Tips on how to save for retirement

We've partnered with American Express to bring you personal finance insights, advice and more. Check out Credit Intel, Amex's financial education center, for more personal finance content.

If you spend any time on Facebook, Reddit or other online forums, you'll notice a massive overlap between award travel enthusiasts and the personal finance communities. Not only do these groups share the belief that they can improve their own standing in life by thinking outside the box and making small but meaningful changes that compound over time (like switching to a credit card with a higher earning rate for everyday spending), but you need a lot of the same skills to do well in each area, like the ability to think long term and delay gratification.

One of the most important goals of personal finance is saving for retirement, perhaps the ultimate example of making decisions today with benefits you won't reap for years or even decades to come. Join us today as we take a look at some strategies to help you save and retire early. Of course, before making any major decisions you should consult with a professional financial advisor to see how these ideas can be best applied to your own circumstances.

How much do you need?

Whenever you're setting a goal, be it saving up for an award flight or for retirement, you need to know how much you need in order to plan effectively. Financial advisors will give you a whole slew of different answers if you ask them this question, but one of the most commonly accepted (and data driven) answers is that you need 25x your annual expenses in order to retire. Another way to look at this is that once you retire, you can withdraw 4% of your portfolio every year (accounting for inflation) and have a 98% chance of your money lasting you at least 30 years. Since 4% is 1/25 of 100, this is how we get the 25x number, also commonly referred to as "the 4% rule."

This number isn't just invented out of thin air, it dates back to the Trinity Study, a landmark paper published in 1998 that examined the success of different withdrawal rates (1%, 2%, etc.) throughout different historical scenarios. In this case success rate means any scenario where the person didn't run out of money during the time period being studied. The authors covered every time period from 1925 to 1995, including several serious recessions and major bull markets. They came up with the following results for an investor with a portfolio of 75% stocks and 25% bonds:

Rate of withdrawal (3%-8%)

| 3% | 4% | 5% | 6% | 7% | 8% | |

|---|---|---|---|---|---|---|

15 years | 100% | 100% | 100% | 97% | 82% | 72% |

20 years | 100% | 100% | 95% | 81% | 68% | 53% |

25 years | 100% | 100% | 84% | 69% | 59% | 47% |

30 years | 100% | 98% | 78% | 59% | 48% | 37% |

35 years | 100% | 93% | 69% | 55% | 38% | 26% |

40 years | 100% | 92% | 66% | 45% | 30% | 6% |

An average individual retiring in their early 60s should be planning for at least 30 years of retirement income. The 3% withdrawal rate ends up being too conservative in most cases, with 4% being a sweet spot that prevents over-saving and still gives you a 98% chance of your money lasting through your retirement, according to the 4% rule. You can mitigate even that minor 2% risk by cutting back on unnecessary expenses if the market drops, to avoid selling your investments at a lower rate.

One common mistake people make is that they assume their expenses in retirement will be the same as they are now. Some things (like a mortgage, work related expenses or the cost of raising children) will go down, while other things like healthcare, travel and other leisure activities may go up. You also need to consider whether you'll have any other sources of income in retirement, such as Social Security, an employer sponsored pension, or any side income you might be generating. Using the 4% rule, a couple with $70,000 in annual expenses would need $1.75 million to retire safely. However, if they expect $20,000 in annual income from a pension, they really only need to replace $50,000 in income, dropping their retirement goal a full half a million to $1.25 million. Without getting too close to the third rail of politics, you need to consider the fact that Social Security payouts may be reduced in the future, or a pension fund may become insolvent.

Understand your risk tolerance

If you earn a high income but pile your savings under a mattress, over time the value of that money will be eaten away by inflation, leaving you with less than you started with. Putting it in a bank isn't much better, as most banks pay interest rates under the historical rate of inflation (about 2%). If you want to speed up your timeline to retirement (or to afford yourself a more luxurious lifestyle when you retire), you'll need to get your money working for you by investing it. You have plenty of options to choose from, including stocks, bonds and real estate, but you'll need to decide how comfortable you are taking risks.

