Money management for kids: How I used the Greenlight debit card to teach my son about finances

Update: Some offers mentioned below are no longer available. View the current offers here.

Growing up, the highlight of my week was getting my allowance on Friday night and blowing it all at the roller rink mere hours later. I didn't save a cent — and at the time, I didn't care.

Looking back, I wish I had managed my money a bit more responsibly. Sure, I have ample happy memories of winning the hokey pokey contest at the rink, but I could've saved up for something even bigger — and possibly more memorable — had I known how to conceptualize working toward a larger goal.

Fast forward to when my oldest son turned 7, and my husband and I decided he was old enough for a weekly allowance. We gave him $10 per week for cleaning the table after dinner, putting his laundry away and other household chores we bestowed upon him.

For the first few months, his attitude toward money was similar to my own as a child. Every Friday after school, he would beg us to go to Target so he could spend his entire allowance on a pack of Pokemon cards or a small Lego set.

Realizing he was making the same mistake I made when I was younger, we sought a different approach. If he could more easily keep track of his money and understand how much he had, it'd feel just as "real" to him as holding cash in his hands.

We started researching debit cards for kids and ultimately settled on the Greenlight debit card. Here's why Greenlight's debit card stood out from the rest and how using it helped change my son's perspective on money.

The information for the Greenlight debit card has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.

Kids debit card options currently available

At TPG, we're not huge fans of debit cards for adults making everyday purchases, but they can be a great option for kids learning about money.

There are various debit cards geared toward kids available, each of which has its own pros and cons.

Chase First Banking: With Chase First Banking, kids ages 6 to 17 receive both a bank account and a debit card. There are no monthly service fees, and parents have access to tools for monitoring and controlling their child's spending. However, only current Chase checking account customers can sign up for the First Banking service.

Capital One Money: Like Chase First Banking, Capital One Money offers a bank account and a debit card for younger customers. Parents can use any checking account to fund their child's account, so it isn't a requirement to be a Capital One checking customer. Plus, there are no fees to open, no minimum balance requirements and no monthly service charges. However, unlike Greenlight, which has no minimum age requirement to open up a debit card account, this checking account is for kids age 8 and up.

GoHenry: A close runner-up to Greenlight, GoHenry differs from Chase First Banking and Capital One Money in that it does not have a bank account. Instead, it is a debit card that is linked to the parent's checking account. There's an app where you can manage your child's funds and kids can play games and take quizzes to improve their financial literacy. While robust, some of the features seem like a better fit for older kids, so some children (like my son) may be too young to take full advantage of what GoHenry has to offer. Another drawback: A monthly fee of $3.99 per child applies after a one-month free trial.

Related: Why my kids are authorized users on my credit cards

Why I chose Greenlight

In the end, Greenlight had everything I was looking for at a price I liked. While there's a cost associated with the base plan ($4.99 per month after a one-month trial), the fee includes debit cards for up to five kids. As a mom of three, I'll be tapping into those extra cards eventually, so I like that the price won't go up as I start paying out more in allowance money.

