Consumer credit is still improving amidst the pandemic: Here's how to keep your credit on track

I expected we'd see consumer credit worsen in 2020. After all, many Americans are out of work during the pandemic. We saw several credit card companies offer relief during the coronavirus crisis, but some cardholders struggled to access it. And some lenders found it difficult to assess creditworthiness during the pandemic.

But a recent Consumer Financial Protection Bureau study noted that consumer debt Hasn't skyrocketed. The study attributed this to many factors, including government payment assistance, decreased consumer spending and card issuers cutting credit limits. And now Experian's State of Credit 2020 report even shows that American consumer credit is improving, on average. So, today I'll take a closer look at Experian's report and what you can do to keep your owncredit on track.

Get the latest points, miles and travel news by signing up for TPG's free daily newsletter.

Experian's State of Credit 2020 report

Experian's State of Credit 2020 report showed that American consumers are still managing their credit responsibly despite the pandemic. Alex Lintner, group president of Experian Consumer Information Services, noted that "While it's difficult to predict when the economy will return to pre-pandemic levels, we are seeing promising signs of responsible credit management, especially among younger consumers."

Experian's 2020 report only compared 2020 data against 2019 data. But I also took a look at Experian's State of Credit 2019 report to gather the following data over the last four years:

| 2017 | 2018 | 2019 | 2020 | |

|---|---|---|---|---|

Average VantageScore | 675 | 680 | 682 | 688 |

Average number of credit cards (average number of retail credit cards) | 3.06 (2.48) | 3.04 (2.59) | 3.07 (2.51) | 3.0 (2.42) |

Average credit card balance (average retail credit card balance) | $6,354 ($1,841) | $6,506 ($1,901) | $6,629 ($1,942) | $5,897 ($2,044) |

Average revolving utilization rate | 30% | 30% | 30% | 26% |

Average nonmortgage debt | $24,706 | $25,104 | $25,386 | $25,483 |

Average mortgage debt | $201,811 | $208,180 | $213,599 | $215,655 |

Average 30 to 59 days past due delinquency rates | 4.0% | 3.9% | 3.9% | 2.4% |

Average 60 to 89 days past due delinquency rates | 1.9% | 1.9% | 1.9% | 1.3% |

Average 90 to 180 days past due delinquency rates | 7.3% | 6.7% | 6.8% | 3.8% |

This report defines retail credit cards as accounts with revolving terms. In short, cards with revolving terms have a credit limit and allow you to carry a balance from one month to the next.

I confirmed with Experian that it calculated the average number of credit cards, the average credit card balance and the average mortgage debt numbers excluding zero value. However, Experian computed the average utilization including zero value.

Related: 8 biggest factors that impact your credit score

Consumer use of credit cards and debt

In some areas, consumer credit habits have continued to follow the same trend. In positive news, the average VantageScore has increased each of the last four years. But, in not-so-good news, the average retail credit card balance, average mortgage debt and average non-mortgage debt have increased modestly each year.

Consumer credit habits have changed in some areas, though. For example, the average credit card balance increased for three years before dropping substantially in 2020. Past-due delinquency rates also dropped noticeably across the board in 2020. And although the average revolving credit utilization rate was 30% for the previous three years, in 2020 it dropped to 26%. All three of these decreases indicate a positive shift in consumer credit habits.

Finally, consumer behavior has bounced around over the last four years in several areas. For example, the average number of credit cards and the average number of retail credit cards haven't followed a noticeable trend. Both of these numbers are the lowest we've seen in the last four years. But, if you use credit cards responsibly, having multiple credit cards can be an excellent way to diversify your rewards and maximize your earnings.

