When does it make sense to buy points and miles?

Update: Some offers mentioned below are no longer available. View the current offers here.

Did you know that many loyalty programs will sell you their program's points or miles currency with no strings attached?

You can jump online, log in to your account and buy points or miles with a credit card and a few clicks. These programs usually have generous purchase limits, meaning you could top up your balance with a six-figure amount in minutes.

What's the catch? Well, the cost. The purchase price per point or mile is usually higher than TPG's valuations.

The good news is that programs regularly run promotions to buy points and miles. During these promotions, you can often snag points and miles for about half their typical cost and sometimes for even less than our valuation, meaning you can then redeem them for more value than it costs you to buy them.

However, you may not want to buy points and miles even when they're on sale. So, in this guide, I'll discuss when it makes sense to buy points and miles.

When should you buy points and miles?

It makes sense to buy points and miles when you can obtain more value for redeeming them than it costs you to purchase them.

Say you were looking at a flight costing $500 in cash or 20,000 miles plus $50 in fees and taxes. If you could buy those 20,000 miles for 1 cent each during a bonus promotion, then the cost of that airfare with your purchased miles would only be $250 (20,000 times $0.01 plus the $50 in taxes and fees) rather than the $500 for a standard cash fare.

That would be a great deal.

For this reason, I look out for sale offers where you either receive bonus miles when purchasing minimum amounts or the price is discounted. A good rule of thumb is that when the price per mile drops below TPG's valuation of that mileage currency, there is a good chance you can redeem them for more value than it costs you to purchase them.

For example, Air Canada's Aeroplan program is my favorite Star Alliance loyalty program, if not my favorite airline loyalty program worldwide. Aeroplan points are easy to earn and redeem with attractive partner redemption rates and a huge list of 50 airline partners, including Lufthansa, All Nippon Airways, Emirates, Singapore Airlines and Cathay Pacific.

TPG values Aeroplan points at 1.5 cents each, per our July 2024 valuations, and I know I can easily redeem them for at least that value, whether for business-class flights to Europe on Air Canada or to Africa on Ethiopian Airlines.

You can purchase Aeroplan points for 3.5 Canadian cents per point, around 2.6 U.S. cents. At this price, it is almost a cent higher than our valuation, so as much as I love my Aeroplan points, I do not purchase them.

However, the program occasionally offers bonus deals when purchasing points, usually between 80% and 100%. A 100% bonus offer means that if I were to buy 50,000 points for 2.6 cents each, I would receive an extra 50,000 points at no cost. This means I'm purchasing the points for 1.3 cents each, which is an attractive offer.

Aeroplan recently offered a 125% bonus on purchasing Aeroplan points, which brought the cost down to around 1.14 cents each (this offer has now ended, but check out the current offers page for buying points and miles, which we regularly update).

The program typically only offers this bonus level around once a year, so I jumped at the opportunity and purchased a large amount of Aeroplan points, but only because I knew that I would eventually redeem them. If you don't have a specific redemption in mind or are not a frequent user of one program, TPG typically doesn't recommend purchasing points or miles as devaluations regularly occur, which makes hoarding one currency a bad long-term investment.

Since I book a lot of flights through Aeroplan, I know I can easily redeem my purchased points for at least TPG's valuation, if not significantly more.

For example, I know I can fly from Western Europe to the eastern United States for just 60,000 Aeroplan points in business class on partner airlines like Lufthansa and Swiss. By purchasing points for 1.14 cents each, I can fly across the Atlantic in business class for less than $700 worth of points, plus minimal taxes and fees. That is a terrific deal.

But there are caveats.

The calculation above assumes you can redeem the miles for the airfare you want at the first quoted redemption rate. The first problem with this assumption is that redemption availability constantly changes. The seat that may have been available today when you considered buying the points and miles might not be available tomorrow.

For those programs that use dynamic pricing, the prices for the same flight can change constantly.

Related: How much will your vacation really cost? The scourge of dynamic pricing is spreading like wildfire

The second issue is that the number of points or miles you need could increase. Most programs increase requirements occasionally — known as a devaluation — and your loyalty currency becomes less valuable. Some programs will warn members before changes happen, but programs have devalued overnight without notice.