If you're 22 years old and just starting your first job out of college, hopefully you're deciding to put some money away in a 401(k). While the crash of 2008 may feel like a distant memory, I have some news for you: Over the 40-50 years that you'll be investing in the market, you can expect at least one or two crashes of that size to happen again, along with plenty of "smaller" corrections of 10-20%. 2008 was a painful time for many Americans, but the only way you lost money in the market was if you sold at the bottom. The S&P500 had fully recovered to its pre-crash highs within five years, meaning that those who held on to their investments and ignored the doom and gloom in the news didn't actually lose anything. It's hard to say how you'll behave when the market crashes if you haven't lived through one before, but you'll want to pick an asset allocation that you're comfortable with, so you don't panic and sell when the market goes down.

Start young, start early

Albert Einstein is often famously quoted as saying "Compound interest is the eighth wonder of the world. He who understands it, earns it. He who doesn't pays it." When you invest, you earn some kind of return. Maybe it's a dividend from a stock or bond, rent money from a real estate property, or maybe the thing you bought (again, stocks, bonds or property) went up in value. Compound interest refers to the fact that over time, the interest you earned will start to earn interest itself, and that interest will earn interest and so on.

Related Article: What is Compound Interest & How is it Calculated?

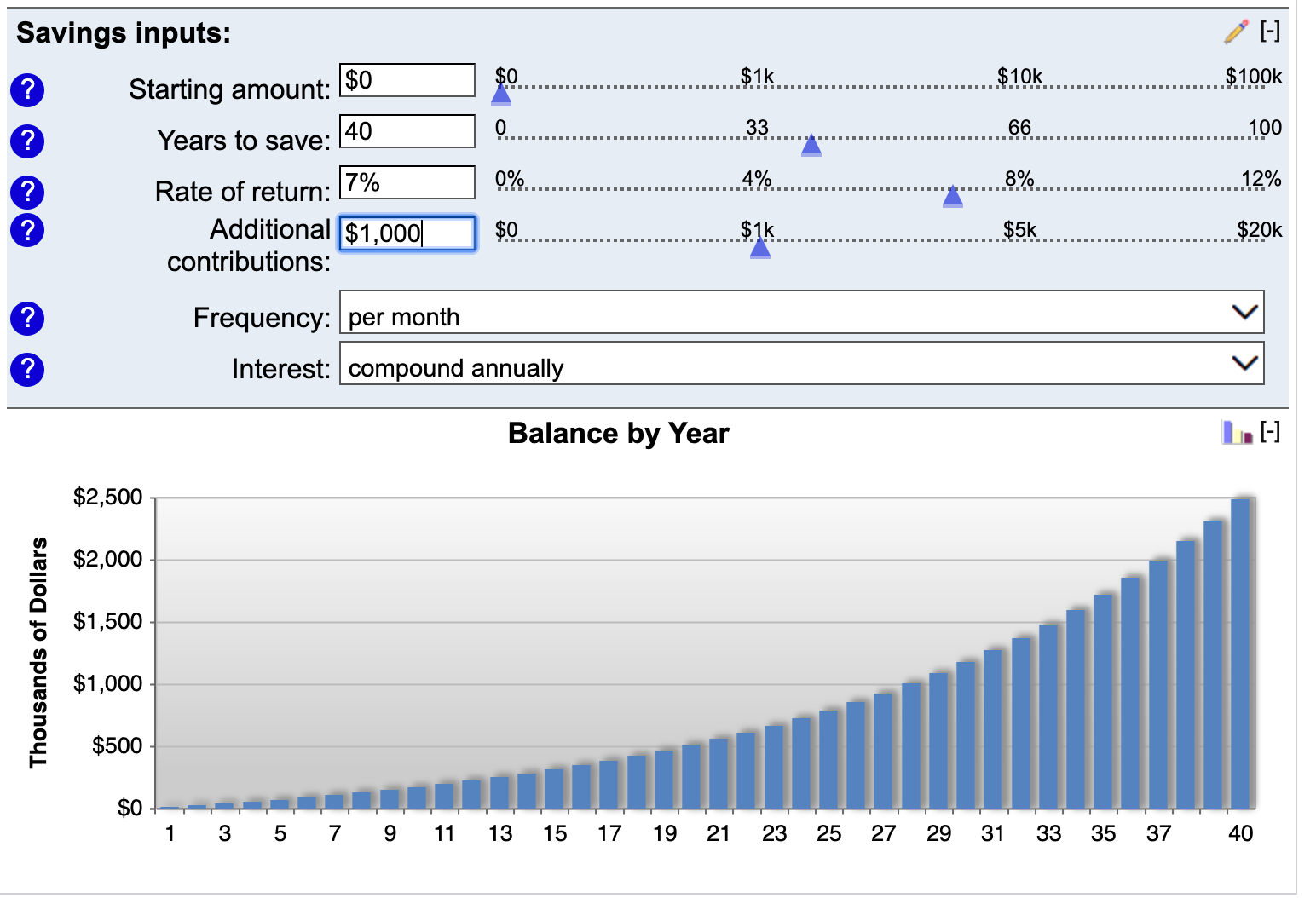

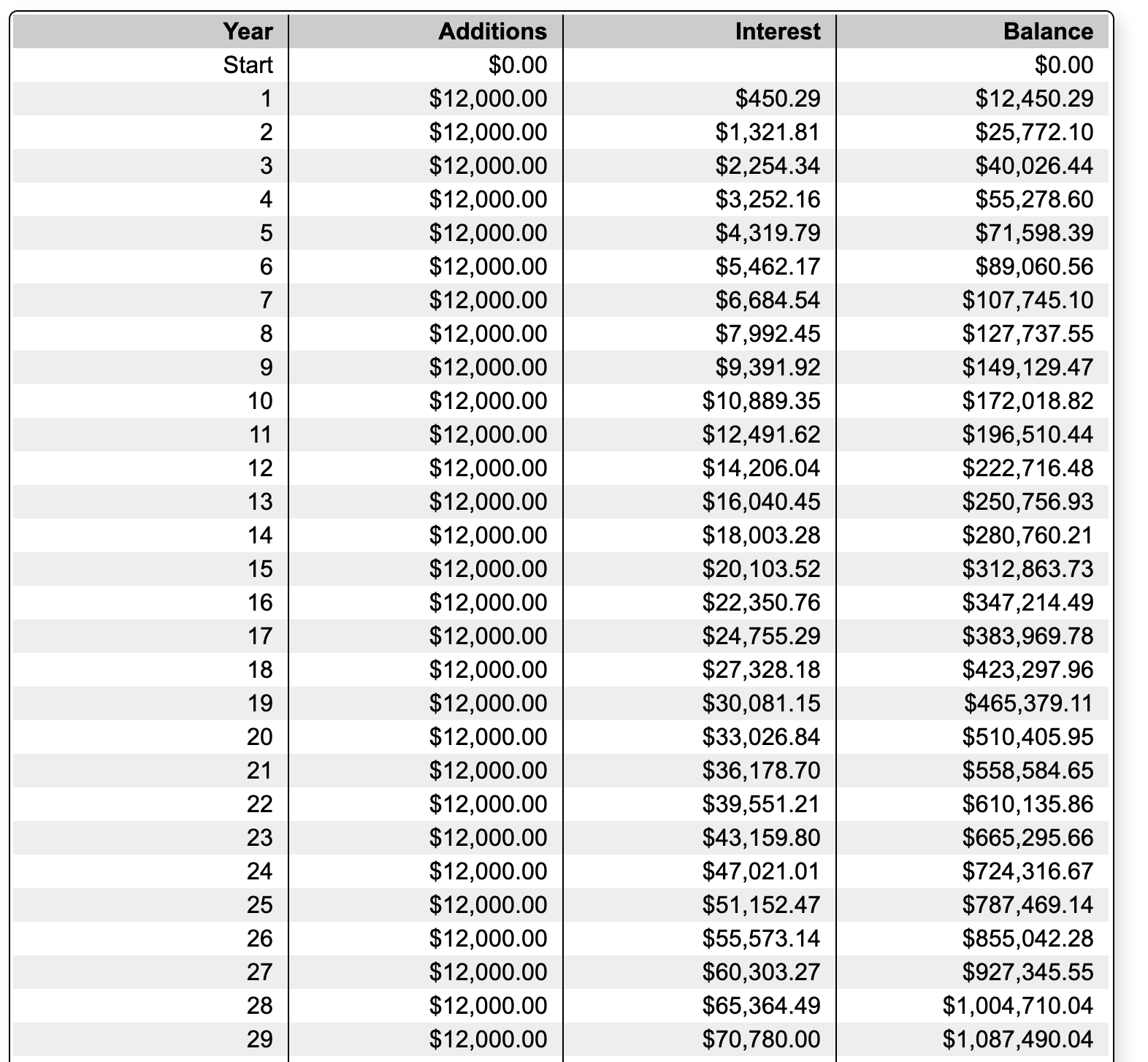

