Debunking credit card myths: Does canceling a card I don’t use help my credit score?

Editor's Note

It's no surprise that travel rewards credit cards get quite a bit of coverage here at TPG.

Taking advantage of top welcome bonuses and strategically using your cards for everyday purchases can unlock fantastic redemptions, such as premium cabin flights and luxurious hotel rooms. However, there are a number of misconceptions about credit cards.

Let's debunk one notable myth to hopefully help you avoid a credit score drop.

Related: How do credit scores work?

Myth: Closing a card I don't use will help my credit score

There are many reasons why you might have a credit card that you simply don't use anymore.

Maybe it was the very first one you opened as an adult, but you have since been replaced with a more valuable card. Maybe your priorities have shifted, and a certain card no longer fits into your strategy. Or maybe you have relocated to a new area of the country and found that your go-to card has less utility.

In these cases, you may think that you should cancel an unused card just sitting in your wallet (or sock drawer) to help your credit score. However, in reality, you may find the exact opposite to be true. Canceling a card can actually drop your credit score.

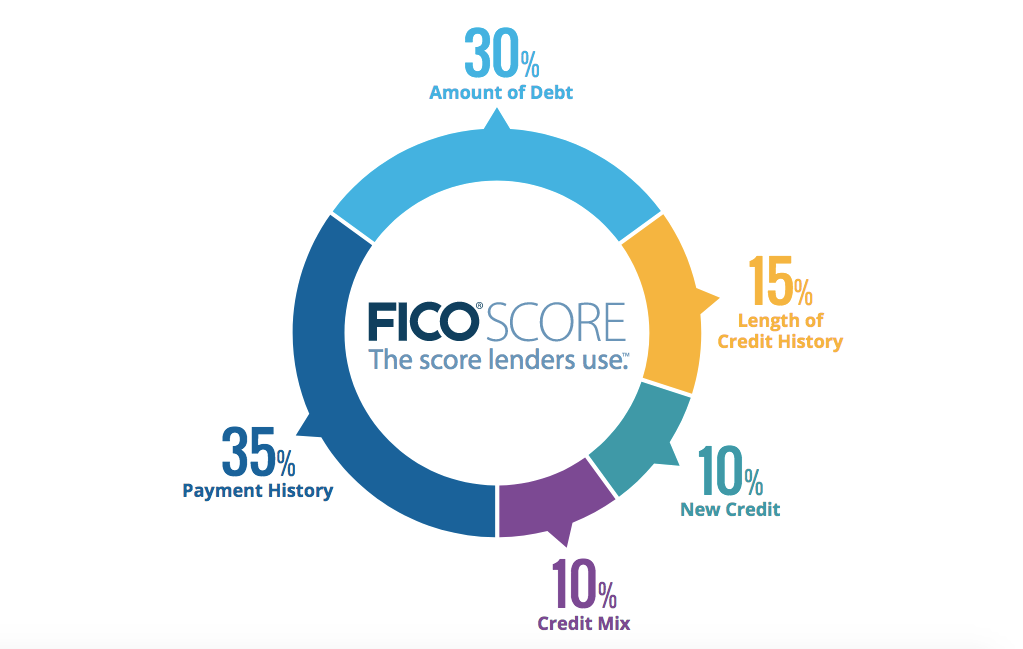

For this myth, it's essential to understand the different factors that contribute to your FICO score, the metric most frequently used to determine your creditworthiness for any new line of credit:

- Payment history

- Amounts owed

- Length of credit history

- New credit

- Types of credit used

However, not all factors are created equal. In the graphic below, these five factors are weighted based on how important they are to your score.

When it comes to closing a card you no longer use, there's one primary factor that can impact your score in a negative way: amounts owed.

Related: How to check your credit score

Amounts owed

The second most important factor in your FICO score is your amounts owed — commonly referred to as your credit utilization rate. This looks at how much of your credit you are actually using, and it's typically expressed as a percentage. Here's the calculation: Total balance on your account(s) divided by the total limit of account(s) equals utilization.

Keeping this number low shows issuers that you can effectively manage your credit lines and aren't at risk of overextending yourself.

An example

Let's say that you typically spend about $2,000 per month on your primary credit card with a $10,000 limit, and you currently have another unused card, also with a $10,000 limit. You thus have a utilization rate of 10% ($2,000 divided by $20,000).

However, if you then cancel that unused card, the monthly spending is now spread across a much lower credit line. By canceling the card, your utilization jumps to 20%. That number isn't too concerning, but you shouldn't take anything that impacts your score lightly.