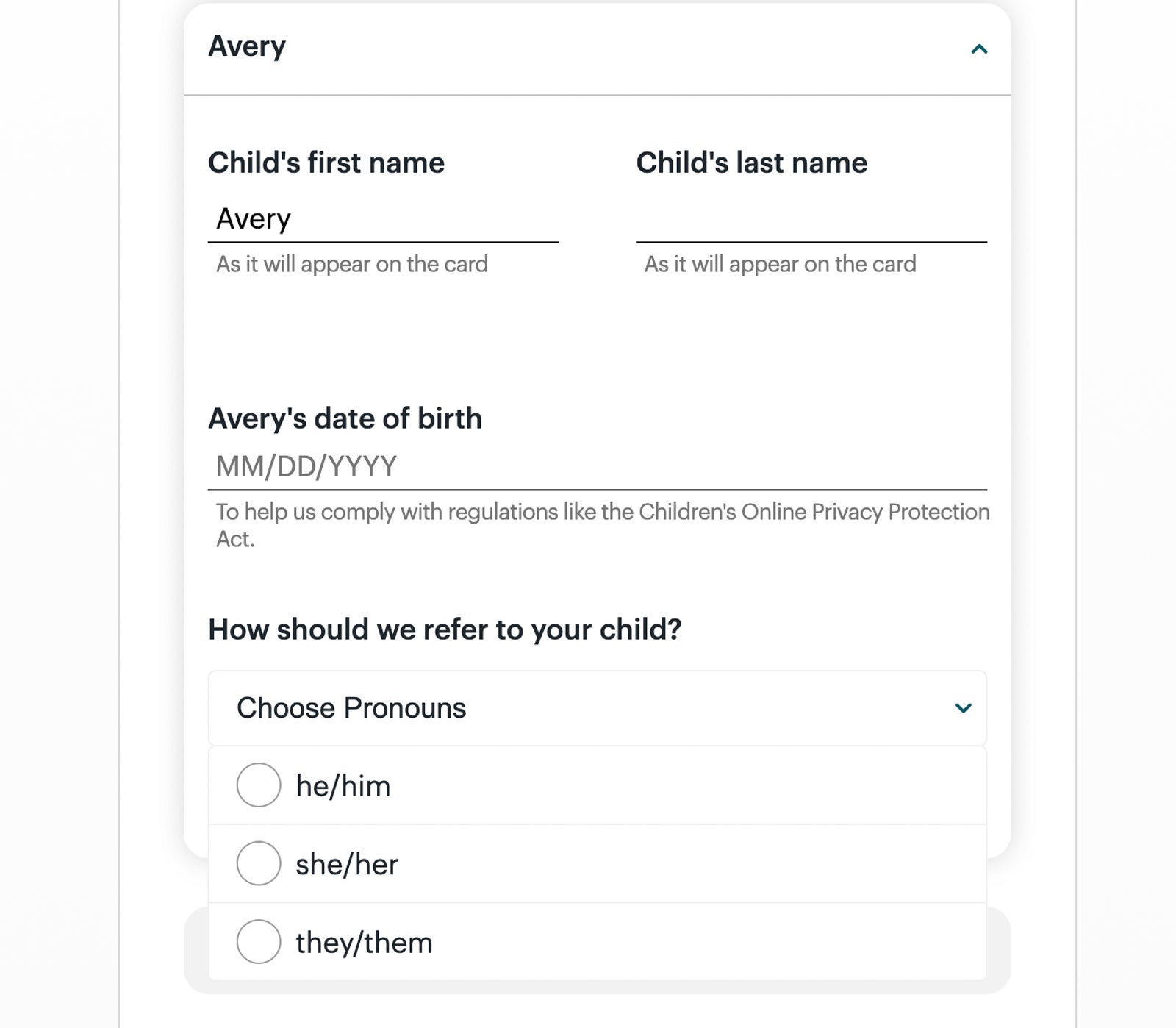

Greenlight first won me over with its use of inclusive pronoun options during the application process. It means a lot to me that they felt this detail was important, even if it doesn't have anything to do with money.

Additionally, the app is simple to use and aesthetically pleasing. I love that there are options to set category-based spending controls and that we have the ability to split his allowance between spending, saving and charitable donations.

For an extra $9.99, you can order a custom card with your child's photo on it, a cute upgrade that I've so far resisted the urge to get in an effort to teach my son the importance of saving money instead of spending more than necessary.

I also appreciate that Greenlight offers two higher-priced plans to account for more ambitious financial goals as kids get older. Greenlight + Invest costs $7.98 per month and includes all of the base plan features, plus an investing platform that lets kids invest in stocks and exchange-traded funds (with their parent's approval, of course). The other plan, Greenlight Max, covers all the benefits of the two lower tiers, as well as 1% cash back on purchases (which gets deposited straight into their savings account) and identity, cellphone and purchase protection in its $9.98 per month fee. I'll likely look into one of these upgraded plans once my other kids start using Greenlight.

How Greenlight works

It took about a week after filling out the application for my son's debit card to arrive. During that time, I set up my "parent's wallet." I linked my checking account and set it up to automatically add funds at the beginning of each month so my son would get his allowance without me having to think about it.

