The best travel insurance policies and providers

Editor's Note

Travel insurance can be polarizing, but this guide isn't about whether it's worth it. Instead, it's about comparing the top providers to help you find the best option for your next trip.

In this guide, I'll review policies from seven top travel insurance providers so you can better understand your options before choosing a specific policy and provider.

The best travel insurance providers

Here's an overview of the travel insurance providers I'll discuss in this guide:

- Allianz Travel Insurance: Best for frequent travelers who want an annual plan

- American Express Travel Insurance: Best for build-your-own-plan flexibility

- Berkshire Hathaway Travel Protection: Best for a straightforward claims process

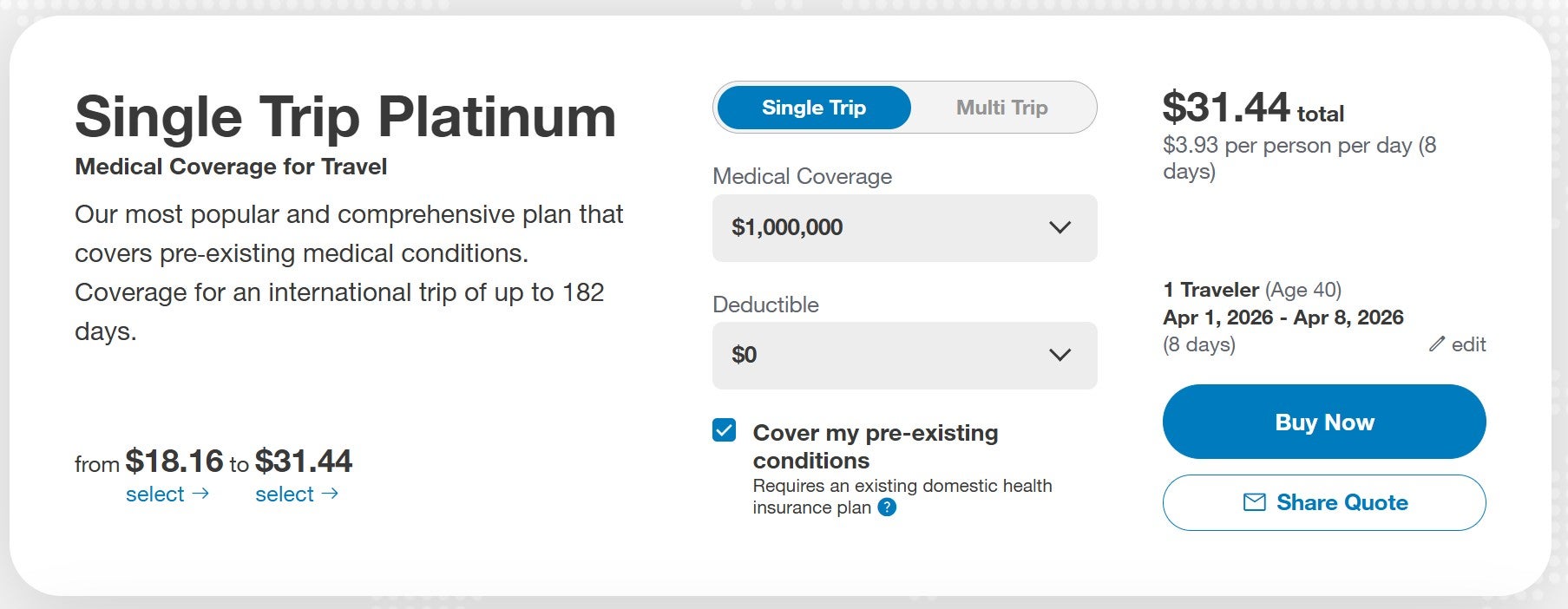

- Blue Cross Blue Shield Global Solutions: Best for international medical coverage

- Travel Guard: Best for customizable add-ons and optional bundles

- Travelex Insurance: Best for travelers who may need to cancel for business reasons

- World Nomads: Best for active travelers who enjoy adventure activities

I considered several details while putting together this list of the best travel insurance providers, including favorable ratings from travelers who have used these providers, the availability of policy and claims process details online, and the ability to purchase policies in most U.S. states.

