Credit cards 101: The beginner’s guide

Editor's Note

Here at TPG, we love credit cards. We've experienced the power of redeeming credit card rewards, and we want to help everyone else have that great experience.

But if you're new to the world of credit cards, reading a credit card application (or even a review) can make you feel like you missed a course somewhere everyone else appears to have taken. If that's you, you're in the right place.

Below, we're taking the mystery out of credit cards. We cover everything from terms to types of credit cards and even breaking down a credit card bill. So settle in, maybe grab a notepad, and let's get into it.

Credit card debt

Before we go over anything else, it's important to note that while we're huge fans of credit cards at TPG, we never recommend carrying a balance from month to month. Carrying a balance means you'll be charged interest, which costs you far more than the value you'll get from any rewards you earn.

If you're considering a credit card, first make sure you have a plan to stay within your budget and pay off your balance each month. Never charge a purchase to a credit card unless you're 110% sure you can pay it off when your bill is due.

Credit scores

A credit score is a number — usually between 300 and 850 — that potential lenders use to determine their risk in lending you money.

Your credit score is made up of multiple factors, including payment history, the amount you owe and new credit opened. To build and keep a good credit score, you must borrow and pay it back on time. Using your credit card and paying your balance in full each month is a great way to improve your credit score.

When you apply for any type of credit, including a credit card, the potential lender will check your credit score to help them decide whether or not to approve your application. Typically, the best rewards cards require good to excellent credit scores for approval.

However, if your score is less than stellar, don't worry. We can show you how to improve your credit score and how to earn rewards while you're improving your credit.

Related: How to check your credit score for free

Debit vs. credit cards

When you use a debit card, money is pulled directly from your bank account to cover your purchase. That's why your $1,000 purchase will be declined if you only have $500 in your bank account.

However, when you use a credit card, you borrow money from the credit card company to make your purchase. When you pay off your balance, you're paying them back for your loan. If you fail to pay within the given time frame (typically around a month), you'll be charged fees and interest, and your credit score could drop.

The main benefit of using a debit card is that it keeps you from overspending. If you use a credit card responsibly, however, you'll earn rewards, get additional benefits and improve your credit score.

Related: Why a credit card is a smarter choice than a debit card

How to read your credit card bill

The terms, dates and different numbers on a credit card bill can make reading one feel like a decoding activity. However, the good news is that the code can be easily broken by understanding some key terms.

First, let's clarify the terms "bill" and "statement." Before online banking, cardholders received a paper statement (also called a bill) in the mail each month. That statement would outline the cardholder's charges for the billing period (the time since the last bill), statement balance (amount the cardholder charged during the billing period), minimum payment amount and payment due date.

Now, we have the luxury of checking our accounts online at any time. We still have statements that reflect our billing periods, but we can also see the transactions we've made since our last statement. This extra information is nice, but it can make things a bit confusing.

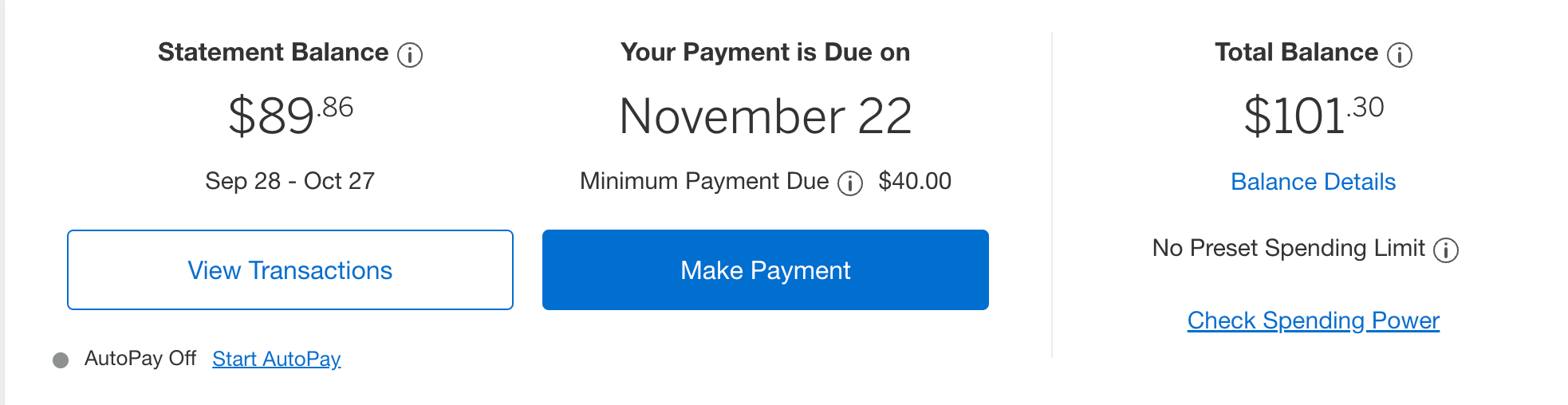

Here's a breakdown of what you might see when you log in to your online account:

The statement balance is the amount charged during your most recent billing period. You must pay this amount by the due date to avoid being charged interest or late payment fees.