Many people have trouble visualizing this exponential growth, especially when they're just learning how to invest for the first time. One of the biggest lightbulb moments in my personal finance journey was when I started playing around with a compound interest calculator to see how much my money could grow. If you save $1,000 a month for 40 years, and you earn a 7% rate of return (which is close to the historical average of the US stock market), how much do you think your money will grow into?

In addition to the $480,000 you yourself will contribute, your investments will return a whopping ~$2 million dollars, giving you a grand total of $2.5 million. If you think back to the 4% rule from before, this equates to about $100,000 a year in comfortable retirement spending.

The real magic comes from looking at the year by year break down. By just the 11th year, the money your investments are making you is greater than the amount of new money you're contributing. By the 30th year your investments are making you about $75,000 (or six years of contributions), and by the 40th year they're making over $160,000 while you sleep, travel the world, or spend time with your family.

Einstein's quote was so insightful because it points out the dangers of waiting to start investing. Compound interest works in such a way that the last years of investing are worth exponentially more than the first years. Every year you wait to get started, you're giving up those valuable years on the backend. There's a popular story that illustrates these dangers by looking at two different investors (let's just call them Miles and Hootie).

These young pups had been friends growing up and knew the wisdom of saving for the future. Their parents each gave them $10,000 as a gift to get them started on the path to financial independence. At age 20, Miles started investing $5,000 a year in the stock market, averaging 8% returns. However, he stopped after just 10 years to focus on buying a house and supporting his family instead. Over those 10 years, he invested a total of $50,000.