Related: Should you get travel insurance if you have credit card protection?

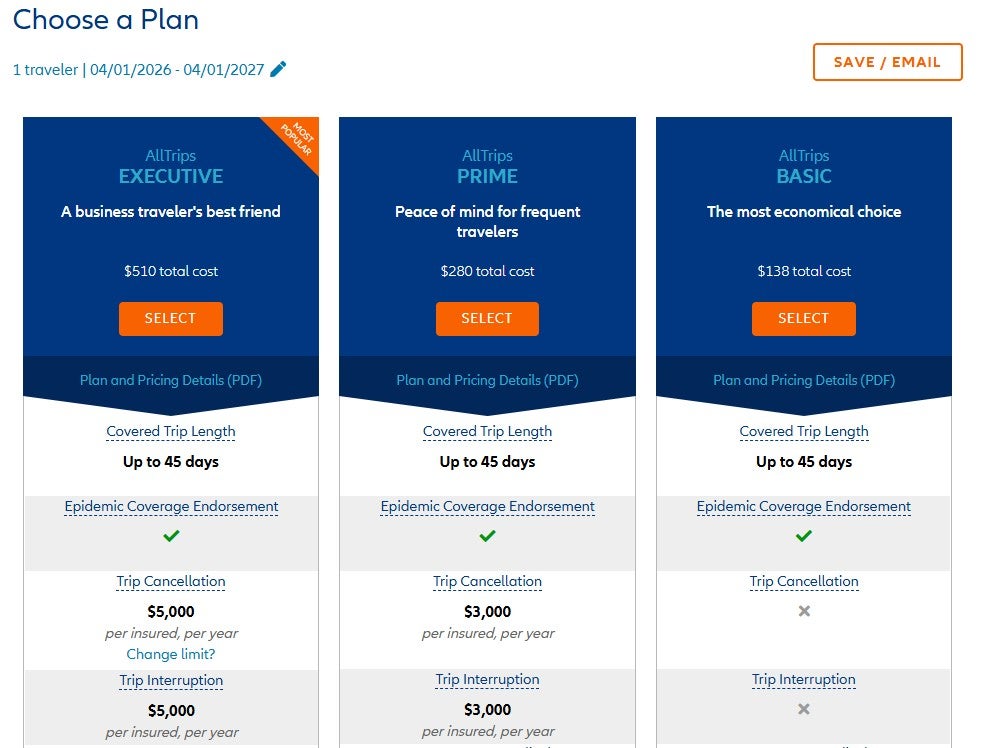

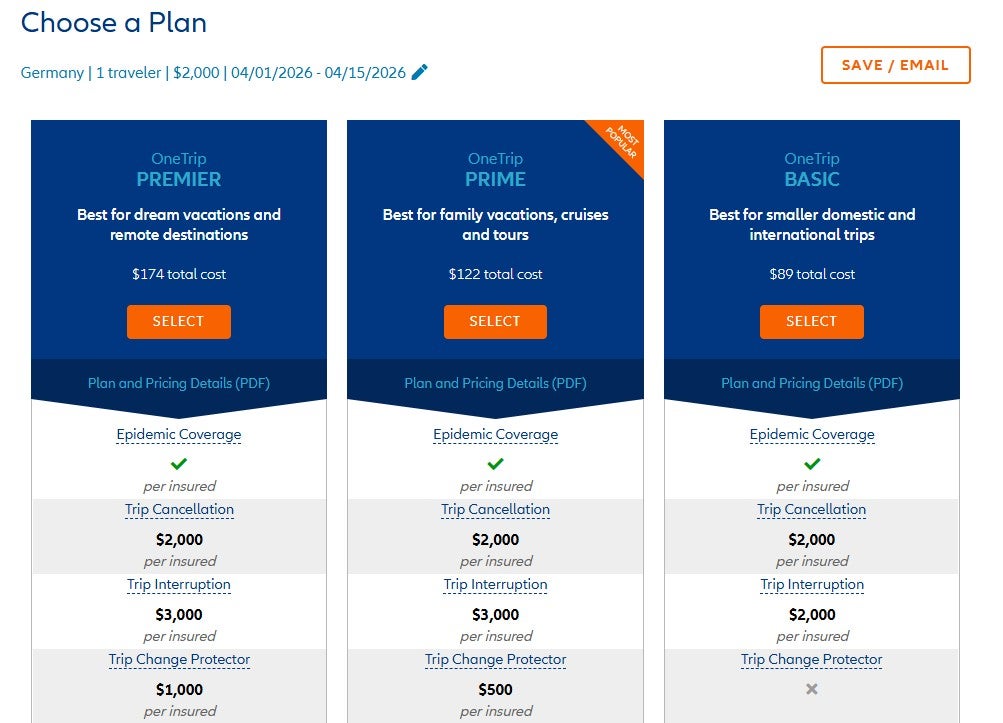

Allianz Travel Insurance

Many travelers highly regard Allianz Travel Insurance, including those who have had to file claims with the provider. Allianz offers single-trip plans, as well as annual plans that cover multiple trips.

Some Allianz plans leave out trip cancellation or interruption insurance — which can be ideal if you usually book award flights and hotels that you can cancel for free until shortly before your trip, or if you're already getting these protections through your travel rewards cards.