Related: 13 expenses that you should not put on your credit card

Consumer credit by generation and state

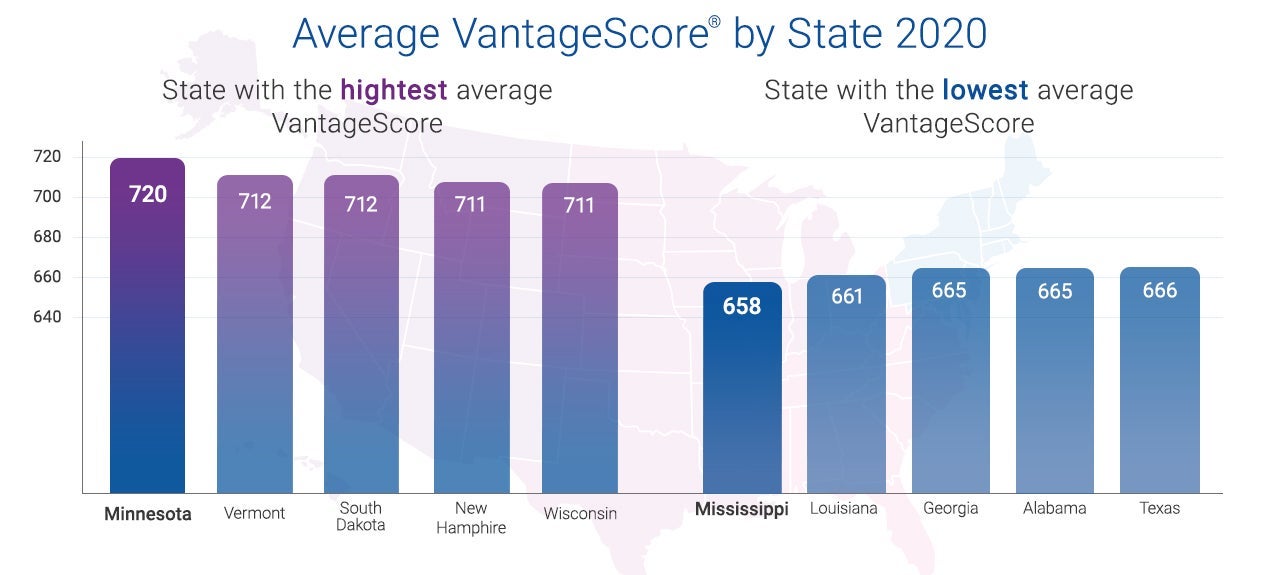

Experian also released information in its State of Credit 2020 report about specific generations and states. As you can see in the figure below, Minnesota had the highest VantageScore credit score, while Mississippi had the lowest VantageScore.