The due date for your billing cycle depends on your card (you can find this in your card's terms and conditions).

In the example above, the cardholder must pay their statement balance of $89.86 by the Nov. 22 due date to avoid fees.

The minimum payment is the lowest amount you can pay by the due date to avoid being charged a late payment fee. However, if you only pay the minimum payment (or anything lower than the full statement balance), you'll carry a balance over to the next billing period and be charged interest on that amount.

The "total balance" refers to the entire amount that you owe on your card: the statement balance from the previous month, along with any charges that have been made since that billing cycle closed. In this example, the cardholder has charged $11.44 since the closing date, so the total balance is the statement balance of $89.85 plus the recent charges of $11.44. The cardholder can pay the total balance, but they can also just pay the statement balance and still avoid paying any fees. If they do this, the $11.44 will show up on the next bill, which they'll have to pay the next month.

Another number you'll likely see is "available credit," which is the amount left in your credit limit. This number will fluctuate as you pay off your balance or charge more to your balance. For example, if this user's credit limit were $4,000, their available credit would be $3,898.70 (the total balance of $101.30 subtracted from the credit limit of $4,000). Avoid maxing out your credit limit, as your card may be declined or charged an over-the-limit fee.

Related: After 15 years, why the Chase Sapphire Preferred should still be your first rewards card

Rates and fees

Now that you understand how to pay your credit card bill, let's review all the essential fees a credit card company might charge.

- Annual percentage rate (APR): The interest rate charged for the entire year. There are various types of APRs, including balance transfer, cash advance, penalty and purchase APRs. The most common type of APR is your purchase APR. This is the monthly interest rate that's added to your credit card balance if you do not pay your statement balance on time.

- Introductory APR offer: A reduced APR for a defined period can help you avoid additional interest charges on purchases and balance transfers.

- Annual fee: The cost of owning your card, charged once per year. Some cards have no annual fees, while others can charge up to $895 (or more) per year.

- Foreign transaction fee: The amount charged to your account when paying with a foreign currency. Some credit cards waive foreign transaction fees, while others charge fees. This is typically 3% of each transaction.

- Late payment fee: The amount charged to your account when you fail to pay the minimum payment by your payment date. In addition to the penalty APR charged to your balance, you'll also be charged a late payment fee.

- Over-the-credit-limit fee: The amount charged to your account when you exceed the credit limit defined on your card.

- Return payment fee: The amount charged to your account when the payment method you provided for your credit card statement fails or bounces for reasons such as insufficient funds, account freezes or closures.

Related: How to choose a credit card with 0% APR

Types of credit cards

If you're new to credit cards, the sheer volume of options can feel overwhelming. It helps to narrow your search by first determining which type of credit card you want.

Here are the most common credit card types.

General travel

These credit cards earn travel rewards and come with travel perks that aren't tied to any airline or hotel brand. They typically earn transferable rewards, which are our favorite type due to their high value and flexibility.

These cards also usually come with general travel benefits, such as travel insurance, TSA PreCheck/Global Entry credits and airport lounge access.

For our top picks, check out our full list of the best travel credit cards.

Related: Why transferable points are worth more than other rewards

Airline

Airline credit cards are cards tied to one specific airline.

You'll earn rewards in the form of that airline's points or miles and get perks tied to the airline, such as free checked bags, automatic elite status and airport lounge access.

Related: Best airline credit cards

Hotel

Hotel credit cards are tied to a specific hotel brand.

You'll earn rewards in the form of points that you can use for any hotel within that brand, and you'll get perks like free nights and automatic elite status.

Related: Best hotel credit cards

Cash-back

Cash-back cards usually have the simplest rewards to earn and redeem. With a cash-back card, you'll earn a percentage of your purchase back in rewards.

Then, you can redeem your rewards for cash — either as a statement credit, a check in the mail or a direct deposit into an eligible checking or savings account, depending on the issuer.

Related: How to choose a cash-back credit card

Secured

A secured credit card is a good option if you have limited credit history or a low credit score. With a secured card, you'll pay a security deposit when you open the card, which functions as insurance for the credit card company.

Generally, these don't earn rewards, but they're a good way to build your credit and increase your chances of being approved for a rewards credit card later on.

Related: Best secured credit cards

Student

A student credit card is for — you guessed it— college students. They're designed to help students build credit, good financial habits and a relationship with a bank so they'll be ready for a more advanced credit card when they graduate.