Why consider Allianz Travel Insurance?

- Some single-trip plans offer an upgrade that lets you cancel your trip for any reason and receive 80% of your nonrefundable trip costs back.

- The AllTrips Premier plan provides annual coverage for all your household members, even when they are traveling separately.

- The OneTrip Prime plan covers children 17 and under at no additional cost when traveling with a parent or grandparent.

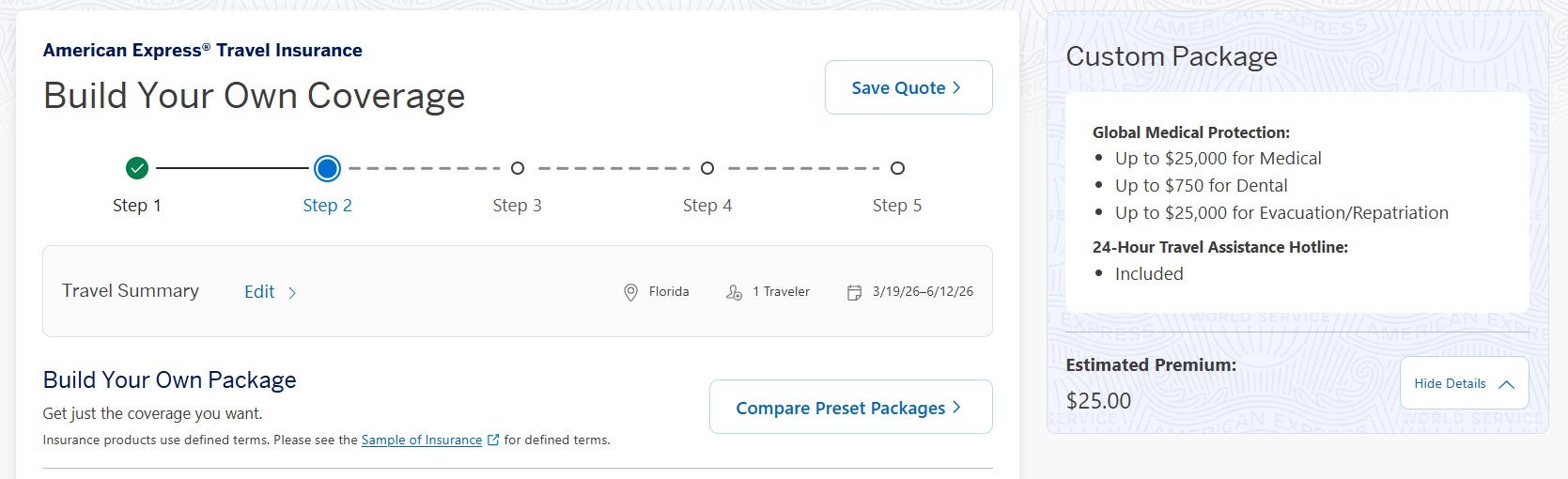

American Express Travel Insurance

American Express Travel Insurance offers four package plans and a build-your-own-coverage option. You don't need to be an American Express cardholder to purchase this insurance.

