Debunking Credit Card Myths: Should You Accept a Credit Line Increase?

Update: Some offers mentioned below are no longer available. View the current offers here.

We frequently discuss travel rewards credit cards here at TPG. These cards allow you to earn top sign-up bonuses and provide numerous bonus categories for everyday spending, unlocking terrific redemptions like premium-class flights and luxurious hotel rooms. However, there are a number of misconceptions out there when it comes to credit cards, so today I'll continue our new series that debunks these myths and allows you to begin planning for your next vacation.

Previous entries includes having too many cards, closing a card you don't use, how permanent of an impact an application has on your score, not paying your balance in full, paying an annual fee, keeping your points when canceling a card, whether annual fees count toward a sign-up bonus, what to do if your application isn't immediately approved and whether cards are a surefire way to get into debt. Today I'll build on the most recent post and look at a myth related to your credit limit.

Myth #10: You should never accept a credit line increase.

One of the most important aspects of using a credit card is your credit limit. A card issuer wants to give you a high enough line of credit to encourage you to use your card but not so high that you'll default on the account. However, the initial limit you get when you open a new card isn't set in stone. As you prove your creditworthiness, an issuer may want to increase the amount of credit you have available.

This actually just happened to me on my Club Carlson Premier Rewards Visa Signature Card. I received a mailer offering me an extra $3,000 of credit on the card. I immediately followed the instructions provided and received an e-mail confirmation a few weeks later:

For some readers out there, this may seem like a recipe for disaster. Opening up additional credit can be a slippery slope if you struggle to manage your credit card accounts. However, as long as you don't use this increased credit line as "free" money, this can actually have a positive impact on your credit profile.

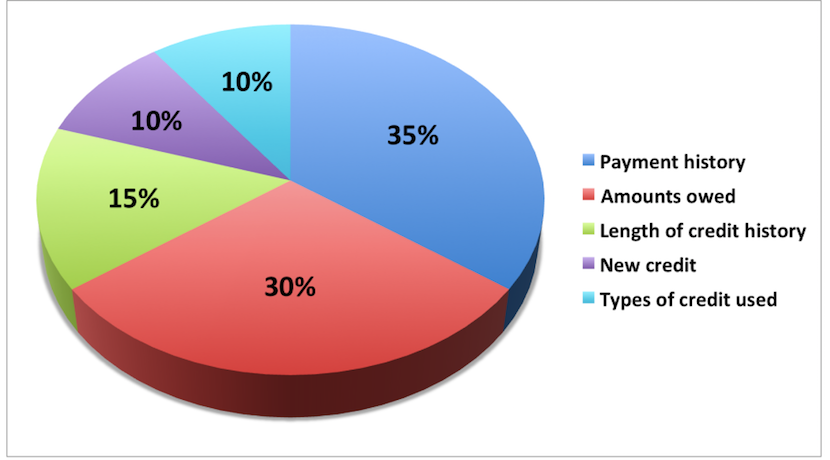

Let's quickly review the key factors that make up your FICO score, the one most frequently used to determine your creditworthiness:

- Payment history

- Amounts owed

- Length of credit history

- New credit

- Types of credit used

As we've discussed before, these five factors aren't created equal. Instead, they are weighted based on how important they are to your score:

When it comes to accepting a credit line increase, it's the second-most important factor (amounts owed) that comes into play. This is commonly referred to as your credit utilization rate, and it basically identifies how much of your available credit you are using. It is typically expressed as a percentage and calculated as follows:

Total balance on your account(s) / Total limit of accounts = Utilization

When this number is low, credit issuers see that you can effectively manage your credit and aren't at a significant risk for default.

Here's how a credit line increase can help this factor: Let's say that you have a single card with a $10,000 limit, and at any given time, you typically have a balance of roughly $1,500 (though you of course pay it off in full each month, my top commandment for travel rewards credit cards). Your utilization is thus 15%. This isn't particularly high but still may prevent you from adding a new card to your wallet, especially a premium one like the Chase Sapphire Reserve.

