Debunking credit card myths: Does having many credit cards hurt your credit score?

Editor's note: This post has been updated with new information.

We talk about travel credit cards quite a bit here at TPG. Applying for and using these cards strategically can unlock incredible travel experiences such as premium class flights or luxurious hotel rooms. However, there are a number of misconceptions out there when it comes to credit cards, and these can stand in your way of not only fantastic rewards but also an excellent credit score.

Today, we're debunking an important myth that involves the number of credit cards you have.

Want more credit card news and advice? Sign up for TPG's daily newsletter

Myth: Having many credit cards will hurt your credit score

At the time of publication, I have 22 open (and active) credit cards. This number strikes many of my friends and family members as off-the-wall, and the most common comment I get is, "Aren't you worried about what all of those cards will do to your credit score?"

Related: Yes, I have 22 credit cards; here's why

In reality, I'm not worried about what they do to my score. Instead, I am enjoying the boost they have on my score.

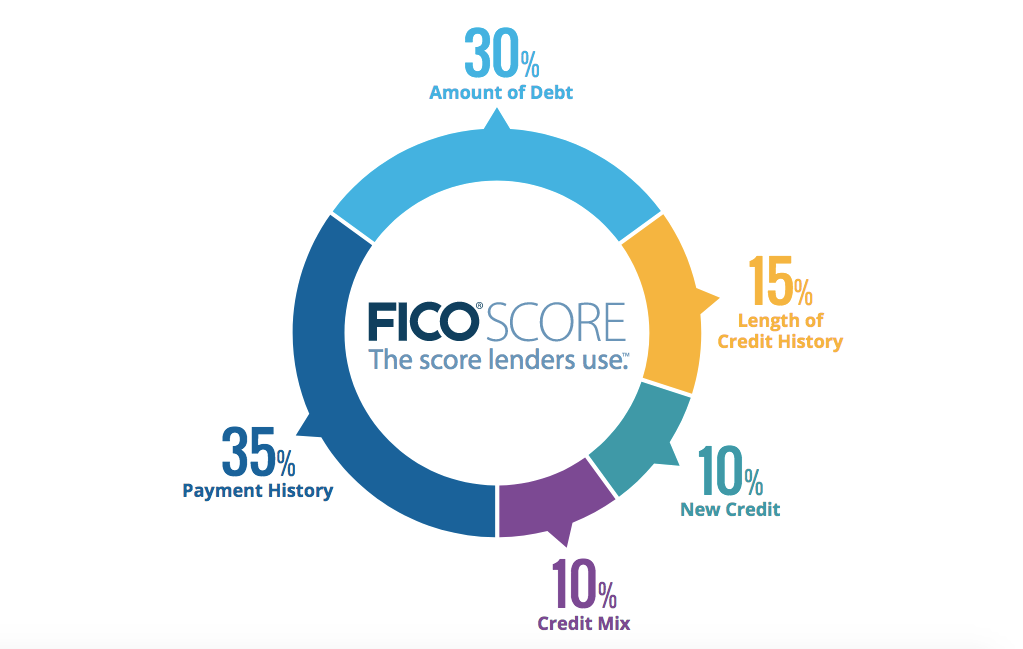

In order to debunk myths surrounding credit cards, it's essential to understand the different factors that contribute to your FICO score, the one most frequently used to determine your creditworthiness for any new line of credit:

- Payment history

- Amounts owed

- Length of credit history

- New credit

- Types of credit used

However, not all factors are treated equally, and these five are weighted based on how important they are to your score:

When it comes to opening a large number of credit cards, it's the two most important factors that come into play: payment history and amounts owed.

Related: How credit scores work

Payment history

The single biggest factor in your FICO score is your payment history, which covers any type of credit or installment account linked to your name. While one or two late payments won't completely ruin your score, it can have a negative impact.

So how does having multiple credit card accounts help this factor? It all comes down to painting a positive picture of your overall credit — and MyFico.com even points out that having multiple accounts with no late payments is a positive.

For example, let's say you have a single credit card and were late on two or three payments several years ago. Even though you've made up ground by paying on time ever since, you're still 0 for 1 when it comes to accounts showing a late payment. If you add new cards to your wallet and aren't late on any payments, you now have accounts with unblemished records. This may not move your score from 500 to 700, but in the long run, it's an undoubtedly positive pattern.

Amounts owed

The second most important factor in your FICO score is the amounts owed, commonly referred to as your credit utilization rate. This looks at how much of your credit you are actually using and is typically expressed as a percentage. Here's the calculation:

Total balance on your account(s) ÷ Total limit of accounts = Utilization

Keeping this number low shows issuers that you can effectively manage your credit lines and aren't at risk of over-extending yourself.

Let's say that you typically have a $2,000 balance on a credit card (paid off in full each month, of course), and your single card has a $10,000 limit. You thus have a utilization rate of 20% ($2,000 ÷ $10,000).

