Why you shouldn't open a store credit card during the holiday season

Editor's Note

Not long ago, I was at Home Depot with my mom, grabbing a few things she needed, like lightbulbs and air filters. A friendly employee wearing the store's iconic orange apron greeted us.

The employee then offered my mom the opportunity to open a Home Depot credit card and receive $25 off her purchase — nearly offsetting the price of my mom's entire cart. As my mom reached for the application, my credit card instincts triggered a reaction uncannily similar to a panic attack. Nobody was opening a store credit card with a $25 welcome bonus if I had anything to say about it.

Related: 4 reasons store credit cards are (almost) always a bad idea

Around the holidays, it's especially easy to fall for an in-store credit card sales pitch at checkout. Many retailers will give you a 10% or 20% discount if you apply for a card on the spot. And while saving even $50 or $100 can seem enticing, there are many reasons to avoid opening a store credit card. Plus, there are shopping tricks (like making purchases through an online portal) that can give you nearly as big of a discount without the need for a hard credit pull.

If you're going to open a new card, choose a true rewards credit card instead of one at the store. The miles, points or cash back you earn with these cards (including certain no-annual-fee cards) can be worth much more than a one-time discount at checkout. They can also come with valuable sign-up bonuses that can be worth hundreds of dollars in cash back — or thousands in free travel. Plus, their ongoing benefits can provide plenty of value in the long term.

Why store cards may be bad for your credit score

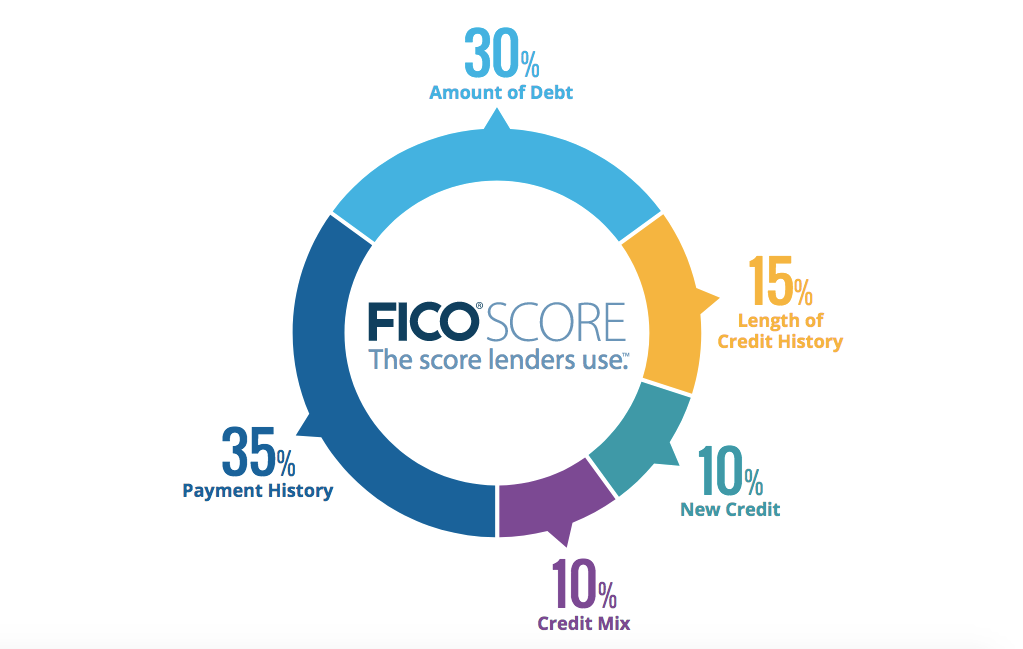

Everyone knows the importance of a good credit score. It's a metric that banks use to determine your creditworthiness when you're applying for a loan for a car, a home mortgage, a credit card, and more. However, not everyone realizes the factors that go into calculating your credit score. Payment history is one important factor, which is why we always urge you to pay card balances on time and in full each month.

But another important factor (30% of your credit score, according to FICO) is your credit utilization ratio, which is the amount of your card balances divided by your total available credit across all of your cards.

In my experience, the credit limit you get on a store credit card typically isn't much higher than the amount of your purchase. If you're spending $1,000, for instance, you might get a $3,000 credit limit. Although your credit utilization score is often calculated as your amounts owed compared to your entire line of credit across all your credit cards, creditors also sometimes consider your per-card utilization. In this particular example, the utilization ratio for your new card account would be a whopping 33%, which might negatively impact your credit score.

