Battle of the Metal Credit Cards — Which Is the Strongest?

Update: Some offers mentioned below are no longer available. View the current offers here.

Over the last few years we've seen a dramatic rise in metal credit cards. What used to feel special, like it or not, has become nearly commonplace. You can blame the Chase Sapphire Reserve card for this situation. The marketing campaign was so successful that Chase actually ran out of metal to make the cards. Then, in 2017, American Express re-introduced the Platinum Card® from American Express as a sleek metal card. And not to be left out, Citibank followed by turning the Citi Prestige into a metal alloy card. And those are just a few examples of the new, non-plastic generation of cards.

Best Metal Credit Cards of 2019 by Strength

- Mastercard® Black Card™

- American Express Platinum Card

- The Business Platinum Card® from American Express

- Delta SkyMiles® Reserve American Express Card

- American Express Business Centurion Card

- Ritz-Carlton Rewards Card

- American Express Platinum Card

- U.S. Bank Altitude Reserve Card

- Capital One Venture Rewards Credit Card

- American Express® Gold Card

- Marriott Bonvoy Brilliant™ American Express® Card

- Chase Sapphire Reserve

- Chase Sapphire Preferred Card

- Citi Prestige

Metal Credit Card Strength Test

The market today has more than a dozen metal cards at last count, with Amex more recently rebranding its Premier Rewards Gold product as the American Express® Gold Card and giving it a nice metal facelift too. More are likely to emerge (the first came from American Express in the form of a Centurion card made of titanium in 1999), but there are differences among cards. You can feel when a product is relatively heavy (like the Ritz-Carlton Rewards Credit Card) and thick. Or when the metal is so thin and malleable that you aren't even sure if it's metal (like the Citi Prestige metal cards when we first got them).

