3 ways to pay without touching anything

Update: Some offers mentioned below are no longer available. View the current offers here.

In the past year, we've seen the full adoption of contactless payments, as the pandemic made us reduce the number of touchpoints we access on a day-to-day basis.

By limiting the amount of cash you handle — or by avoiding your physical credit card and wallet altogether — you're not just preventing yourself from coming in contact with someone else's germs; you're keeping others safe from yours as well.

Related: How to clean your credit cards

In this post, we'll go over the three ways to pay without ever pulling out your credit card or cash.

Pay ahead online or in-app

This is something you're probably used to when ordering online from places like Amazon and Uber Eats. Your cards are saved and all you have to do is check out. This is certainly one of the easiest and most common contactless payment methods. Many restaurants have adopted this order-ahead method as the new norm, eliminating contact while also streamlining the whole process.

I actually used this process earlier today when I ordered something last-minute at Target that I plan to pick up curbside later. Because my payment details are stored with my Target account, I was able to prepay for my order so that all I'll need to do when I arrive at Target is wait for my order.

Use mobile payment services

Mobile payment services like Venmo or PayPal allow you to safely transfer money directly from your bank account to third parties with a simple touch of a button. This eliminates the need to pull out cash or your card.

Related: You can now use PayPal and Venmo directly within the Amex app

And frankly, these services make the whole payment process much smoother. Many businesses like Seamless, GrubHub and UberEats have started to accept Venmo. It's also an option at many small, local businesses. PayPal is often an option during checkout at millions of online retail stores.

Use a mobile wallet

Mobile wallets work similarly to tap-to-pay cards, minus the credit card. Not to mention this method can sometimes be more rewarding. For instance, Apple tries to incentivize Apple cardholders to utilize Apple Pay by offering an extra 1% cash back on mobile payments. Another perk of Apple Pay is that you can load other loyalty programs into it, like Walgreens, so you don't have to punch in your phone number on the dirty payment terminal.

Related: Your guide to contactless payments — and the many benefits of using them

How other countries approach contactless payments

The U.S. has been unbelievably slow in adopting contactless payments. It wasn't until 2015 that U.S. retailers were required to accept EMV cards (i.e., credit cards with chips). Europe had been using the more secure technology for years before that. And it took even longer for U.S. banks to issue dual interface cards — also known as the feature that allows for contactless payments.

Although the U.S. lagged behind many parts of the world in issuing dual interface cards, the trend has gained steam domestically over the past few years. Many U.S. issuers have begun issuing dual-interface cards with contactless payment capabilities. I can say from experience that our payment terminals are far less efficient than those in countries including Australia and China, which have been using this method for years now. However, with the new expectation of less contact due to the coronavirus, we widely adopt these efficient practices from leading countries. Here's an idea of what we could expect:

Related: Best contactless credit cards: Tap to Pay

QR code payments

QR code payments are a popular payment method in China. This method allows customers to easily complete payments without any contact. TPG's previous writer, Ethan Steinberg, who lived in China until March 2020, shared the photo above from a food stall in Xi'an. All you have to do is scan in line and then pay while they make the food — it only takes a few seconds.

Tap-to-pay everywhere

On a recent trip to Australia, I was amazed at how seamless every payment was. I never once swiped my credit card. Instead, I tapped my Chase Sapphire Preferred Card and the transactions were completed within seconds. I was also pleasantly surprised with how widely accepted credit cards were. I'm so used to carrying around some extra cash for those cash-only spots, but I didn't run into that issue anywhere in Australia.

While the complete elimination of cash is a different issue on its own, I did appreciate how efficient the Aussies were with their payments. This is something that I hope is adopted here in the U.S. in the coming months.

Widespread adoption of tableside payments

We could soon see more widespread adoption of tableside payments at U.S. restaurants to avoid the mixture of cash and credit cards that constantly travel between the kitchen and the dining room.

By implementing tableside payments, guests could easily tap-to-pay and avoid contact with various other surfaces. This is something that many restaurants in Australia and countries in Europe currently implement. Not only is it super-efficient, but it's also much more secure for customers since you never lose sight of your card.