Ideally, it's best to keep your credit utilization below 10%. I always strive for 3% or less — which means I have to pay off big purchases quickly. Remember never to spend more than you can pay off in full, and consider paying off your balance before the billing cycle ends.

Related: Credit utilization ratio: What it is and how it affects your credit score

Utilize shopping portals and rewards card discount offers with retailers

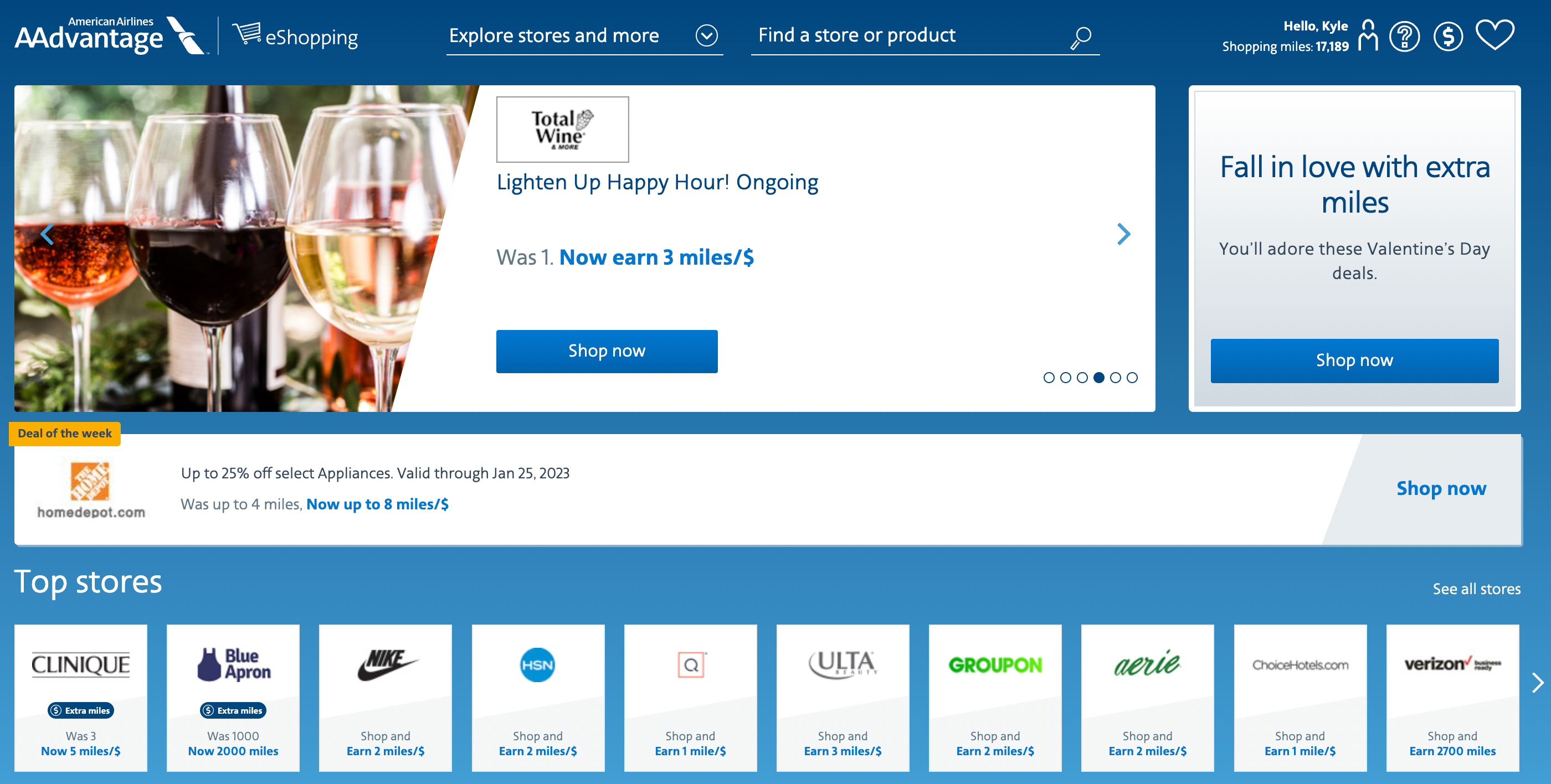

You don't need a store credit card to save money or get a discount when shopping. For example, online shopping portals offer an easy way to earn tons of bonus miles, points or cash back at many popular retailers. We've seen deals like 15% cash back (or 15 Amex points per dollar) through Rakuten on many popular retailers during Black Friday and Cyber Monday week, and such offers will surely pop up again throughout the holiday season.