Now let's say that you're offered an increase of $5,000 and don't charge any more on the card each month. With that single change, your utilization drops to just 10%, making your credit profile more attractive to issuers. Of course, there are many other ways to improve your credit score, but as long as you don't take a credit line increase as an invitation to rack up debt, you shouldn't be afraid to accept one.

Bottom Line

Opening and utilizing a travel rewards credit card does carry some risk, and you may think that accepting a credit line increase is an easy way to enhance that risk. However, this can actually help boost your credit score, as long as you manage the higher credit limit carefully. If you're lucky enough to get targeted for one of these offers, don't just discard it! Hopefully this post has given you some insight into the benefits involved.

What are your thoughts on credit line increases?

TPG featured card

at American Express's secure site

Terms & restrictions apply. See rates & fees.

| 4X | Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 4X | Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 5X | New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App. |

| 3X | Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines. |

| 2X | Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com. |

| 1X | Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases. |

Pros

- Valuable dining and food-related credits

- Flexible rewards with airline and hotel transfer partners

- Multiple travel and purchase protections

- No foreign transaction fees

- Access to Amex Offers for additional savings (enrollment required)

Cons

- Not as useful for those living outside the U.S.

- Some may have trouble using Uber and other dining credits

- You may be eligible for as high as 100,000 Membership Rewards® Points after you spend $8,000 in eligible purchases on your new Card in your first 6 months of Card Membership. Welcome offers vary and you may not be eligible for an offer. Apply to know if you’re approved and find out your exact welcome offer amount – all with no credit score impact. If you’re approved and choose to accept the Card, your score may be impacted.

- Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year.

- Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year.

- New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App.

- Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines.

- Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com.

- Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases.

- Pay It® lets you tap in the American Express® App to quickly pay for small purchase amounts throughout the month and still earn rewards the way you usually do. Plan It® gives you the option to split up big purchases into equal monthly payments with a fixed fee. You’ll know upfront exactly how much you’ll pay.

- Updated! $120 Dining Credit: Earn up to a total of $10 in statement credits monthly when you pay with the Gold Card at Grubhub (including Seamless), Buffalo Wild Wings, Five Guys, The Cheesecake Factory, and Wonder. This can be an annual savings of up to $120. Enrollment required.

- $100 Resy Credit: Get up to $100 in statement credits each calendar year at over 10,000 qualifying U.S. Resy restaurants after you pay for eligible purchases with the American Express® Gold Card. That’s up to $50 in statement credits semi-annually. Enrollment required.

- $84 Dunkin' Credit: Earn up to $7 in monthly statement credits after you pay with the American Express® Gold Card at U.S. Dunkin’ locations. Enrollment required.

- $120 Uber Cash on Gold: Enjoy up to $120 in Uber Cash annually with your Gold Card. Just add your Card to your Uber account and you'll get $10 in Uber Cash each month to use on orders and rides in the U.S. when you select an Amex Card for your transaction.

- New! As an American Express® Gold Card Member, you can enjoy complimentary Hertz Five Star® Status. Enjoy benefits like skipping the counter at select locations, adding an additional driver at no additional cost*, and vehicle upgrades**. Benefit enrollment and Hertz Gold+ registration are required. *Additional drivers must meet standard rental qualifications and must be a spouse or domestic partner to qualify as complimentary. Other additional drivers subject to fees. **Benefits are subject to availability and vary by location. Additional Hertz program Terms and Conditions including age restrictions apply.

- Take advantage of a $100 credit towards eligible charges* at over 1,300 upscale hotels worldwide when you book The Hotel Collection through AmexTravel.com or the Amex Travel App **. *Eligible charges vary by property. **The Hotel Collection requires a two-night minimum stay.

- Book your travel through the Amex Travel App with added peace of mind – backed by American Express® service and support. Only for American Express® Card Members.

- Whenever you need us, we're here. Our Member Services team will ensure you are taken care of. From lost Card replacement to statement questions, we are available to help 24/7.

- No Foreign Transaction Fees.

- Annual Fee is $325.

- Terms Apply.