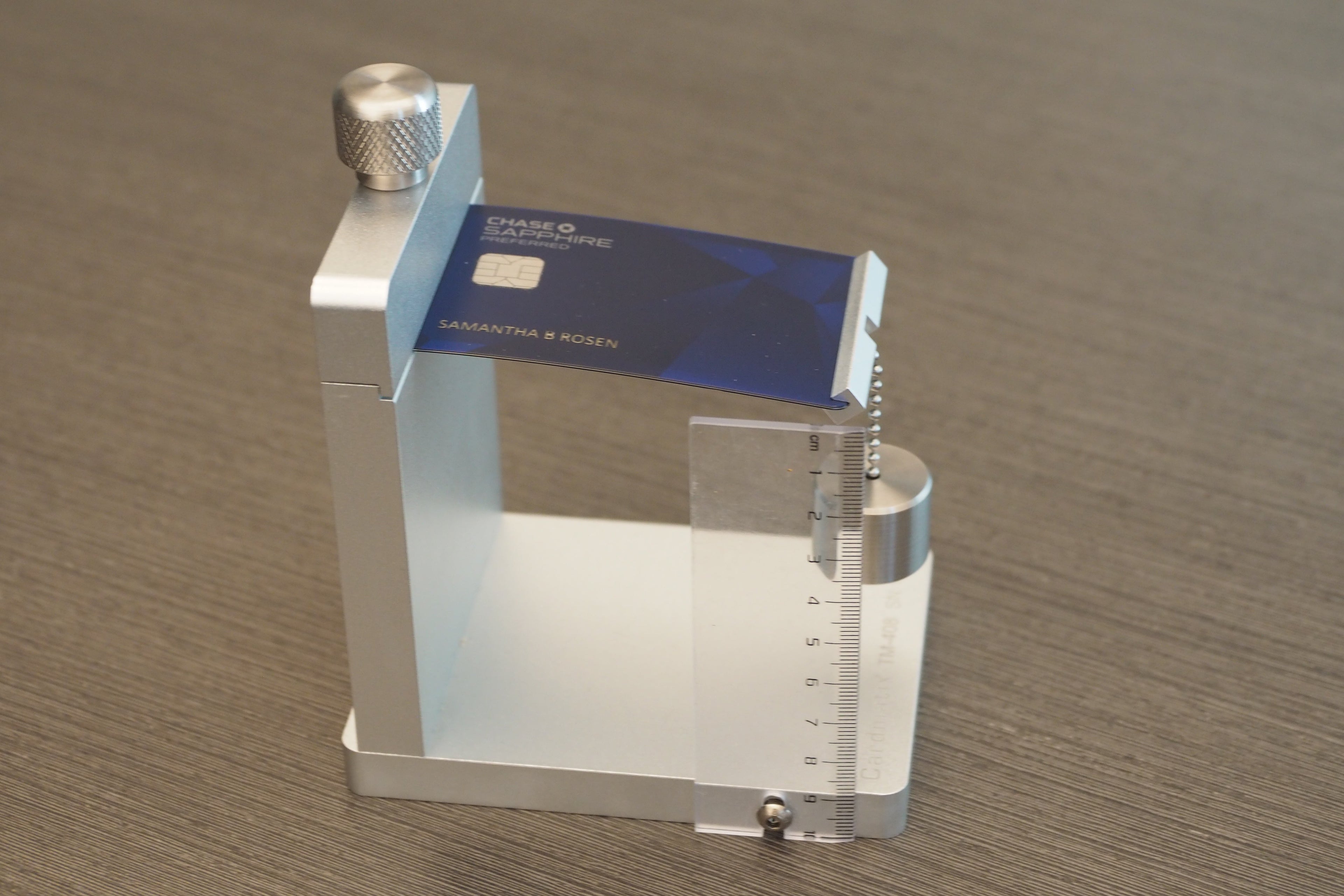

After some investigation, we discovered that metal credit-card bending is a science. In fact, there is a machine specifically made for gauging credit card sturdiness. It is the aptly named "Bending Stiffness Gauge" manufactured by Cardmatix, a company with offices in California and China. Cardmatix describes the $525 device as follows:

This fixture is designed to hold a test card in a cantilevered position. Card placement is a snap with a large tensioning knob. Once clamped in the test position, a stainless steel weight - calibrated to apply a force of 0,7N - is applied on the opposite edge of the card body. The resulting deformation is measured using the integrated ruler. It is crafted from aircraft grade 6061 aluminum alloy bar stock and electrostatically coated for a durable long-lasting finish. Fittings and test weights are made of stainless steel.

To test a card, you stick one end into the device, twist the top to fasten the card into place, and then attach the provided weight at the other end of the card. The metal block weighs about 70 grams (2.5 ounces). Once everything is set up, you attach a ruler to the side and measure the distance between the weight and the bottom of the machine. It looks like this:

We got our hands on one of these devices and tested as many metal cards as we could find. The lower the number in the bend column, the stronger the card is.

Here's how the different cards stack up against each other in our tests. This includes the bend as well as the weight.

| Credit Card | Bend (millimeters) | Weight (Grams) |

|---|---|---|

Mastercard Black Card | .5 | 21.54 |

American Express Platinum Card | 1 | 18.6 |

The Business Platinum Card® from American Express | 1 | 18.8 |

American Express Platinum Card (contactless) | 2 | 17.34 |

Delta SkyMiles Reserve American Express | N/A | 17.18 |

Apple Card | 2 | 14.75 |

U.S. Bank Altitude Reserve Card | 2.5 | 16.25 |

Capital One Venture Rewards Credit Card | 3 | 16.46 |

American Express® Gold Card | 4 | 14.73 |

Marriott Bonvoy Brilliant™ American Express® Card | 5 | 14.46 |

American Express Business Centurion Card | 2 | 12.56 |

Chase Sapphire Reserve | 6 | 12.41 |

Chase Sapphire Preferred Card | 7 | 12.37 |

Ritz-Carlton Rewards Card | 7 | 12.33 |

Citi Prestige | 7 | 11.46 |

Best Metal Credit Card Analysis

The strongest (least bendy) card is the Mastercard Black Card. For second place, there was a four-way tie between the Amex Platinum, Amex Business Platinum (which makes sense considering they use the same materials), the Amex Business Centurion and the Ritz-Carlton Rewards Card, each of which came in just half a millimeter behind the Mastercard Black Card. The contactless version of the Amex Platinum was a little more flexible, bending just 1 millimeter more than the second place finishers.

The Chase Sapphire Preferred and Citi Prestige tied for last place with 7 millimeters in bend; both are lighter than their heavy metal counterparts as well (12 and 11 grams, respectively).