Nearly every airline, hotel, or bank has some kind of shopping portal to help you earn rewards when shopping online. Nowadays, many retailers allow you to shop online and pick up in the store. These portals are a really easy extra way to earn rewards for your purchase.

Read our guide to maximizing online shopping portals to learn how to quickly check which portal offers the best return rate for your purchase.

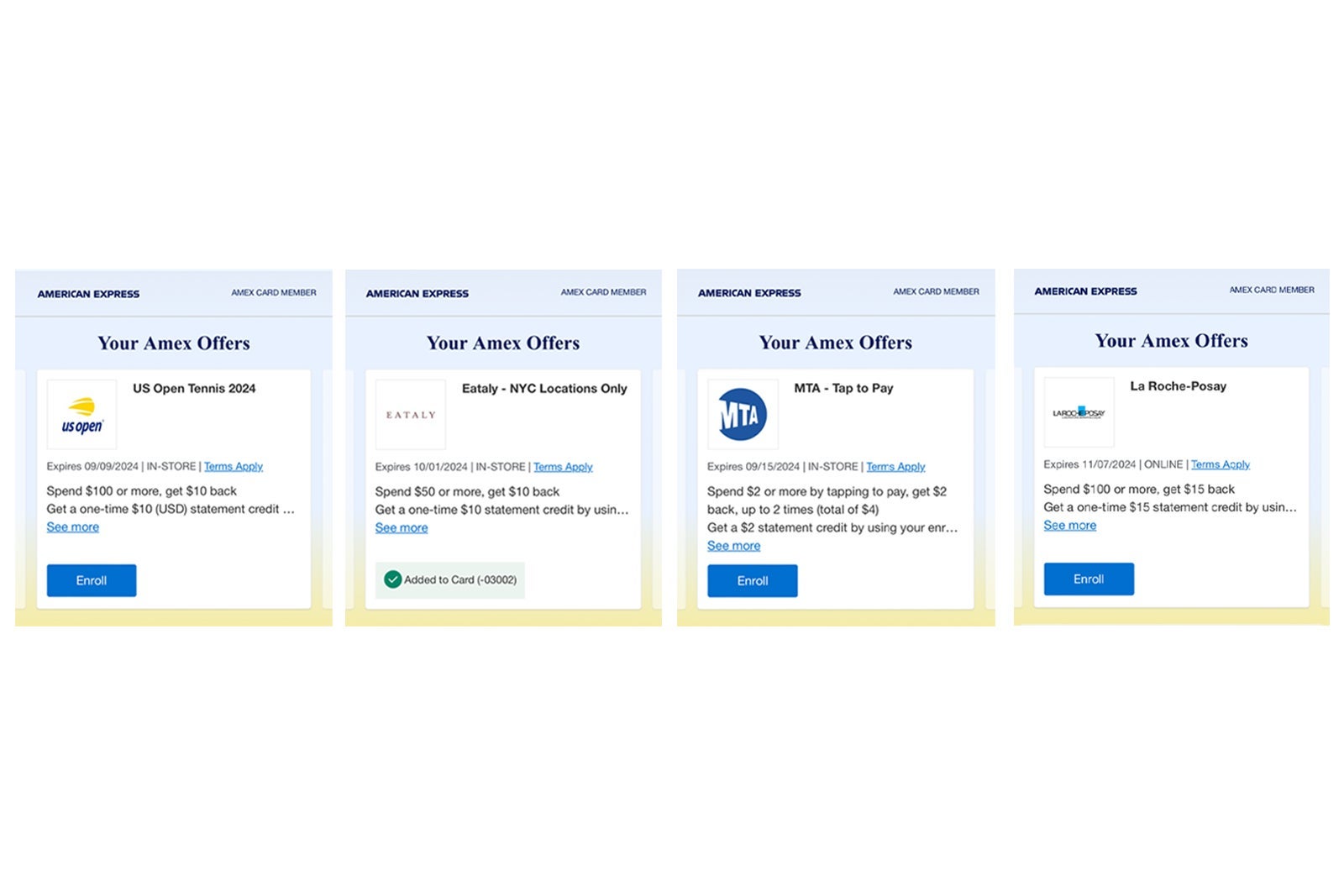

The best American Express cards come with Amex Offers, which are basically souped-up coupons that help you earn easy bonus points or save money on in-store or online purchases. These targeted offers include deals like 20,000 bonus points if you hit a certain purchase dollar amount, 10% discounts on popular retailers or $100-plus statement credits when you shop at specific merchants. You can often combine an offer with other coupons or discount codes to get even more savings.