Touchless options in the travel sector

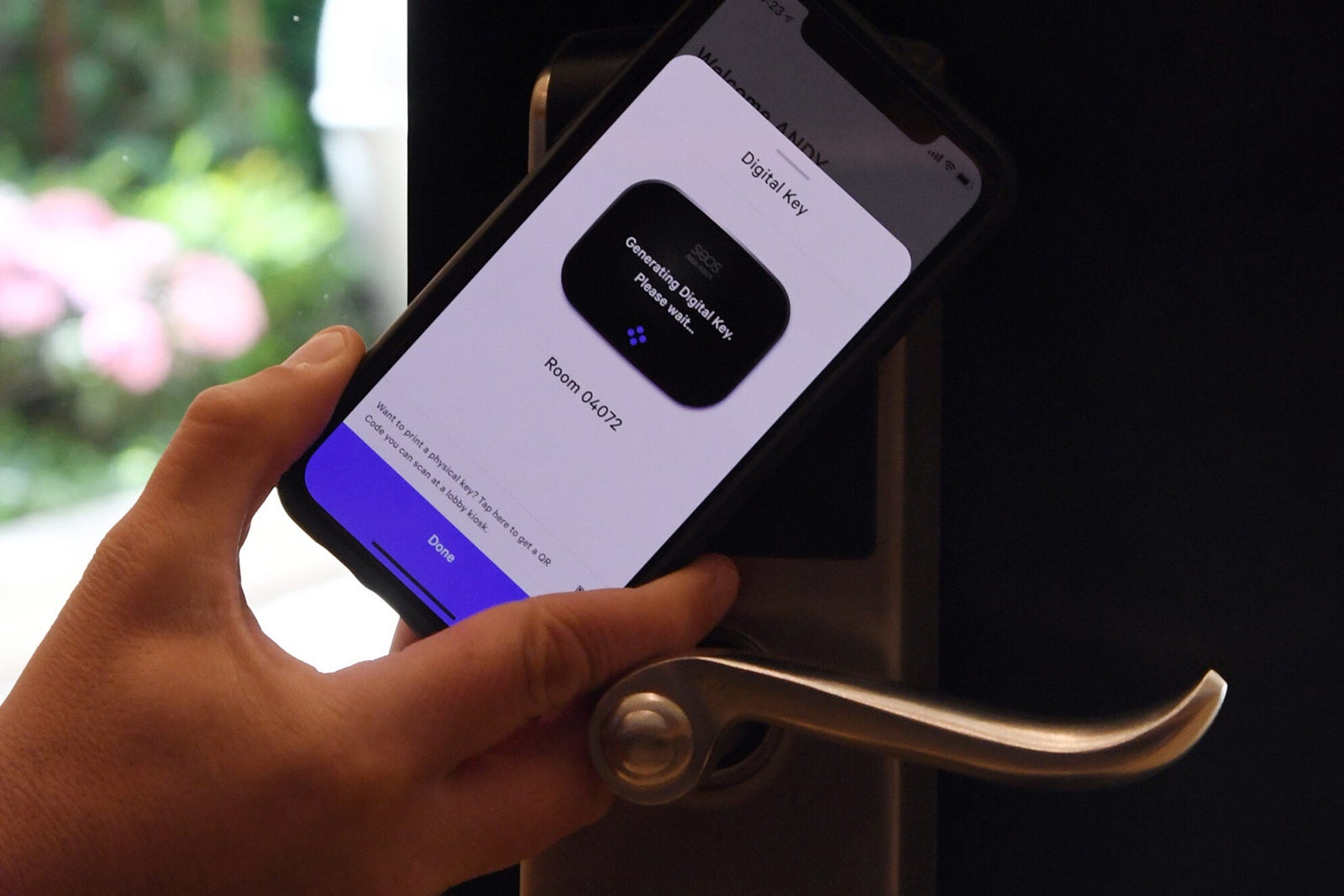

Many travel merchants are implementing touchless platforms throughout the guest service experience. For example, Hilton has long offered digital room keys and is further enhancing the mobile app to enable touchless temperature controls, TV, lights, and more.

Major hotel chains have already begun removing literature from guest rooms in order to eliminate the spread of germs. In-room dining has been expanded at hotels that have been forced to shutter restaurants, with paper menus replaced by digital menus accessible via QR codes.

Bottom line

Pay ahead, mobile payment services and contactless payments are here to stay. Even as the CDC relaxes mask requirements and eases social distancing requirements for fully vaccinated individuals, you'll want to get used to these methods of payment that have been prevalent in other parts of the world already.

Additional reporting by Stella Shon, Ariana Arghandewal and Madison Blancaflor.