Amex's build-your-own-coverage plan is unique because you can purchase only the coverage you need. For most types of protection, you can even select the coverage amount that works best for you.

Why consider American Express Travel Insurance?

- Amex's build-your-own-coverage option lets you pay only for the coverage you need.

- The cost of coverage is determined by the cost of the trip, not the duration. However, regardless of the duration, the emergency medical and dental benefit only covers your first 60 days of travel.

- American Express Travel Insurance can protect travel expenses you purchase with Amex Membership Rewards points in the Pay with Points program (as well as travel expenses bought with cash, debit or credit). However, travel expenses bought with other points and miles aren't covered.

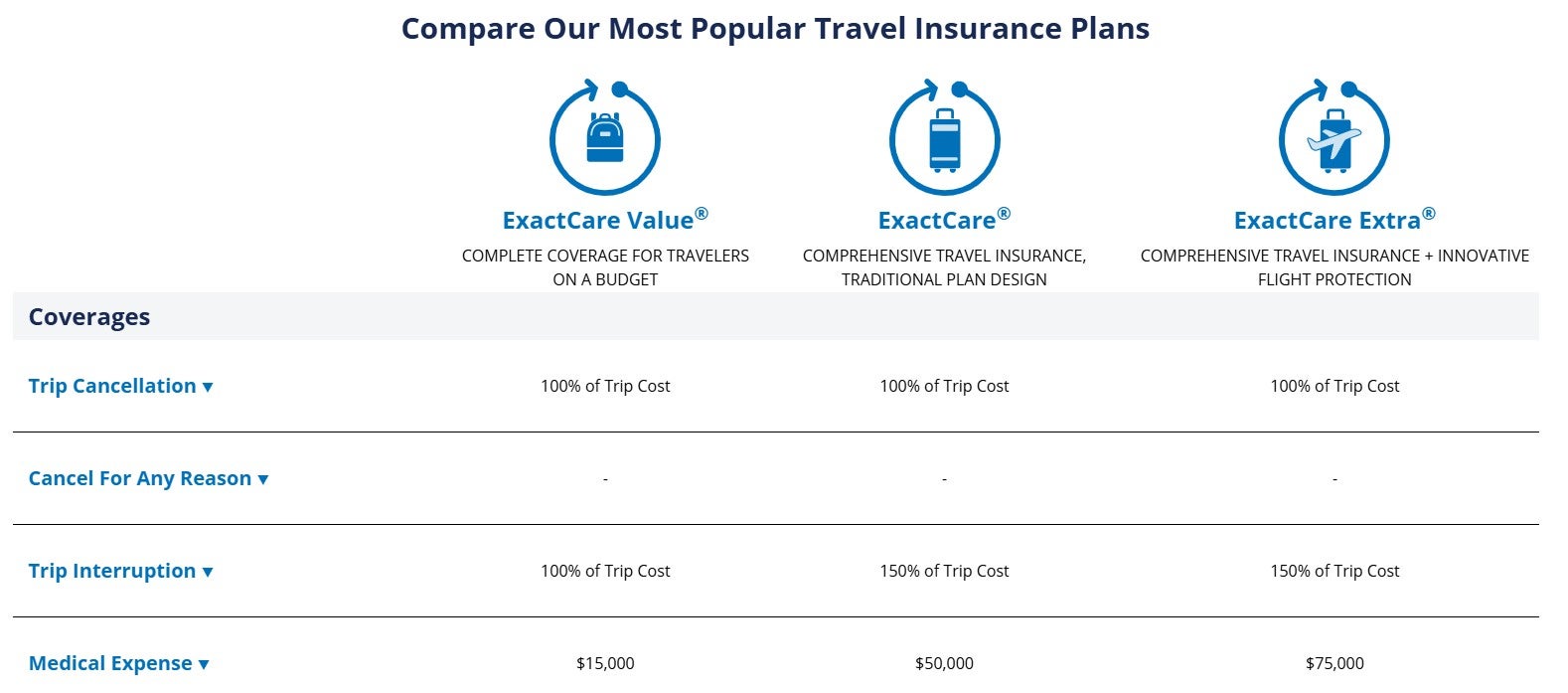

Berkshire Hathaway Travel Protection

Berkshire Hathaway Travel Protection is highly recommended among travelers for its relatively straightforward claims process. The provider offers three types of single-trip travel insurance and four specialty plans.

The specialty plans include a post-departure travel insurance plan (ExactCare Lite), a cruise travel insurance plan (WaveCare) and an adventure travel plan (AdrenalineCare) that includes adventurous activities like sky diving, rock climbing or scuba diving.

Why consider Berkshire Hathaway Travel Protection?

