Should I purchase rental car insurance for a rental car booking?

Update: Some offers mentioned below are no longer available. View the current offers here.

You're standing at the rental car counter filling out your paperwork when the representative asks you, "Do you want rental car insurance today?" You may be put on the spot. What should you say?

This guide will help you understand how rental car insurance works so that you know when to rely on your credit card rental car benefits, go through your existing car insurance policy or purchase a rental-specific policy.

Car rental companies cannot require you to purchase car rental insurance when you pick up your car, according to Ryder Pearce, CEO and founder of Skip, a company that helps individuals navigate government services and information. And most car rental companies do not require you to have proof of existing car insurance when getting a car.

However, rental companies can require a deposit for the car, Pearce told TPG, and have you pay for the booking with a credit card. (These companies don't require a credit card when booking.)

What is rental car insurance?

As the name states, this type of auto insurance differs from the policy you hold for your current car. Rental car insurance protects your temporary vehicle for the duration of your booking.

Rental car policies typically have multiple components, and you can choose which ones are best for you. Some of these names can vary slightly from insurance company to insurance company, but here are the basics of what they cover:

- Collision damage waiver (CDW)

This coverage prevents the rental car company from holding you responsible for repair or replacement costs if your rental car is damaged in your possession. Collision damage includes anything from a dent in the bumper to a full-on wreck; you will not have to pay for any of those fixes. It's worthwhile to note that rental agencies purchase damage insurance on the vehicles they own, according to Riley Spiller, a founding partner of insurance brokerage Noble House. So if you damage the car without CDW coverage in place, the rental company's insurance will pay for the expenses upfront, and you will have to reimburse the rental car company for those costs. - Supplemental liability protection (SLP)

Unfortunately, collision damage only covers any expenses related to the vehicle itself. If you are involved in an accident that affects other people, you could be liable for medical expenses and property damage from the other party. SLP covers some or all of those costs, depending on the amount of coverage you purchase. - Personal accident insurance (PAI)

The first two types of coverage have to do with expenses related to the rental company's property or a third party's damages and injuries. PAI, on the other hand, pays for any medical expenses that you and your fellow passengers may incur in the event of an accident. - Personal effects coverage (PEC)

Finally, PEC covers the cost of your possessions in the event of car theft.

Do I need rental car insurance to get my car?

You are not obligated to purchase any of the above types of rental car insurance from your rental agency. If you have an existing current auto policy or a premium credit card, you may already carry enough coverage for your car rental needs.

You also don't have to purchase rental car insurance through your rental company itself. Several companies focus exclusively on rental car coverage, including Bonzah, InsureMyRentalCar.com and Sure. Allianz is a more traditional insurance company that also offers a plan just for rental car coverage.

Related: TPG's comprehensive guide to independent travel insurance

Make sure you familiarize yourself with the laws about how much insurance coverage you have to carry, both in your home state as well as your destination(s) and any other states you travel through. You can use this state-by-state guide from rental car insurance company Bonzah to help you figure out a state's minimum liability requirement, which is the dollar amount you must pay to someone who is injured or has property damage from an accident that's your fault.

What can I expect from a rental car insurance plan?