Hootie, on the other hand, was a little later getting started. During his 20s he was so focused on acclimating to life in the workforce that he didn't save anything beyond that initial $10,000. Once he turned 30, he decided it was time to start saving and began investing $5,000 a year in the stock market every year until he turned 65. Over that time, he invested a total of $175,000. So, when Miles and Hootie met up down the road, who had done better? Let's take a look.

| Miles | Hootie | |

|---|---|---|

Initial balance | $10,000 | $10,000 |

Annual savings | $5,000 a year from 20 to 30, then nothing | Nothing until age 30, then $5,000 a year until age 65 |

Total amount invested | $50,000 | $175,000 |

Total interest earned | $1.6 million | $1.16 million |

Final balance | $1.67 million | $1.35 million |

Miles saved barely 1/3 the amount that his friend Hootie did, and he only saved for 10 years of his working career, unlike Hootie who saved for a whole 35 years. Yet just by starting a decade earlier and understanding the power of compound interest, Miles came out ahead, and by a whopping $300,000.

This is not meant to be discouraging if you're already in the middle of your career and haven't started saving for retirement yet. There's an ancient Chinese proverb that says "the best time to plant a tree was 20 years ago, the next best time is today." There's nothing you can do about the past, but if you've been telling yourself "oh, I can start saving next year," remember that you'll have to save a whole lot more to make up for the lost time.