- The ExactCare Extra plan includes payment if your delay exceeds two hours on the tarmac or if your flight is delayed by more than two hours from its scheduled gate departure.

- ExactCare and ExactCare Extra plans include a cancel-for-work-reasons benefit.

- WaveCare provides a cruise disruption benefit if your cruise does not stop at a scheduled port for a covered reason.

Blue Cross Blue Shield Global Solutions

Blue Cross Blue Shield Global Solutions differs from most other providers in this piece because it only provides medical coverage. There are many different policies, but some require primary health insurance in the U.S. (although it doesn't need to be provided by Blue Cross Blue Shield), and most don't offer medical coverage within the U.S.

Gold and Platinum policies can likely meet the needs of most travelers, with options for single- or multi-trip coverage outside the U.S. However, special plans also provide options for other types of travel, including studying and working abroad.

Why consider Blue Cross Blue Shield Global Solutions?

- Blue Cross Blue Shield Global Solutions can be an excellent option if you're mainly concerned about the medical side of travel insurance.

- Blue Cross Blue Shield Global Solutions provides single-trip, multi-trip and long-term medical travel insurance policies for many different types of travel.

- Some Blue Cross Blue Shield Global Solutions policies, such as most Platinum policies, cover sudden recurrences of preexisting conditions for medical services and evacuation.

