Here's why it matters which card you use to pay in the United MPX app

Update: Some offers mentioned below are no longer available. View the current offers here.

Reader Questions are answered twice a week by TPG Senior Points & Miles Contributor Ethan Steinberg.

One of the easiest ways to increase the amount of miles you earn in your day to day life is by looking for opportunities to "stack" or "double-dip," i.e. earning multiple different sets of miles on a single purchase. You can do this by taking advantage of an online shopping portal, but another popular option involves using the United MileagePlus X app to purchase gift cards at participating retailers and earn bonus miles. TPG reader Kyle wants to know if he can earn category bonuses (i.e. triple points on dining) on his MPX purchases ...

[pullquote source="TPG READER KYLE"]If you make a purchase through the MileagePlus X app for a gift card at a restaurant, it seems to code as "shopping" and not as "dining." Is there any way around that, and if not what's the best card to use with MPX?[/pullquote]

This is a great question Kyle, with a surprisingly simple answer that's worth bookmarking for future use. If you're not familiar with the United MileagePlus X (MPX) app, it's quite simple. You download the app on your phone and link it to your MileagePlus account. Then when you're shopping at one of their partner retailers, you log into the app and buy a gift card, usually in the exact amount of the purchase you're making (the gift cards are available for immediate use). In addition to the charge on your credit, card, you'll earn a certain number of bonus miles for every dollar you spend.

Related: New way to earn bonus United miles in MileagePlus X app

While most merchants set their own identification codes (telling credit card companies if they are a restaurant, hotel, grocery store, etc.) there's definitely variation in how different issuers process those codes and identify transactions. This has led to some issues in the past with cards not earning bonus points the way they should.

For example, the American Express® Gold Card earns 4x points at restaurants and U.S. supermarkets (up to $25,000 in purchases per calendar year, then 1x), but many readers have reported issues when dining at smaller restaurants that use payment processors like Square to process transactions. By comparison, the Chase Sapphire Reserve also earns 3x points on dining and travel, and it seems to do fine at restaurants that use Square.

But what does any of this have to do with the MPX app? The simple answer is that when using Amex cards, you won't receive any additional category bonuses (travel, dining, etc.). Since you're technically buying a gift card, you won't have any luck calling Amex and asking them to manually fix it either. Meanwhile, for reasons I honestly can't explain, Chase does give you category bonuses for United MPX purchases.

This matters most for dining purchases, as a large portion of United MPX partners are restaurants. Normally, the Amex Gold offers a better return than the Chase Sapphire Reserve. TPG values American Express Membership Rewards points and Chase Ultimate Rewards points evenly at 2 cents each, meaning the Amex Gold's 4x comes out to an 8% return while the Chase Sapphire Reserve's 3x comes out to a 6% return. However, when you factor in the bonus points you'd only earn if paying with the Sapphire, that can easily push it into the lead.

Related: Which purchases count as dining with Chase Sapphire Preferred and Chase Sapphire Reserve?