Bookmark our Amex Offers page so you don't miss the latest deals — and learn how to stack multiple deals in our guide to maximizing holiday purchases.

Bottom line

Instead of falling for a store credit card, use shopping portals or rewards card offers to get similar savings. You can always check our best credit card offers page, too, and consider better alternatives that deliver long-term value. You'll find travel and cash-back credit cards that come with $750 or more in cash back after you meet minimum spending requirements — some with no annual fee. Also, check out our guide to sign-up bonuses of more than 100,000 points, which we update frequently. From those bonuses, you can reap value on the scale of hundreds of dollars in cash or thousands of dollars in travel.

Related: The beginners guide to airline shopping portals: How to earn bonus points and miles

TPG featured card

at American Express's secure site

Terms & restrictions apply. See rates & fees.

| 4X | Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 4X | Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 5X | New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App. |

| 3X | Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines. |

| 2X | Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com. |

| 1X | Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases. |

Pros

- Valuable dining and food-related credits

- Flexible rewards with airline and hotel transfer partners

- Multiple travel and purchase protections

- No foreign transaction fees

- Access to Amex Offers for additional savings (enrollment required)

Cons

- Not as useful for those living outside the U.S.

- Some may have trouble using Uber and other dining credits

- You may be eligible for as high as 100,000 Membership Rewards® Points after you spend $8,000 in eligible purchases on your new Card in your first 6 months of Card Membership. Welcome offers vary and you may not be eligible for an offer. Apply to know if you’re approved and find out your exact welcome offer amount – all with no credit score impact. If you’re approved and choose to accept the Card, your score may be impacted.

- Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year.

- Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year.

- New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App.

- Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines.

- Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com.

- Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases.

- Pay It® lets you tap in the American Express® App to quickly pay for small purchase amounts throughout the month and still earn rewards the way you usually do. Plan It® gives you the option to split up big purchases into equal monthly payments with a fixed fee. You’ll know upfront exactly how much you’ll pay.

- Updated! $120 Dining Credit: Earn up to a total of $10 in statement credits monthly when you pay with the Gold Card at Grubhub (including Seamless), Buffalo Wild Wings, Five Guys, The Cheesecake Factory, and Wonder. This can be an annual savings of up to $120. Enrollment required.

- $100 Resy Credit: Get up to $100 in statement credits each calendar year at over 10,000 qualifying U.S. Resy restaurants after you pay for eligible purchases with the American Express® Gold Card. That’s up to $50 in statement credits semi-annually. Enrollment required.

- $84 Dunkin' Credit: Earn up to $7 in monthly statement credits after you pay with the American Express® Gold Card at U.S. Dunkin’ locations. Enrollment required.

- $120 Uber Cash on Gold: Enjoy up to $120 in Uber Cash annually with your Gold Card. Just add your Card to your Uber account and you'll get $10 in Uber Cash each month to use on orders and rides in the U.S. when you select an Amex Card for your transaction.

- New! As an American Express® Gold Card Member, you can enjoy complimentary Hertz Five Star® Status. Enjoy benefits like skipping the counter at select locations, adding an additional driver at no additional cost*, and vehicle upgrades**. Benefit enrollment and Hertz Gold+ registration are required. *Additional drivers must meet standard rental qualifications and must be a spouse or domestic partner to qualify as complimentary. Other additional drivers subject to fees. **Benefits are subject to availability and vary by location. Additional Hertz program Terms and Conditions including age restrictions apply.

- Take advantage of a $100 credit towards eligible charges* at over 1,300 upscale hotels worldwide when you book The Hotel Collection through AmexTravel.com or the Amex Travel App **. *Eligible charges vary by property. **The Hotel Collection requires a two-night minimum stay.

- Book your travel through the Amex Travel App with added peace of mind – backed by American Express® service and support. Only for American Express® Card Members.

- Whenever you need us, we're here. Our Member Services team will ensure you are taken care of. From lost Card replacement to statement questions, we are available to help 24/7.

- No Foreign Transaction Fees.

- Annual Fee is $325.

- Terms Apply.