The award for heaviest card goes to the Ritz-Carlton Rewards Card (which has been closed for applications), in fact, it's about 30% more heavy than the Mastercard Black Card, which was the second-heftiest product.

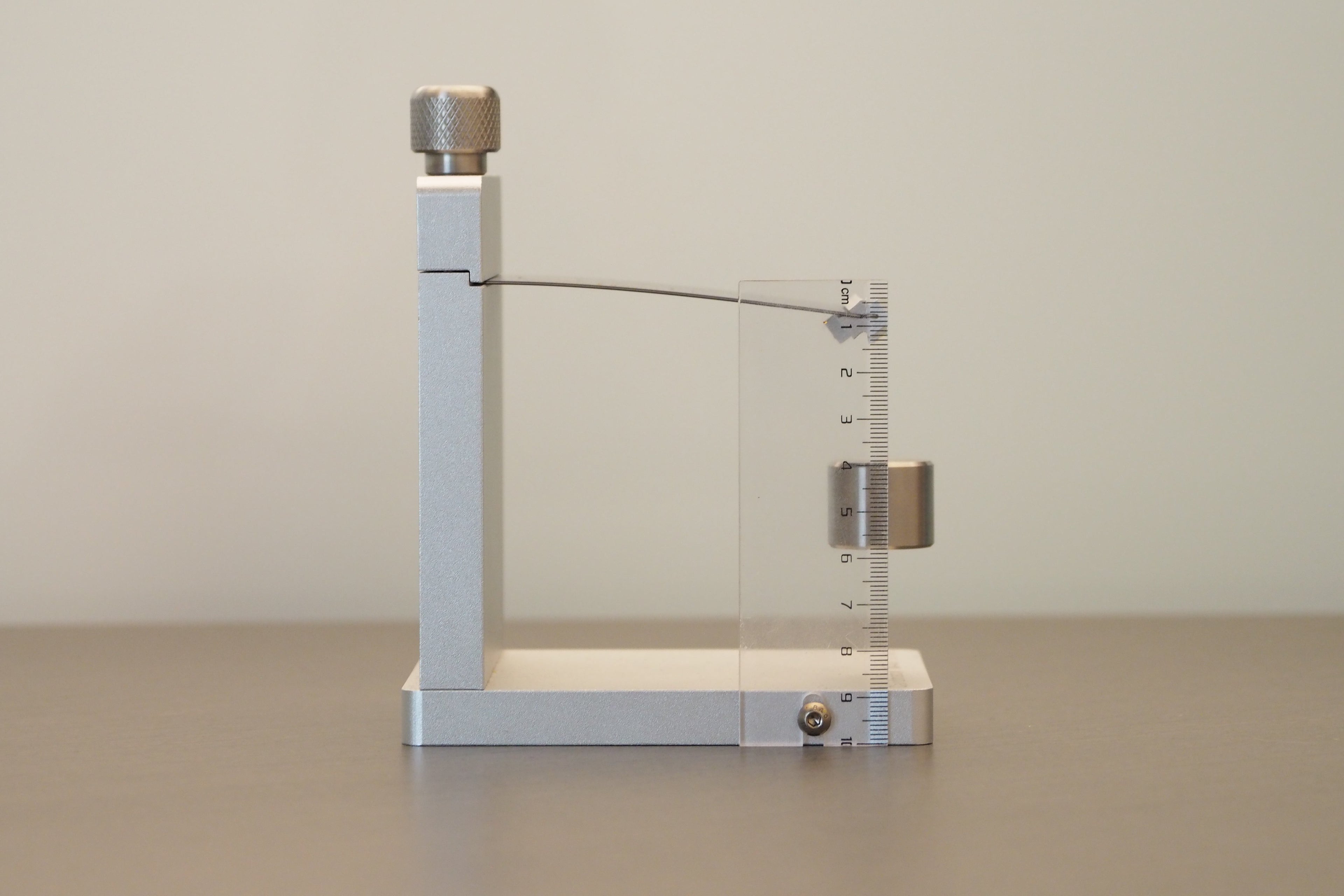

You can get a better sense of how weak some cards are by looking at them in profile as they are being tested. Below is the Chase Sapphire Preferred — which is very flexible.