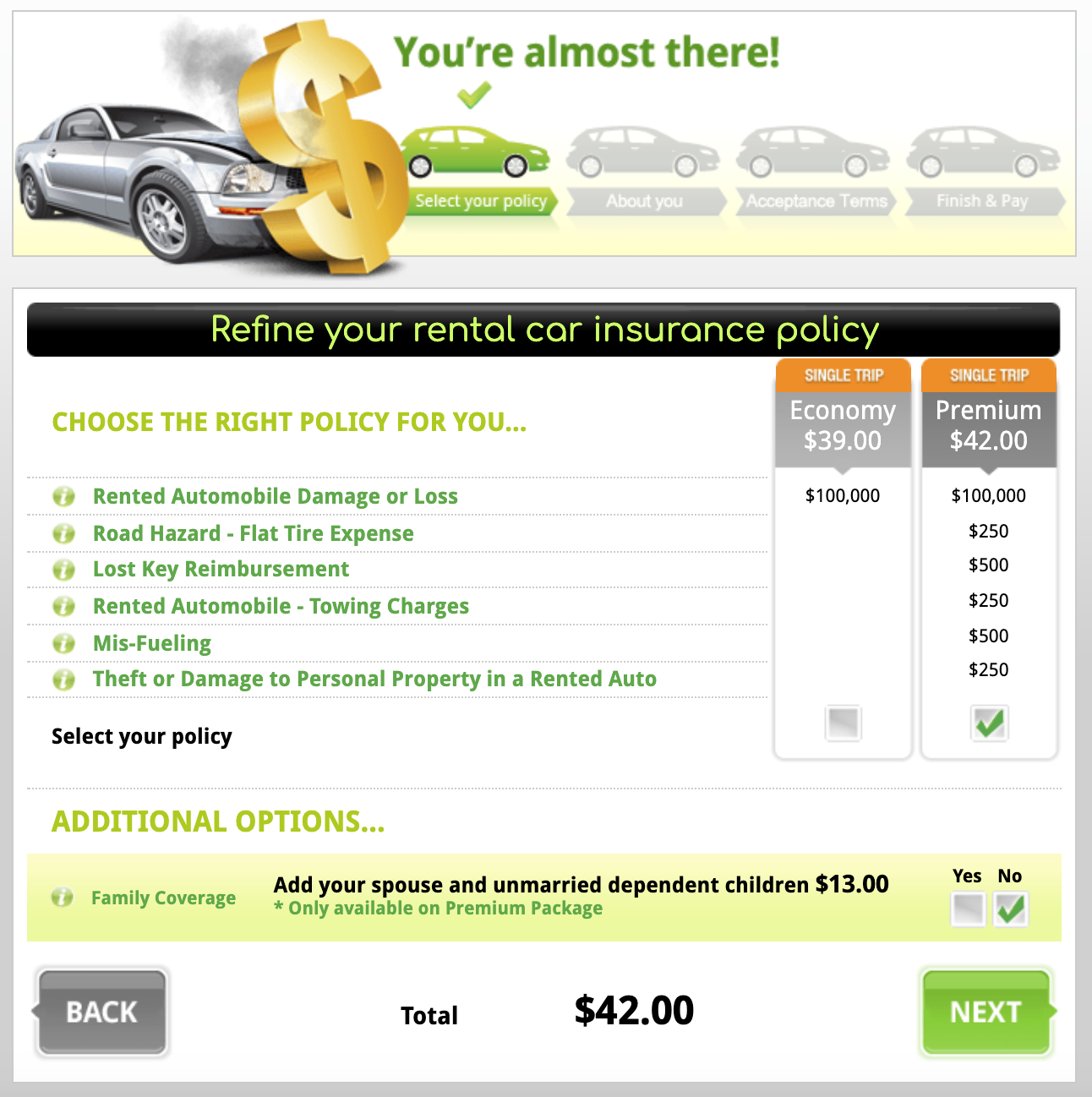

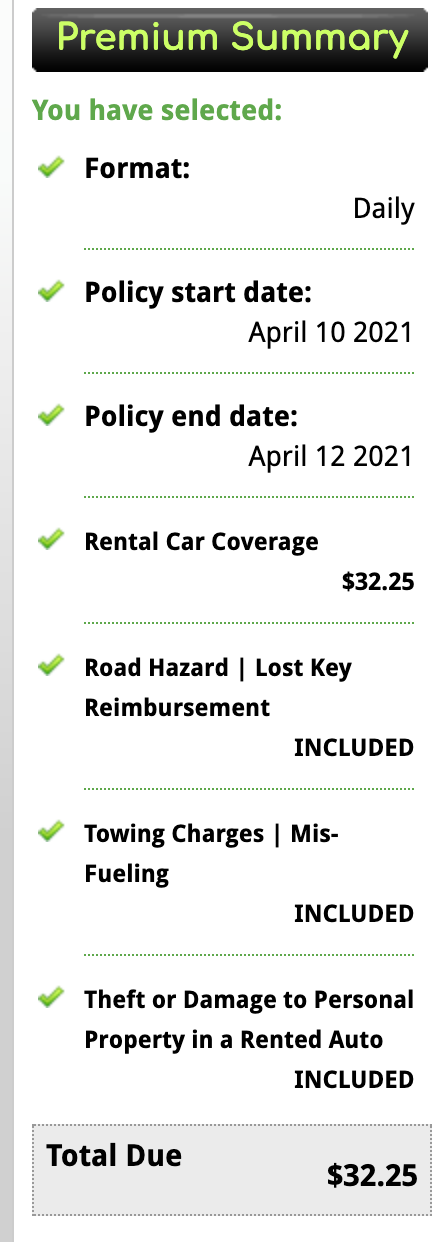

Purchasing a rental car insurance plan is quite straightforward. You can generate a quote online in minutes by submitting your basic contact information as well as your location(s) and dates of travel.

Here's an example from InsureMyRentalCar.com:

From there, you'll typically see a few price points that show a breakdown of different coverage included in the quote, and then you'll need to fill out the online form for your address and other personal information, a short four- or five-step process.

Does my current auto insurance policy cover my car rental?

The answer to this question is entirely dependent on your individual insurance policy. Your best bet is to reach out to your provider before your trip to see what coverage may be included on your current plan, especially if you plan to travel overseas. If you're not sure, or if your maximum limit for rental coverage is very low, you should look into purchasing a rental car insurance plan or double-checking your credit card benefits.

What's the difference between primary and secondary coverage?

A credit card with rental car insurance typically offers either primary or secondary coverage. Primary insurance applies before any other type of coverage, such as your standard auto insurance, travel insurance or a homeowners policy in the event of theft. In contrast, secondary insurance kicks in after you've filed a claim with your other insurance companies.

Related: Why I'll always check the VIN before renting a car

Both primary and secondary coverage usually have limits on the maximum dollar amount you can claim for an incident, so make sure you've evaluated those limits to ensure they meet or exceed the value of your rental car in case of damage.

In some cases, secondary policies become primary policies if your main insurance coverage doesn't apply. If your everyday auto insurance policy doesn't cover international rentals, your secondary coverage from your credit card will automatically become your primary policy since you don't hold any existing policies that would support a claim. And if you don't own a car and thus don't have an auto insurance policy, your secondary coverage benefits will serve as your primary coverage on car rentals.