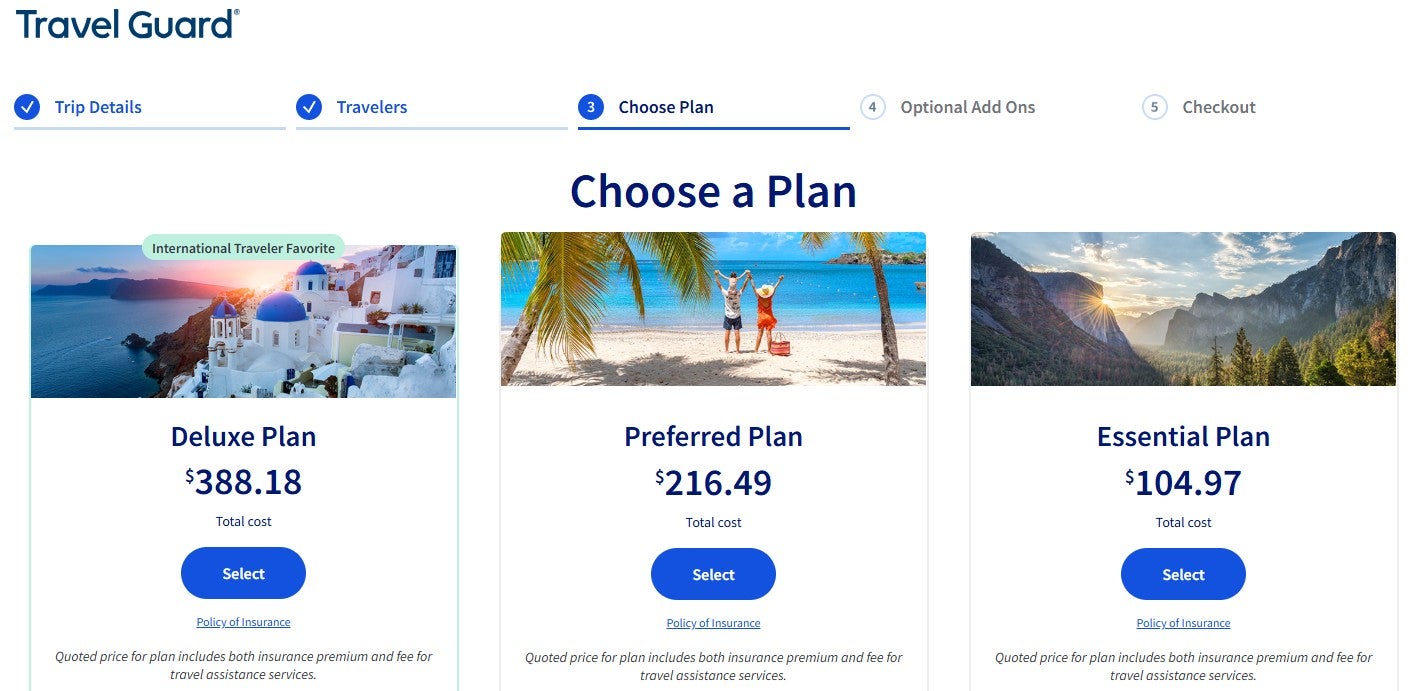

Travel Guard

Travel Guard offers three standard plans online, which you can compare side by side. But what sets Travel Guard apart from many other providers in this article is the ability to add a wide variety of optional coverage and bundles to these plans.

You can also buy an annual travel insurance plan from Travel Guard that covers multiple trips.

Why consider Travel Guard?

- Some single-trip plans offer an upgrade that lets you cancel your trip for any reason. However, reimbursement under this coverage will not exceed 50% of your covered trip cost.

- You can add a "name your family" bundle to some single-trip plans. This bundle lets you add one person not normally included under your plan as a family member for coverage purposes that would normally only apply to those related by blood or marriage.

- You can add other optional bundles to some single-trip plans, including adventure sports, baggage, travel inconvenience, quarantine, pets, security and wedding travel.