These tend to earn minimal rewards, but they're an excellent option for students to ease into the world of credit cards.

Related: The best credit cards for college students

Authorized user

An authorized user is someone who has been added to an existing credit card account by the primary account holder. An authorized user has full spending abilities on their credit card, but usually has limited benefits.

If you're having trouble getting approved for a credit card, being added to someone else's account as an authorized user may help your credit score.

Related: Have good credit? Share it with an authorized user

Earning rewards

Each rewards card earns a type of rewards "currency." The American Express® Gold Card earns transferable American Express Membership Rewards points, for example, while the Citi® / AAdvantage® Executive World Elite Mastercard® (see rates and fees) earns American Airlines AAdvantage miles, and the Hilton Honors American Express Surpass® Card earns Hilton Honors points. These currencies have different values, so check out our latest TPG valuations chart to see what each rewards type is worth.

Your card's earning rate and spending habits determine the amount of rewards you'll earn. Some cards earn at a fixed rate, meaning they earn the same amount on all purchases. The Capital One Venture Rewards Credit Card, which earns 2 Capital One miles per dollar spent, and the Citi Double Cash® Card (see rates and fees), which earns 2% cash back on all purchases (1% when you buy and 1% as you pay), are both examples of cards that earn at a fixed rate.

Other cards have bonus-earning categories. The Chase Sapphire Preferred® Card (see rates and fees), for example, earns 5 Ultimate Rewards points per dollar on travel purchased through Chase Travel℠, 3 points per dollar spent on dining (including takeout and eligible delivery services), popular streaming services, gas and electric vehicle charging and vacation homes at top brands* and online grocery purchases (excluding Walmart®, Target® and wholesale clubs) as well as 2 points per dollar spent on other travel purchases. It earns 1 point per dollar spent on all other purchases.

*Brands are: Airbnb, Vrbo, Plum Guide, HomeAway, Homestay.com and Vacasa.

Additionally, many rewards cards include welcome bonus that can be worth hundreds or thousands of dollars in value. To earn the welcome bonus, you'll need to spend a certain amount of money in a given period of time.

Related: The best credit cards for each bonus category

Credit card best practices

You may have heard that credit cards should be avoided because they can get you into serious trouble. Although you won't hear us tell you to avoid credit cards, we only condone responsible credit card use.

Here are some of the best credit card practices that we live by.

Always pay your balance on time and in full. It may seem like we're heavily emphasizing this point, but it's for good reason. Not only will you negate any points and miles you earn if you start to accrue interest charges, but carrying a balance can get you into significant debt quickly.

Credit cards are not free money, so never charge more than you can afford. Similarly, remember that you'll owe the statement balance on your card each month. Budget and manage your credit wisely so your finances don't get out of hand.

Understand credit card application restrictions. You may be tempted to dive into the deep end of credit card rewards immediately, but it's best to take it slowly. In addition to giving yourself time to find a credit card budget system that works best for you, know that some issuers have their own set of restrictions. It pays to be thoughtful and have a longer-term plan before you apply for a credit card.

Wait at least three months (ideally, six months or longer) between card applications. Opening new lines of credit affects your credit score, and applying for new cards too quickly can be a red flag. Pace yourself by earning a card's welcome bonus and taking some time to learn how well the card matches your lifestyle. Then you can choose your next card based on what best complements it (and any others in your wallet).

Think twice before canceling a credit card. As you add more cards to your portfolio, you might be tempted to cancel the ones you aren't reaching for as often. However, if a card has no annual fee, there's no harm in keeping the card in your wallet — potentially forever. Length of credit is a factor in your credit score, so keeping your earliest cards open helps increase your credit history and, therefore, your credit score.

Related: TPG's 10 commandments of credit card rewards

Building a points-and-miles strategy

Now that you have a baseline understanding of credit cards, it's time to choose your card.

Don't feel like you need to have a strategy in place right now. If you're overwhelmed by the types of rewards, you can start small with a cash-back card to solidify your good credit habits and enjoy simple rewards redemptions.

But if you do have a dream trip in mind, you can set your sights on a travel rewards card that will help make that dream a reality.

When you're ready to think about a points-and-miles strategy, check out our TPG guide to getting started with points and miles to travel.

Related: Key travel tips you need to know — whether you're a first-time or frequent traveler

Bottom line

Congratulations! You're armed with the terms and knowledge you need to research, apply for and responsibly use a credit card.

Now, take a look at our recommendations of the best first credit cards and use the knowledge you've gained here to help you choose the one that fits your spending habits and rewards goals. We'll be here for you as you go through every step of your credit card journey.

Related: The best starter travel credit cards