Can I use credit card benefits for rental car coverage?

Many credit cards include rental car coverage as part of your benefits. The Chase Sapphire Preferred Card is one of the best all-around credit cards because it offers primary coverage on car rentals. In contrast, American Express does not offer primary coverage on many of its cards.

Some of our top favorite cards for car rentals include:

- Chase Sapphire Reserve

- Ink Business Preferred Credit Card

- Ink Business Cash Credit Card

- Ink Business Unlimited Credit Card

- United Explorer Card

- United Business Card

- Capital One Spark Miles for Business

Note that there are some important details in the rental coverage fine print. For example, the Chase Sapphire Preferred Card (and its big brother, the Chase Sapphire Reserve) rental car benefits only extend to bookings of 31 consecutive days or less for international reservations. So if you need a longer-term rental, you might consider purchasing an independent rental car insurance plan.

There are some ways you can work around this issue. For instance, TPG's Scott Mayerowitz successfully booked a rental car for 110 days straight in summer 2020. However, he was able to get his rental car agency to create four separate reservations that would allow him to keep the same car but appear as four different transactions to meet his credit card maximum requirement.

Related: Renting a car? These are the cards you need

Do credit card rental benefits cover damages to other people or myself?

Remember the supplemental liability protection and personal accident insurance coverage types mentioned above? Your credit card benefits do not include either SLP or PAO. This means you're responsible for paying for any damages to someone else's car and personal property, as well as medical expenses for yourself, your passengers and any other affected victims.