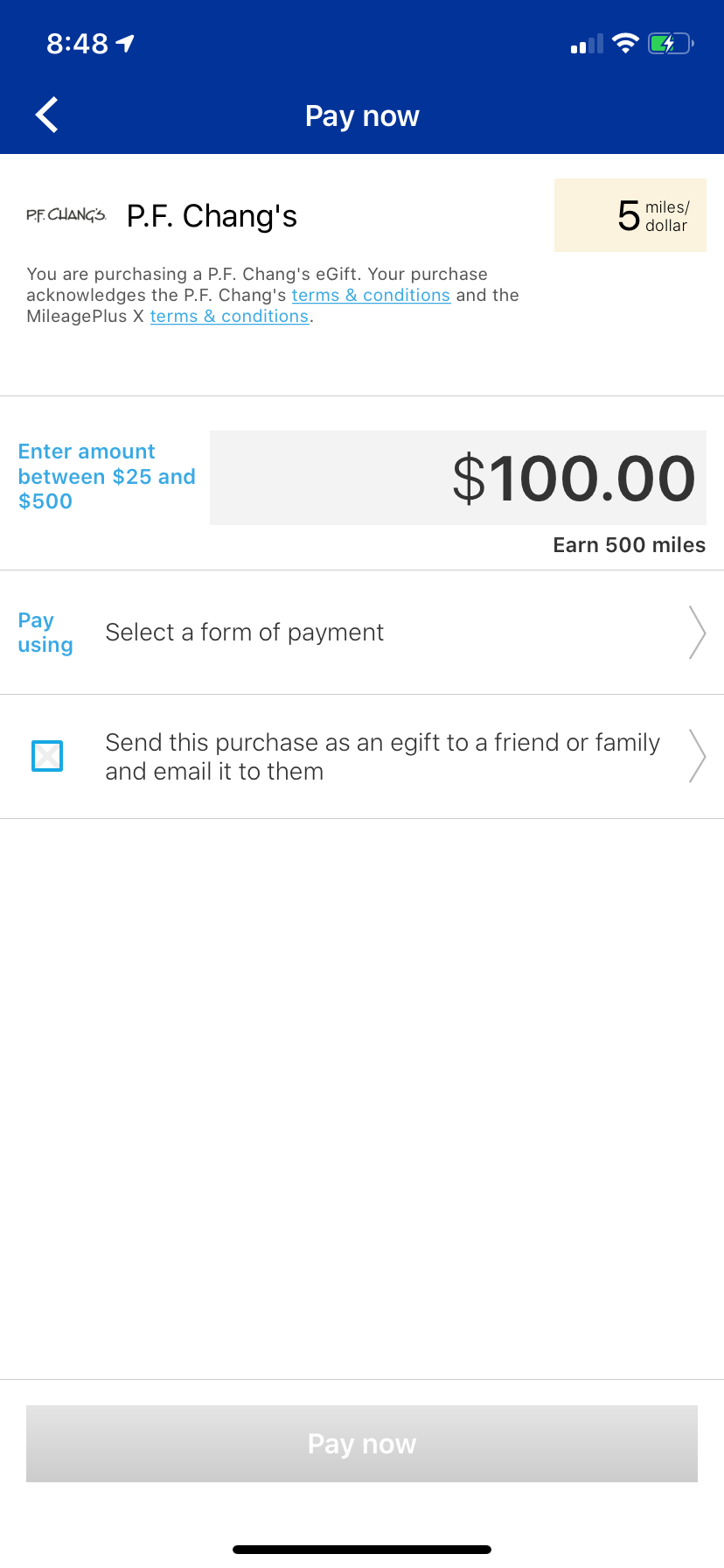

For example, if you spent $100 at PF Changs through the MileagePlus X app and used the Chase Sapphire Reserve for the purchase, you'd earn points and miles worth a total of about $12.50:

- 5x United Airlines miles = 500 miles (worth $6.50 based on TPG valuations)

- 3x Chase Ultimate Rewards points = 300 points (worth $6 based on TPG valuations)

But if you used the Amex Gold through the MileagePlus X app, it would code as shopping rather than dining and you'd only earn 1x Membership Rewards points on top of the United miles, or effectively $8.50 worth of points and miles:

- 5x United Airlines miles = 500 miles (worth $6.50 based on TPG valuations)

- 1x Amex Membership Rewards points = 100 points (worth $2 based on TPG valuations)

If you skipped the MileagePlus X app altogether and paid directly at PF Changs, you'd earn 4x Membership Rewards points or 400 points, worth $8.

Of course, if you don't have a Chase Sapphire Reserve card this discrepancy is much less important. In that case, you should focus on a card that offers a great return on everyday spending, like the Chase Freedom Unlimited.

Related: The best credit cards for dining out — and ordering in

Bottom line

If you're using the United MPX app, you already have the right idea. This can be a great opportunity to rack up bonus miles on purchases you already planned to make, but paying with the right travel rewards credit card can supercharge your returns even more. If you're buying a gift card for any type of restaurant, you'll want to try and pay with a Chase Sapphire card to make sure you get your dining category bonus in addition to the extra United miles.

Thanks for the question, Kyle, and if you're a TPG reader who'd like us to answer a question of your own, tweet us at @thepointsguy, message us on Facebook or email us at info@thepointsguy.com.