Start by eliminating high interest debt

People often talk about compound interest in the context of saving and investing, but the same principles apply to debt. If you have high interest debt like a credit card, student loans or a car loan, the interest you're paying is compounding against you and often at a higher rate than your investments would compound. Before you start saving for retirement, many financial advisors recommend tackling all high interest debt to save on interest payments. It's up to you to decide what counts as "high interest" here, but I'd argue that anything over 6-7% and certainly anything over 10% should be a high payment priority. Once you finish paying off the debt, you can take that same line item in your budget and switch it over to retirement savings to start your journey.

Further Reading: How to Get out of Debt in 2020

Utilize tax advantaged accounts

Now that we've discussed the philosophy of saving for retirement and the importance of starting early, let's talk about some of the mechanics. The exact details will be slightly different depending on whether you're a full time employee (W-2) or part time/self employed (1099), but the overall strategies are the same.

The government wants to encourage people to take care of themselves by preparing for retirement, so they offer a number of tax deductions when you save in special tax advantaged retirement accounts, like a 401(k) or IRA. Once you put money into this account you can choose to keep it in cash, or invest it as you'd like, but most of the tax benefits come from the act of funding the account.

With a traditional 401(k) and IRA, you'll get a dollar for dollar tax deduction on the first $19,500 and $6,000 respectively. Additionally, if you're over 50 you can take advantage of a "catch-up contribution," letting you put an extra $6,500 into your 401(k) or $1,000 into your IRA. Note that these tax deductions are not the same as a tax credit. Contributing $5,000 to your 401(k) doesn't take $5,000 off your tax bill, it just reduces your taxable income by $5,000.

Most large employers offer a company 401(k) plan and may even include a match, essentially giving you free money to incentivize you to save. You should always take advantage of the match if you can, as it's a great way to boost your retirement savings without any extra contributions on your part.

Meanwhile if you're self-employed, you won't have access to a company sponsored 401(k) but you can set up your own individual 401(k) plan. This is a great hack to supercharge your retirement savings, as you're allowed to contribute as both the employer and employee. On the employee side you can still contribute $19,500 of pre-tax money each year, while as the employer you can contribute 25% or your annual profit/compensation, with the combined contribution not allowed to exceed $57,000. For a highly compensated self-employed individual in the top 37% tax bracket, contributing the maximum of $57,000 to an i401(k) would lead to a tax savings of approximately $21,000.

Money invested in a traditional 401(k) or IRA is allowed to grow tax free, meaning you won't pay any taxes on the proceeds of your investments until you start withdrawing them. You can begin withdrawing at age 59.5, but any withdrawals before that will incur a 10% penalty.

Traditional vs. roth

When saving for retirement, you get to decide if you'd rather pay taxes now or later. If you're early on in your career or in a unique situation (like an expat or student) that lowers your current tax rates, you might be better off opting for a Roth IRA or 401(k) instead of a traditional one. Roth contributions are not tax deductible, but the money that you invest grows tax free and can be withdrawn tax free once you turn 59.5. It's impossible to predict whether tax rates will go up or down decades from now and what path your own career will take, but if you're in a lower tax bracket now this is a great option to consider.

Pay yourself first

Knowing what you need to do to prepare for retirement is very different than actually doing it. One of the best financial habits you can form is paying yourself first. This means that you budget for savings and investing, and only spend whatever's left over on discretionary expenses instead of doing it the other way around. I like to take this one step farther: when I get paid, I make it a priority to move some money into my investment accounts before I start paying my bills. Even if I do both tasks in the same hour, the psychological effect of paying myself first helps me remember that I'm working to save, not working to spend.

Bottom line

Planning for retirement can be a daunting task, as most people will have no idea what their lives will look like 10, 20, or 40 years down the road. It can be scary to try and think that far ahead, but it helps to reframe the issue. Saving for retirement today is the best gift you can give your future self, to ensure that you'll be financially taken care of no matter what happens. Planning for the future opens doors, it doesn't close them, and I promise you that your future self will be thanking you when they see the magic of compound interest unfolding in front of their eyes.