However, if you apply for another card and get another $10,000 of credit, you are now spreading that $2,000 balance across double the available credit. Your utilization drops to 10%.

Let's extend this math out to even more cards with that same $10,000 credit limit and the same $2,000 in monthly spending:

- Three cards: $2,000 ÷ $30,000 = 6.67%

- Four cards: $2,000 ÷ $40,000 = 5%

- Five cards: $2,000 ÷ $50,000 = 4%

My cards have a huge amount of available credit on them (over $300,000), but my utilization rate regularly hovers around 2%. I don't spend more on the cards just because I have them. What I am spending is just spread out across a broader credit line, helping my utilization rate and thus improving my credit score.

All that being said, it's important to note that there are situations where having too many credit cards can impact your credit score. Spending beyond your means (and not paying your balance in full) is a quick way to wreck your score, and adding untrustworthy authorized users can also have a negative impact. Remember too that you should do everything possible to avoid missing payments.

Related: Ten commandments for travel rewards credit cards

Bottom line

There are many myths about credit cards out there, and a common one relates to the perceived negative impact that multiple accounts can have on your credit score. In reality, the opposite is true, as almost two-thirds (65%) of your FICO score is determined by factors that can actually be enhanced with additional accounts. As always, be sure that you aren't over-extending yourself, as this myth can easily come true given the right (or wrong) environment.

Additional reporting by Benét J. Wilson

TPG featured card

at American Express's secure site

Terms & restrictions apply. See rates & fees.

| 4X | Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 4X | Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 5X | New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App. |

| 3X | Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines. |

| 2X | Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com. |

| 1X | Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases. |

Pros

- Valuable dining and food-related credits

- Flexible rewards with airline and hotel transfer partners

- Multiple travel and purchase protections

- No foreign transaction fees

- Access to Amex Offers for additional savings (enrollment required)

Cons

- Not as useful for those living outside the U.S.

- Some may have trouble using Uber and other dining credits

- You may be eligible for as high as 100,000 Membership Rewards® Points after you spend $8,000 in eligible purchases on your new Card in your first 6 months of Card Membership. Welcome offers vary and you may not be eligible for an offer. Apply to know if you’re approved and find out your exact welcome offer amount – all with no credit score impact. If you’re approved and choose to accept the Card, your score may be impacted.

- Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year.

- Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year.

- New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App.

- Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines.

- Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com.

- Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases.

- Pay It® lets you tap in the American Express® App to quickly pay for small purchase amounts throughout the month and still earn rewards the way you usually do. Plan It® gives you the option to split up big purchases into equal monthly payments with a fixed fee. You’ll know upfront exactly how much you’ll pay.

- Updated! $120 Dining Credit: Earn up to a total of $10 in statement credits monthly when you pay with the Gold Card at Grubhub (including Seamless), Buffalo Wild Wings, Five Guys, The Cheesecake Factory, and Wonder. This can be an annual savings of up to $120. Enrollment required.

- $100 Resy Credit: Get up to $100 in statement credits each calendar year at over 10,000 qualifying U.S. Resy restaurants after you pay for eligible purchases with the American Express® Gold Card. That’s up to $50 in statement credits semi-annually. Enrollment required.

- $84 Dunkin' Credit: Earn up to $7 in monthly statement credits after you pay with the American Express® Gold Card at U.S. Dunkin’ locations. Enrollment required.

- $120 Uber Cash on Gold: Enjoy up to $120 in Uber Cash annually with your Gold Card. Just add your Card to your Uber account and you'll get $10 in Uber Cash each month to use on orders and rides in the U.S. when you select an Amex Card for your transaction.

- New! As an American Express® Gold Card Member, you can enjoy complimentary Hertz Five Star® Status. Enjoy benefits like skipping the counter at select locations, adding an additional driver at no additional cost*, and vehicle upgrades**. Benefit enrollment and Hertz Gold+ registration are required. *Additional drivers must meet standard rental qualifications and must be a spouse or domestic partner to qualify as complimentary. Other additional drivers subject to fees. **Benefits are subject to availability and vary by location. Additional Hertz program Terms and Conditions including age restrictions apply.

- Take advantage of a $100 credit towards eligible charges* at over 1,300 upscale hotels worldwide when you book The Hotel Collection through AmexTravel.com or the Amex Travel App **. *Eligible charges vary by property. **The Hotel Collection requires a two-night minimum stay.

- Book your travel through the Amex Travel App with added peace of mind – backed by American Express® service and support. Only for American Express® Card Members.

- Whenever you need us, we're here. Our Member Services team will ensure you are taken care of. From lost Card replacement to statement questions, we are available to help 24/7.

- No Foreign Transaction Fees.

- Annual Fee is $325.

- Terms Apply.