, during my most recent search, I came up empty.

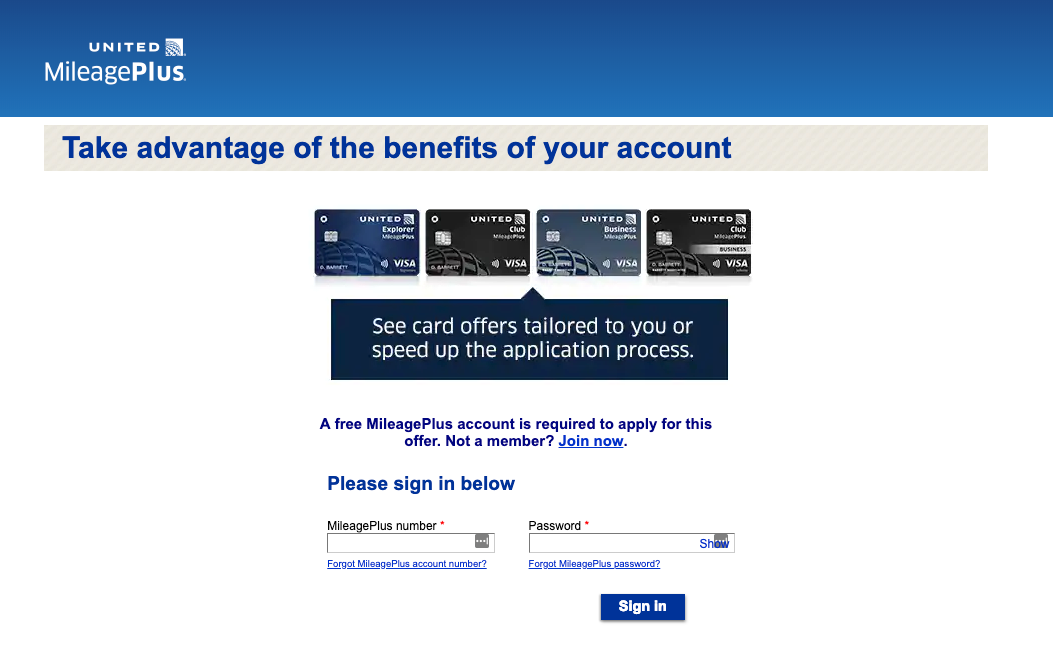

I did find this regarding the United cobranded cards, which makes it seem like you can apply for the card so long as you log in. But I logged in with my MileagePlus information and was sent to a landing page that said that card was not currently available to me. You might have better luck, but there is no guarantee.

The most likely explanation is that Chase has temporarily pulled these from the site to curb new applications during the current economic downturn.

The temporary removals of the Slate (at least to online applications) and TravelBank cards are not entirely surprising. The Chase Slate is a low-tier credit card that doesn't earn rewards and the TravelBank card is United's no-annual-fee option. The Slate especially has historically been an easier credit card to be approved for from a credit score standpoint, and issuers across the board are looking to mitigate risks during the current economic climate. But the other card removals are a bit more surprising. Both business cards carry an annual fee and generally appeal to business owners with good credit scores.

How this affects you

This affects business owners more than anything else. While the Chase Slate is a solid no-annual-fee card option for those looking for a balance transfer card, it's not a large draw for points and miles earners. And if you're flying with United frequently enough to warrant a cobranded card, you'll likely be better off with the United Explorer Card.

The other two cards currently missing in action could be of value to business owners who want to rack up points to travel once pandemic concerns have subsided.

The Southwest Rapid Rewards Premier Business Credit Card even earns points that count toward the Companion Pass. Since not many business travelers are likely going to hit that 100-flight requirement for the pass, credit card spending is the more realistic way to earn 2021 Companion Pass status this year. For those who wanted to apply for a Southwest small business card, the Southwest Rapid Rewards Performance Business Credit Card is still available. It's arguably the more valuable Southwest credit card and still only charges a manageable $199 annual fee.

Meanwhile, the United Club Business Card can now earn up to 4,000 Premier Qualifying Points (PQPs) per year toward elite status (though to be fair, earning all 4,000 PQPs does require significant spending on the card). United does still list the United Business Card as open to applications on the Chase site, but you'll be required to sign into an eligible existing Chase account to apply.

Related reading: 7 credit card rules ever business owner should follow

Business application process changes

The negative changes don't stop there for small business owners. In April, Doctor Of Credit reported that Chase was requiring annual business revenue (rather than letting you put $0) and business established date (rather than asking for a more vague "years in business"). Now, it appears Chase is continuing to add restrictions to business card applications.