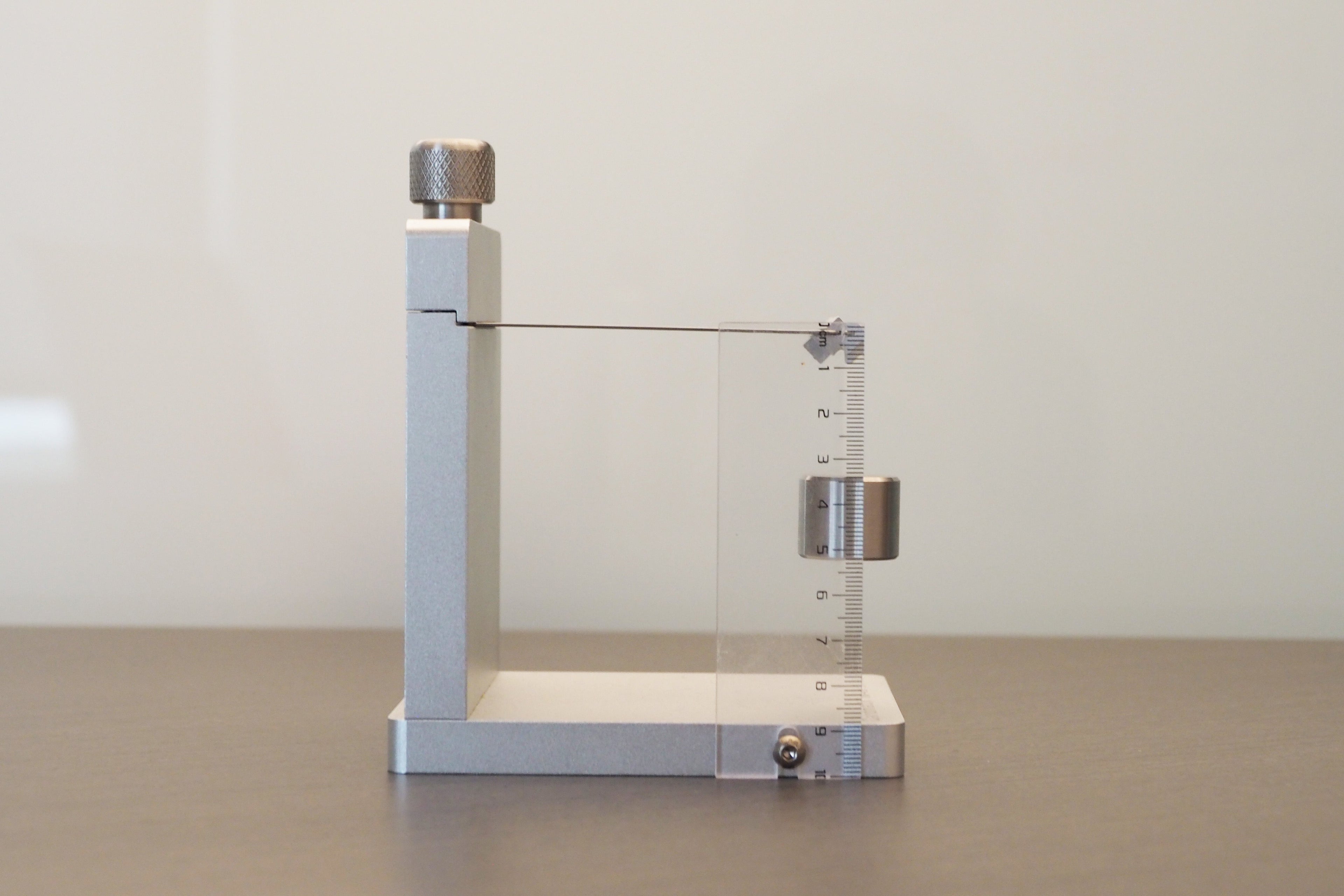

And the second strongest, The Amex Platinum:

Does heft really have any impact on the credit card market? Does it change which card you whip out after a meal? Once upon a time, a thicker, stronger card may have been the status symbol — sturdy being more impressive than thin and wimpy. But we also realize that wallets are getting heavier with all of these metal cards. So maybe more bendability is actually preferred by some consumers. Let us know how you feel in the comments below.

Additional reporting provided by Elizabeth Hund.

All images by the author.