Of course, that's not to say that you should never cancel a credit card. If you're no longer using a card that carries an annual fee, it may not make sense to keep that card open unless the benefits you're getting outweigh the fee. Just be sure to call the issuer and inquire about a retention bonus. The agent may even be willing to waive the annual fee.

Related: How canceling a credit card impacts your FICO score

Length of credit history

While the amounts owed are the primary factor affected by canceling a card you no longer use, it can also impact your credit history, which makes up 15% of your credit score.

If the unused card is your longest-tenured account, canceling it can negatively affect the average age of your accounts. However, this doesn't happen right away, as closed accounts (in good standing) will typically stay on your credit report for up to 10 years.

Nevertheless, canceling a card with no annual fee — especially one you've had for years — can ultimately impact your score.

This is a key reason why I always recommend opening and keeping at least one card with no annual fee. Just be sure to make a least a few purchases a year on the card to prevent the issuer from canceling it due to inactivity. This can also help prevent your points and miles from expiring.

Bottom line

There are many myths about credit cards, and one common misconception is that you should cancel a card that you don't use anymore to boost your credit score.

In reality, this can have a significant negative impact on your credit score, as it will lower your overall credit limit and thus increase your utilization rate. Over time, this could (potentially) decrease your average age of accounts as well. While there may be legitimate reasons to cancel a card, don't do it without first considering how it will affect your credit score.

TPG featured card

at American Express's secure site

Terms & restrictions apply. See rates & fees.

| 4X | Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 4X | Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 5X | New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App. |

| 3X | Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines. |

| 2X | Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com. |

| 1X | Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases. |

Pros

- Valuable dining and food-related credits

- Flexible rewards with airline and hotel transfer partners

- Multiple travel and purchase protections

- No foreign transaction fees

- Access to Amex Offers for additional savings (enrollment required)

Cons

- Not as useful for those living outside the U.S.

- Some may have trouble using Uber and other dining credits

- You may be eligible for as high as 100,000 Membership Rewards® Points after you spend $8,000 in eligible purchases on your new Card in your first 6 months of Card Membership. Welcome offers vary and you may not be eligible for an offer. Apply to know if you’re approved and find out your exact welcome offer amount – all with no credit score impact. If you’re approved and choose to accept the Card, your score may be impacted.

- Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year.

- Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year.

- New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App.

- Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines.

- Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com.

- Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases.

- Pay It® lets you tap in the American Express® App to quickly pay for small purchase amounts throughout the month and still earn rewards the way you usually do. Plan It® gives you the option to split up big purchases into equal monthly payments with a fixed fee. You’ll know upfront exactly how much you’ll pay.

- Updated! $120 Dining Credit: Earn up to a total of $10 in statement credits monthly when you pay with the Gold Card at Grubhub (including Seamless), Buffalo Wild Wings, Five Guys, The Cheesecake Factory, and Wonder. This can be an annual savings of up to $120. Enrollment required.

- $100 Resy Credit: Get up to $100 in statement credits each calendar year at over 10,000 qualifying U.S. Resy restaurants after you pay for eligible purchases with the American Express® Gold Card. That’s up to $50 in statement credits semi-annually. Enrollment required.

- $84 Dunkin' Credit: Earn up to $7 in monthly statement credits after you pay with the American Express® Gold Card at U.S. Dunkin’ locations. Enrollment required.

- $120 Uber Cash on Gold: Enjoy up to $120 in Uber Cash annually with your Gold Card. Just add your Card to your Uber account and you'll get $10 in Uber Cash each month to use on orders and rides in the U.S. when you select an Amex Card for your transaction.

- New! As an American Express® Gold Card Member, you can enjoy complimentary Hertz Five Star® Status. Enjoy benefits like skipping the counter at select locations, adding an additional driver at no additional cost*, and vehicle upgrades**. Benefit enrollment and Hertz Gold+ registration are required. *Additional drivers must meet standard rental qualifications and must be a spouse or domestic partner to qualify as complimentary. Other additional drivers subject to fees. **Benefits are subject to availability and vary by location. Additional Hertz program Terms and Conditions including age restrictions apply.

- Take advantage of a $100 credit towards eligible charges* at over 1,300 upscale hotels worldwide when you book The Hotel Collection through AmexTravel.com or the Amex Travel App **. *Eligible charges vary by property. **The Hotel Collection requires a two-night minimum stay.

- Book your travel through the Amex Travel App with added peace of mind – backed by American Express® service and support. Only for American Express® Card Members.

- Whenever you need us, we're here. Our Member Services team will ensure you are taken care of. From lost Card replacement to statement questions, we are available to help 24/7.

- No Foreign Transaction Fees.

- Annual Fee is $325.

- Terms Apply.