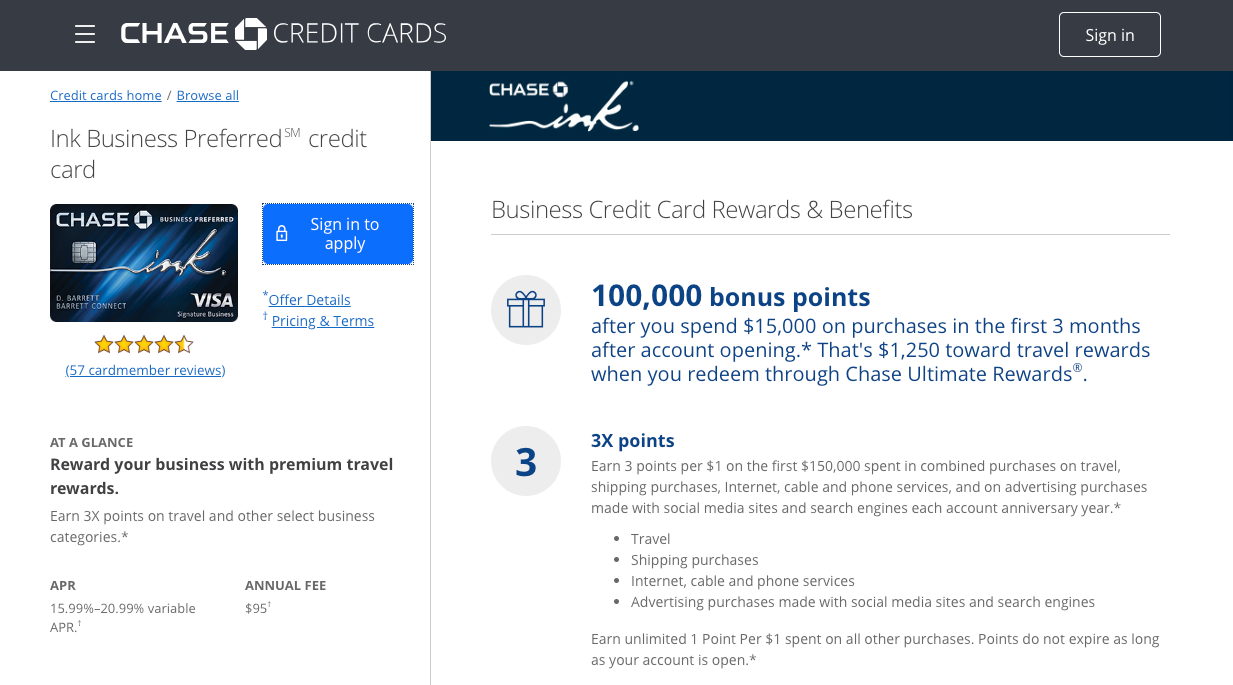

For all of their currently available small business credit cards, you have to sign in to a Chase account before you can go through the application process. Now, I did sign into my personal Chase account (I don't have any Chase small business cards), and that sent me to an application with some of my information pre-filled.

So, it doesn't seem like you have to be an existing business account holder, just a Chase credit account holder in general. I do have a friend who has a personal Chase checking account (but not any credit cards), and she was unable to use her login credentials to get to the application page. So, you'll likely need to be a credit card holder or business banking customer in order to apply.

Doctor of Credit has also recently reported anecdotal evidence of Chase tightening the approval criteria of small business credit card applications, citing "insufficient balance in deposit and investment accounts with us" as a common reason for denial.

Chase isn't the first issuer to give preference to existing account holders – Bank of America is notorious for this. But it does make things harder for small business owners hoping to jump into earning Chase Ultimate Rewards right now.

Related reading: Do I need a business to get a business credit card?

How this affects you

This is obviously a way for Chase to mitigate the risk of taking on unknown applicants. It makes sense when you look at it from their perspective. If you are a banking customer with Chase, they have access to your funds and can know whether you have the capital to pay your credit balances. And if you are a current Chase credit cardholder in good standing, then that shows them you are more likely to be a trustworthy borrower.

However, these new restrictions do put non-Chase customers at a severe disadvantage. If you are a business owner, it might be worth opening a Chase business banking account if you really want to apply for a Chase small business credit card. You can also start with a Chase personal credit card before trying to apply for a business card in the coming months.

Bottom line

Most of these changes are likely temporary while the economy is in a downturn due to the coronavirus pandemic. Restricting which cards are open for applications and focusing on developing deeper relationships with existing customers is a way for banks to have more control over the risk they are taking on. And Chase has certainly made efforts to appeal to existing cardholders, adding many temporary (and one permanent) additions to help cardholders utilize their travel cards during a time when they are likely staying at home.

Unfortunately, I predict that we'll see these types of changes extend beyond just business applications as we head deeper into this recession. Credit limits are likely to decrease, new applicants are likely to be subject to higher application criteria, and approvals, in general, will likely be harder to come by for anyone with a sub-700 credit score or past negative marks on their accounts.

This doesn't just apply to Chase cards. We've seen in the past that banks across the board are less inclined to open new lines of credit during an economic downturn. While it won't last forever, it will likely make opening new cards harder in the coming months.

Beginners to the credit card game will be the hardest hit. Those with long credit histories, excellent credit scores and existing banking relationships may not see the same effects of issuers tightening approval criteria. But young professionals, new business owners and others who are just starting out with credit cards may find it harder to open lines of credit for the duration of the recession.