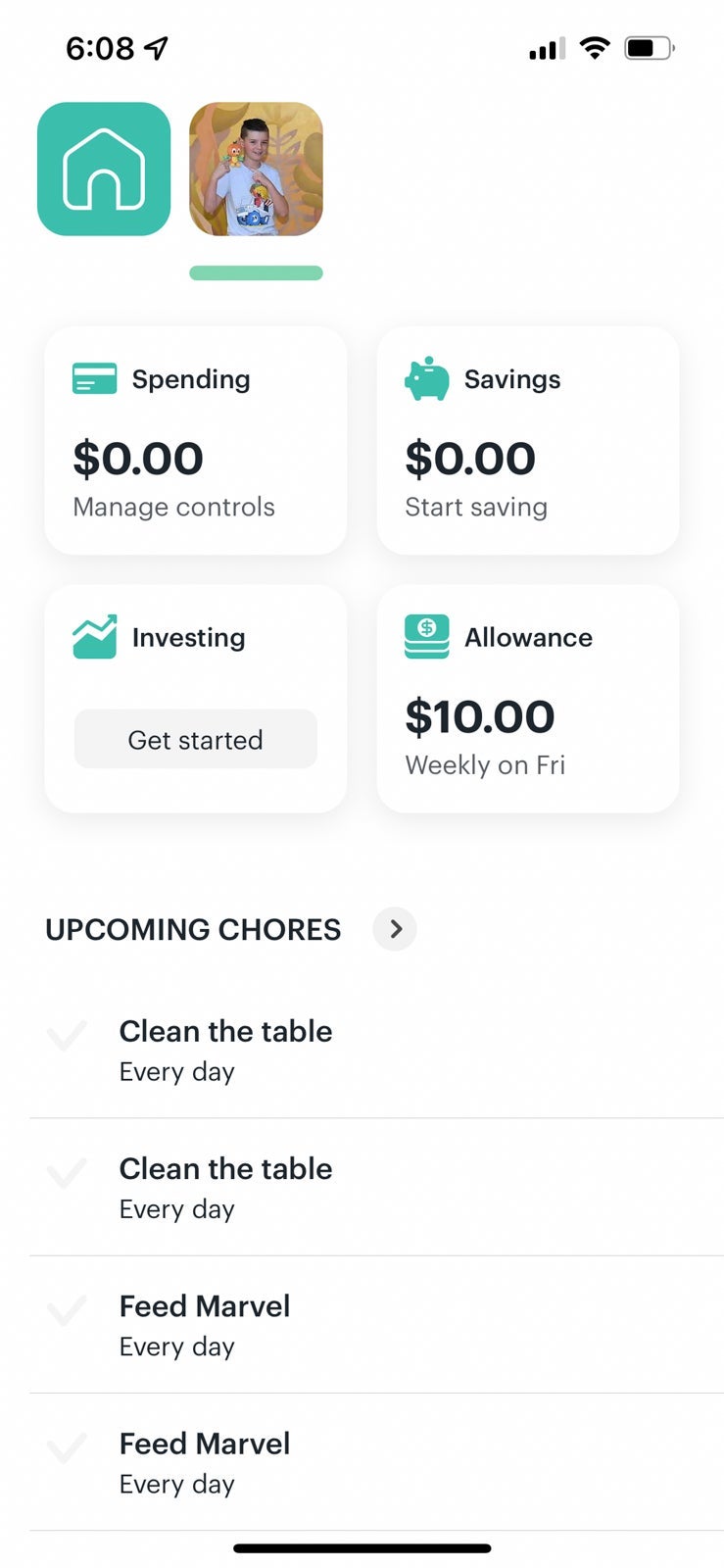

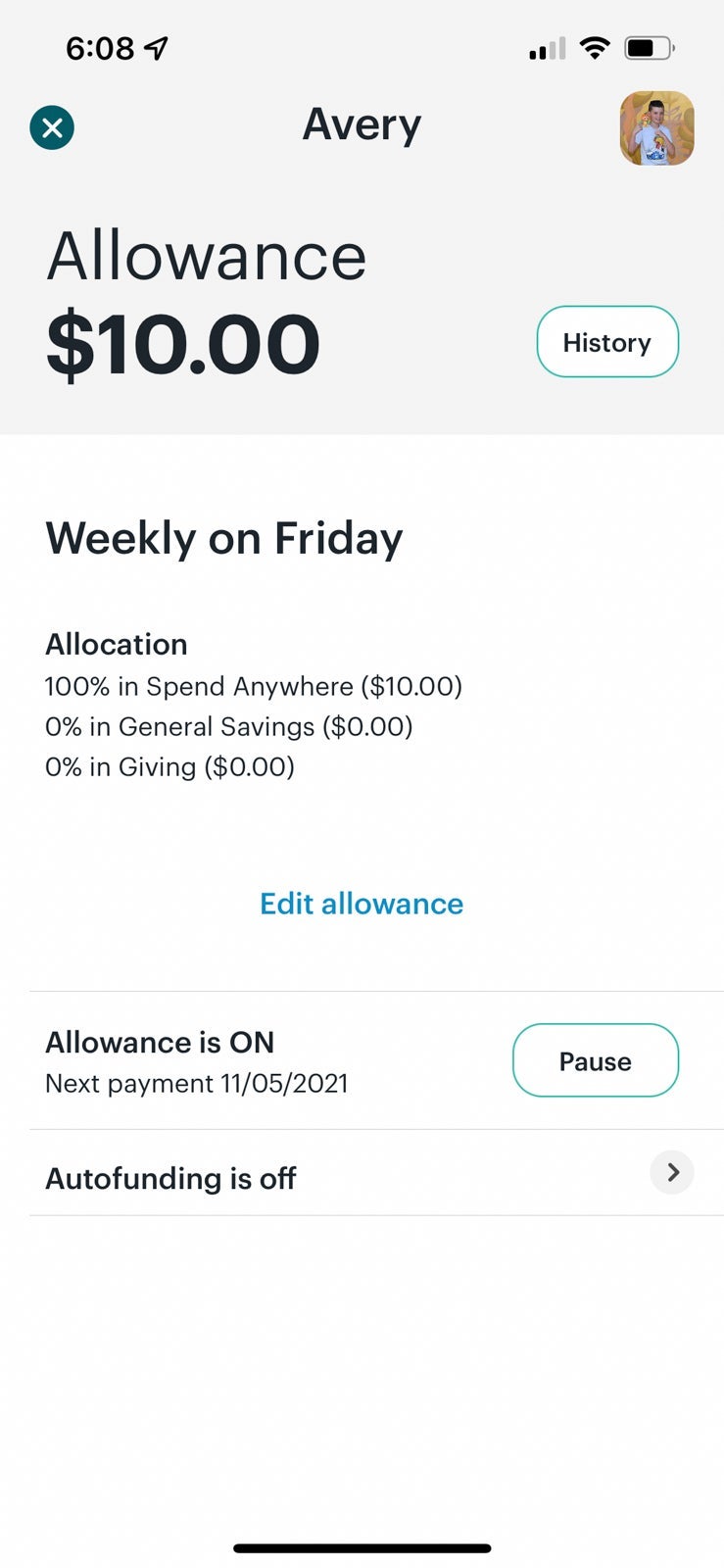

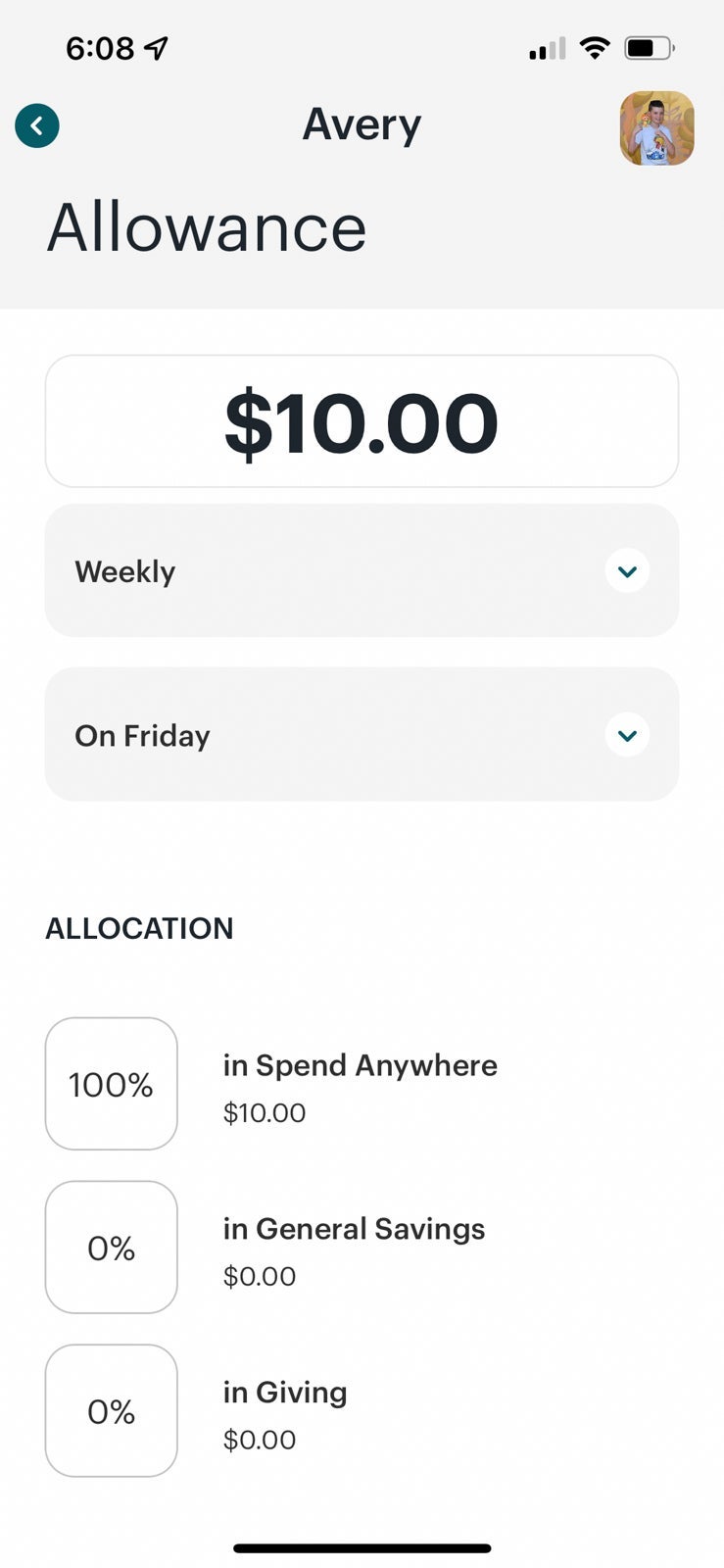

Every Friday, $10 is moved from my parent's wallet to my son's debit card account. I've set it up to put 70% into his spending category, 20% into his savings category and 10% into his charitable donations category. When he wants to know how much money he has to spend on a new toy or game, I can just open the app and show him.

Kids with their own electronic device can use the app to check off their daily and weekly chores, but since my son doesn't have one yet and I kept forgetting to mark his allowance tasks as complete, I dropped that feature.

When he received monetary gifts from family for Christmas, I deposited the money into my checking account and then added it to my parent's wallet in Greenlight in order to transfer it to his balance.

You can also set savings goals when your child is working toward purchasing a more expensive item. In our case, that item was a Hot Wheels Mega Garage, which he was excited to save for after I showed him that he only needed to set aside a few weeks of allowance on top of his Christmas money. I set up a savings goal in the app, and we watched as he moved closer to his goal.

Related: How to open a frequent flyer account for your kids

How our Greenlight journey is going

So far, Greenlight has been an amazing tool for my son. It has eliminated our frequent arguments about money, and he has learned some important lessons about savings and money management.

Now, with gentle reminders, he's understanding that when he doesn't have enough money in his account for a toy, he can't purchase it quite yet. If he handed his debit card to the cashier, it would be declined. As a result, I've noticed he's starting to make smarter purchase decisions, such as choosing a less expensive (yet equally fun) toy.

Bottom line

I would happily recommend the Greenlight debit card to other parents looking to go beyond the piggy bank for teaching lessons about earning and saving money.

My son has learned a ton about money management, so much so that I feel like he has a better understanding of money as a tangible asset now than he did when using cash. He's more inclined to save for what he wants instead of spending his money like it's about to burn a hole in his pocket.

Although he still requests a quick trip to Target for Pokemon cards from time to time, I'm confident that he's well on his way toward making smart financial decisions as an adult.