If you're confident you can redeem the points or miles for the purpose you bought them for at the price you are happy with, it can make sense to buy them, but you shouldn't stockpile this currency for a rainy day.

It can also make sense when you are a few thousand points or miles short of a big redemption, such as first-class flights for your honeymoon. Even if the points or miles aren't on sale, topping off your account to make a dreamworthy redemption could make sense.

Related: How to decide whether to use cash or miles for airline tickets

When shouldn't you buy points or miles?

If it's cost-ineffective, you shouldn't buy points or miles.

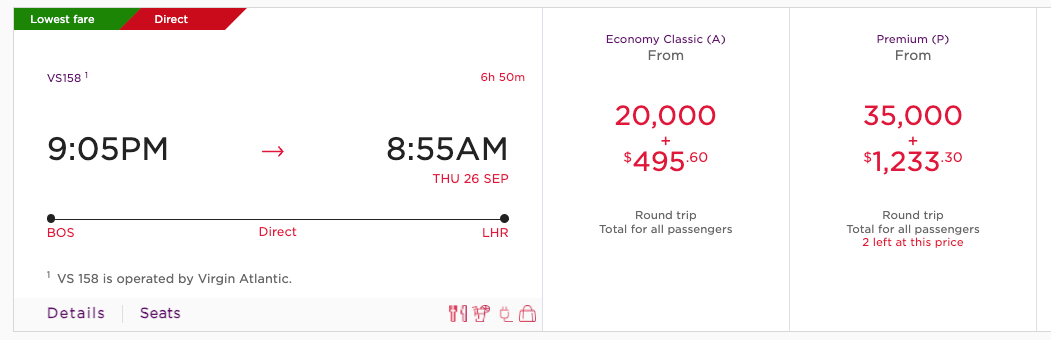

It would be best to remember that when you buy points or miles, you are subject to the cost of the points or miles and the taxes and fees associated with booking your award tickets. For example, Virgin Atlantic Flying Club only requires 20,000 points for a round-trip flight from New York to London during the standard (i.e., off-peak) season. But before you think you've effectively found a discounted one-way flight to London, you need to understand the fee structure associated with this type of ticket.

First, you must pay a transaction fee to buy the points. Then, when booking your ticket, Virgin imposes a hefty surcharge and taxes and fees. In this case, the taxes and fees alone may be more expensive than the cost of the points. You might do better by paying cash outright for a paid fare.

It rarely makes sense to purchase points or miles if you don't plan to redeem them immediately — known as purchasing them "speculatively." This is because you can't guarantee their value in the future when you decide to use them because of devaluations and other ways loyalty programs can change their programs.

Related: Why points and miles are a bad long-term investment

Which credit card should you use to buy points and miles?

Most of these promotions are processed through Points.com rather than directly by the hotel or airline, so you won't earn bonus rewards with most travel rewards cards. You'll want to use an everyday spending card that offers a solid return on nonbonus spending.

The main exception to this rule is American Airlines. This airline reportedly codes mileage purchases as airfare, so you may want to use a credit card that earns bonus miles on airfare for the highest return when buying AAdvantage miles.

If you're working toward a minimum spending requirement to earn a welcome bonus on a new card, using that card may be the best option.

Remember that you may incur foreign transaction fees on some cards when buying points or miles from a program abroad, so you may want to use one of the following cards:

- Capital One Venture Rewards Credit Card: 2 miles per dollar spent on all purchases and no foreign transaction fees

- Capital One Venture X Rewards Credit Card: 2 miles per dollar spent on all purchases and no foreign transaction fees

Bottom line

In the right circumstances, you can get amazing deals by buying points and miles. Over the past decade, I've bought over a million points and miles in different programs. That is because, at the time, I had immediate uses for them.

If you are considering buying points or miles, know that those rewards will unlikely ever be worth more than they are right now. After all, devaluations happen frequently. So, if you're buying speculatively, it's possible your newly purchased points and miles could drop in value before you use them.