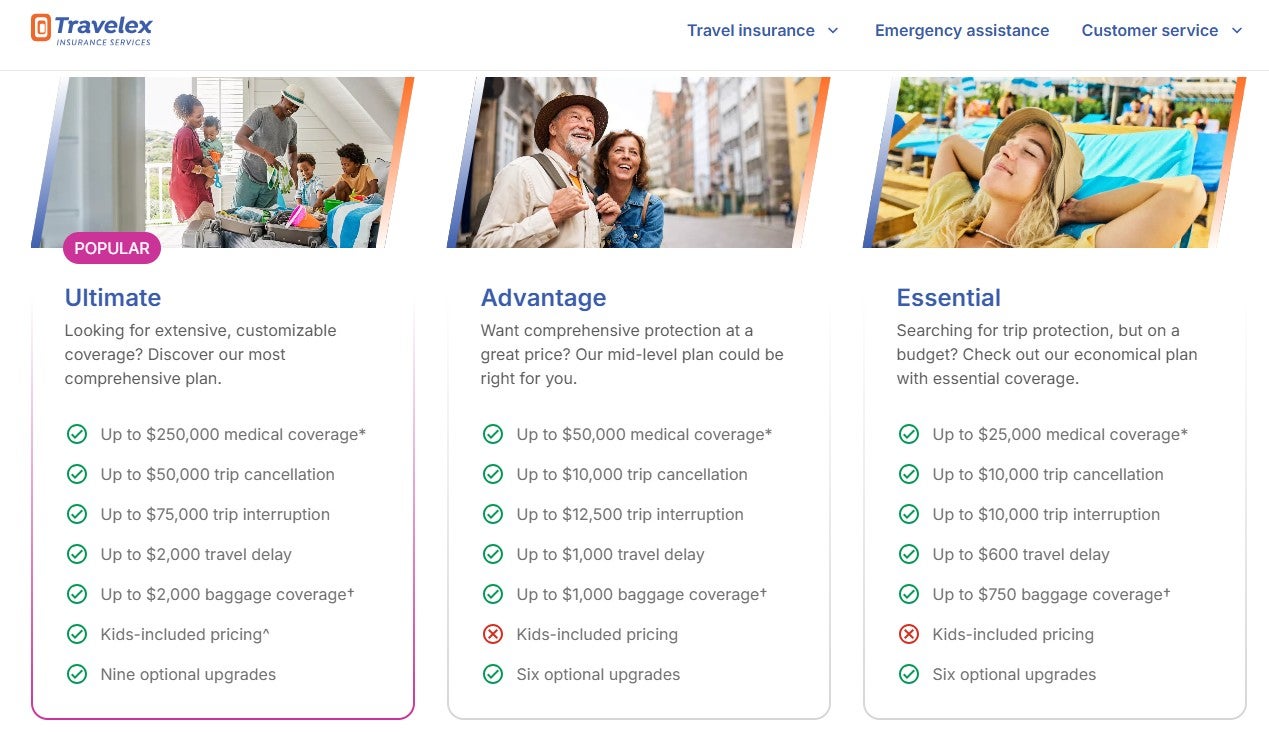

Travelex Insurance

Travelex Insurance offers three single-trip plans, each with some optional upgrades, that differ in their coverage maximums and inclusions.

Meanwhile, their Travel Med Go plan only offers on-trip benefits. This makes the Travel Med Go plan a good option for last-minute trips, or trips for which you've made plans you can cancel for little to no cost until shortly beforehand.

Why consider Travelex Insurance?

- Travelex's Ultimate policy can cover trips lasting up to 180 days and includes one traveling companion, 17 years or younger, for each insured adult.

- You can add rental property security deposit coverage to most plans, covering up to $2,000 of repairs if you accidentally damage your accommodations.

- You can add cancel-for-any-reason insurance or cancel-for-business-reasons insurance to the Ultimate plan. Cancel-for-any-reason coverage will not exceed 75% of your insured trip cost (up to $7,500), while cancel-for-business-reasons coverage will cover 100% of your insured trip cost (up to $10,000).

World Nomads

World Nomads is more expensive than many other providers discussed in this article. However, it remains popular with active travelers because it covers many adventure activities.

It offers three single-trip plans, each covering one trip of up to 180 days, and one annual plan covering multiple trips within a 12-month period, each of up to 45 days.

Why consider World Nomads?

- World Nomads' policies cover more adventure sports and activities than most providers, such as bungee jumping, jet skiing, and even riskier activities like cliff diving and free soloing.

- You don't need to estimate prepaid costs when purchasing World Nomads travel insurance.

- Every World Nomads plan also includes help from Blue Ribbon Bags if an airline loses your checked bag, a predeparture medical consultation from Runway Health and a portable personal health record provided by FootprintID.

Other options for buying travel insurance

This guide details the policies of seven providers, based on the information available at the time of publication. There are many options when it comes to travel insurance, though. To compare different policies quickly, you can use a travel insurance aggregator like InsureMyTrip or SquareMouth to search. Just note that these search engines won't show every policy or provider, and you should still research the provided policies to ensure the coverage fits your trip needs.

You can also purchase a plan through various membership associations, such as USAA, AAA and Costco. Typically, these organizations partner with a specific provider, so if you are a member of any of these associations, you may want to compare the policies offered through the organization with other policies to get the best coverage for your trip.

Related: Valuable travel perks that you can get with a credit card

Is travel insurance worth it?

Whether you should purchase travel insurance is a personal decision. Suppose you use a credit card that provides travel insurance for most of your expenses and have medical insurance that provides adequate coverage abroad. In that case, you may be covered enough on most trips to forgo purchasing travel insurance.

However, suppose your medical insurance won't cover you at your destination, and you can't comfortably cover a sizable medical evacuation bill or last-minute flight home. In that case, it may be worth purchasing travel insurance. Buying an annual multi-trip policy may be worth it if you travel frequently.