Related: Which rental car company is right for you?

For instance, auto collision benefits from the Chase Sapphire Reserve do not insure costs from injuries sustained by anyone or anything inside or outside of the vehicle, nor does it pay for loss or theft of personal belongings.

So once again, check the fine print on your current car insurance policy to see what's covered. If you need additional protection, look into purchasing a rental car insurance plan, just for peace of mind.

Can I still use my credit card benefits if I purchase insurance from my rental car company?

You cannot utilize both your credit card auto collision benefits and an insurance policy from your rental car company, according to Chase's complete guide to card benefits. Purchasing rental coverage will cancel out the credit card benefits.

What else do I need to know about using credit card auto collision insurance?

Credit card insurance typically won't cover claims with the following issues:

• Any violation of the auto rental agreement.

• Vehicles that are not rented from a rental agency.

• Personal liability.

• Expenses covered by your insurer, employer or employer's insurance.

• Theft or damage due to intentional carelessness, illegal and contraband activities, or driving under the influence of drugs, intoxicants or alcohol.

• Wear and tear, gradual deterioration or mechanical breakdown.

• Items not installed by the original manufacturer.

• Damage due to off-road operation of the rental vehicle (unless designed for that purpose).

• Theft or damage due to hostility of any kind (including, but not limited to, war, invasion, rebellion, insurrection or terrorist activities).

• Confiscation by authorities.

• Vehicles that do not meet the definition of covered vehicles.

• Theft or damage reported more than 60 days after the date of the incident.

• Theft or damage for which a claim form has not been received within 100 days from the date of the incident.

• Theft or damage for which all required documentation has not been received within 365 days after the date of the incident.

How much insurance coverage do I need?

If you decide to purchase an independent rental car coverage plan, make sure you know the legal minimum requirements for your insurance, both in the state where you book as well as for any other states you might travel through. But you also might want to upgrade your plan, just in case.

Related: The 10 best ways to redeem your points and miles for a car rental

For instance, you could purchase a bare-bones policy for a trip to Arizona that would pay up to the state's minimum requirement of $15,000 for each person injured in an accident of your causing. But if the injured person's medical bills cost more than $15,000, you'd need to pay the rest of their expenses out of your own pocket.

So in many cases, it makes sense to spend the few dollars extra to get the maximum coverage.

At a minimum, you should seek out a policy that covers some of the following costs for your protection:

- Coverage for damages and medical expenses to a third party if you're at fault in a collision.

- Coverage for damages to your own vehicle and potential medical expenses for you and any passengers.

Related: 11 common car rental mistakes

This checklist applies whether you go through your existing auto insurance, purchase a plan through your rental agency or rely on your credit card benefits.

Does my rental car insurance cover international travel?

The answer to this question depends on the policy you decide to use: your existing auto policy, an independent coverage plan or your credit card benefits.

As mentioned above, your existing policy will specify whether or not your international rental is covered. If you aren't sure, reach out to your provider for specifics. An independent coverage plan establishes your rental destination upfront, so your quote will automatically include international coverage.

Your credit card's rental car benefits are a little bit more complex. These perks usually apply to international rentals as well as domestic rentals, with some exceptions. For example, Visa offers many credit cards that include domestic and international rental car insurance as part of your cardholder benefits. But the fine print in Visa's terms of services states that the issuer does not pay for theft or damage from rental reservations made in Israel, Jamaica, the Republic of Ireland or Northern Ireland.

Related: Why I'll never make this rental car mistake again

So before you rely too heavily on your credit card for international coverage, make sure you check the fine print for the credit card you plan to use to make sure your countries of travel are included.

Bottom line

There are a lot of situations where your credit card benefits will be more than sufficient for a car rental. However, you should definitely consider an independent rental car insurance policy if you think you might need additional coverage, such as when traveling under precarious weather conditions.

For Capital One products listed on this page, some of the above benefits are provided by Visa® or Mastercard® and may vary by product. See the respective Guide to Benefits for details, as terms and exclusions apply.