Related: 7 times your credit card's travel insurance might not cover you

What does travel insurance cover?

Travel insurance usually offers some of the following types of coverage:

- Baggage delay protection may reimburse you for essential items and clothing when a common carrier (such as an airline) fails to deliver your checked bag within a set time of your arrival at a destination. You may be reimbursed up to a particular amount per incident or day.

- Lost or damaged baggage protection may provide reimbursement for lost or damaged luggage and its contents. However, valuables and electronics usually have a relatively low maximum benefit.

- Trip delay reimbursement may provide reimbursement for necessary items, food, lodging and transportation when you're delayed for a substantial time while traveling on a common carrier, such as an airline. This insurance may be beneficial if weather issues (or other covered reasons for which the airline usually won't provide compensation) delay you.

- Trip cancellation and interruption protection may reimburse you if you need to cancel or interrupt your trip for a covered reason, such as a family death or jury duty.

- Medical evacuation insurance can arrange and pay for medical evacuation if necessary, with the assistance of the insurance provider and a medical professional. This coverage can be particularly valuable if traveling to a region with subpar medical facilities.

- Travel accident insurance may provide a payment to you or your beneficiary in the case of your death or dismemberment.

- Emergency medical insurance may provide payment or reimbursement to you if you must seek medical care while traveling. Some plans only cover emergency medical care, but some also cover other types of medical care. You may need to pay a deductible or copay.

- Rental car coverage may provide a collision damage waiver when renting a car. This waiver may reimburse for collision damage or theft up to a set amount. Some policies also cover loss-of-use charges assessed by the rental company and towing charges to the nearest qualified repair facility. You generally need to decline the rental company's collision damage waiver or similar provision to be covered.

However, keep in mind that most travel insurance benefits have exclusions. For example, most travel insurance policies specifically exclude coverage during acts of war.

Related: Can my credit card help if my vacation is affected by a military conflict or war?

How much is travel insurance?

Travel insurance costs depend on various factors, including the provider, the type of coverage, trip cost, destination, your age, where you live and how many travelers you want to insure. A standard travel insurance plan will generally cost between 4% and 10% of your total trip cost. However, this can be lower for basic protections or higher if you add on options like cancel-for-any-reason protection.

The best way to determine how much travel insurance will cost is to price out your trip with a few providers discussed in the guide. You can also visit an insurance aggregator like InsureMyTrip or SquareMouth to quickly compare options across multiple providers.

Related: My 4 top travel credit cards — and how they elevate my trips

When and how to get travel insurance

For the most robust selection of available travel insurance benefits — including time-sensitive add-ons like cancel-for-any-reason protection and waivers of preexisting conditions for eligible travelers — you should ideally purchase travel insurance on the same day you make your first payment toward your trip.

Some providers may still offer a preexisting conditions waiver if you buy travel insurance within 14 to 21 days of your first trip expense or deposit. But if you don't need a preexisting conditions waiver and aren't interested in cancel-for-any-reason coverage, you can purchase travel insurance once your departure date nears.

However, you'll usually need to purchase your plan before departure, and you must always buy travel insurance before you know you need it. Once you recognize the need, it's too late to protect your trip.

Once you've shopped around and decided on the best travel insurance plan for your trip, you can almost always complete your purchase online. You'll usually be able to download your insurance card and the complete policy shortly after the transaction.

Related: Best credit cards for everyday spending

Bottom line

Not all travel insurance policies and providers are equal. Before buying a plan, make sure you read and understand the policy documents. This will help you choose a plan appropriate for you and your trip.

For example, if you plan to go skiing or rock climbing, make sure the policy you buy doesn't exclude these activities. Likewise, if you're making two back-to-back trips and will be returning home for a short time in between, be sure the plan doesn't terminate coverage at the end of your first trip.

Finally, if you're looking to cover a sudden recurrence of a preexisting condition, select a policy with a preexisting condition waiver and fulfill the requirements for the waiver. After all, buying insurance won't help if your policy doesn't cover your losses.