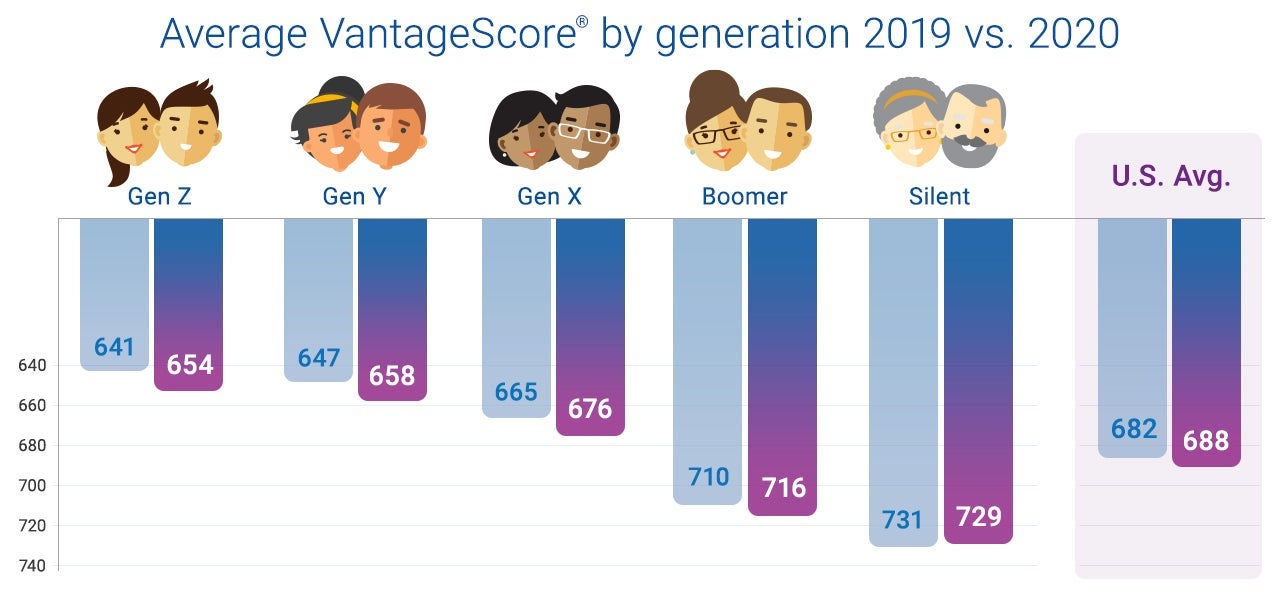

The report noted that Gen X consumers have the highest average credit card balance at $7,718 and credit utilization at 32%. Meanwhile, Gen Z consumers have the lowest average credit card balance at $2,197. And the Silent Generation has the lowest credit utilization, at 13%.

Average utilization rates decreased for every generation in the last year. But, Gen Z consumers reduced their credit utilization the most (6%), followed by Gen Y / Millennials (5%).

Gen Z and Gen Y consumers now carry more credit cards than they did in 2019, but their average credit card balance also decreased in the same period. So, this might indicate that Gen Z and Gen Y consumers are learning how to leverage multiple cards to maximize their rewards.

Related: Why I'm applying for travel credit cards during a pandemic

How to keep your credit on track

It's essential to keep your credit card balances, credit score and credit utilization on track as the pandemic continues. You may even want to recession-proof your credit score. Experian Senior Director of Consumer Education and Awareness Rod Griffin told The Points Guy:

While the pandemic has created serious financial challenges for many, we're seeing promising signs in terms of how consumers are managing their credit histories. As we travel the road to recovery from the COVID-19 pandemic, it will be important to maintain and protect your credit standing. Understanding your credit history and the factors that affect credit scores are key to emerging from this crisis with your finances intact.

Griffin went on to note that the most important thing you can do is be proactive. And Griffin provided The Points Guy with five steps you can take to keep your credit on track:

- Monitor your credit report by checking it regularly: Equifax, Experian and TransUnion are offering free weekly credit reports online through April 2021 at www.annualcreditreport.com.

- Continue to make payments on time: Late payments damage your credit history and drag down your credit scores. Plus, you may face interest and fees when you don't pay on time.

- Talk to your lender before being late on a payment: Your lender may have tools and resources to help you stay on time. And, in some cases, your lender may be willing to delay your payments temporarily. However, it's still best to make payments on time, if possible.

- Keep your credit card balances as low as possible: High credit card utilization is the second-most crucial credit score element. So, pay your balance in full each month if possible. And, if you must carry a balance, strive to pay it down. Doing so will improve your credit score and minimize the interest you incur.

- Use tools like Experian Boost: This free service allows you to bump up your credit scores by adding your cell phone, utility and streaming service payments to your credit report.

It's also a good idea to check your credit score regularly. If your credit score is lower than you'd like, see our guide on how to improve your credit. And, you may find it useful to make a budget or use a money management app.

Related: Seven ways to improve your finances in one week

Bottom line

Some Americans are facing financial struggles during the pandemic. But, other Americans seem to be using this time of quarantine, social distancing and stay-at-home measures as an opportunity to pay off debt. Overall, Experian's State of Credit 2020 report shows that American consumers have continued to improve their credit profiles despite the pandemic.

It's important to stay vigilant and proactive when it comes to your credit, especially during uncertain financial times. So, remember to pay your credit card balance in full each month, if possible. And remember one fundamental tenet of using rewards credit cards: the rewards aren't worth it if you're incurring interest and fees.

TPG featured card

at Capital One's secure site

Terms & restrictions apply. See rates & fees.

| 5X miles | Earn 5X miles on hotels, vacation rentals and rental cars booked through Capital One Travel |

| 2X miles | Earn unlimited 2X miles on every purchase, every day |

Pros

- Stellar welcome offer of 75,000 miles after spending $4,000 on purchases in the first three months from account opening. Plus, a $250 Capital One Travel credit to use in your first cardholder year upon account opening.

- You'll earn 2 miles per dollar on every purchase, which means you won't have to worry about memorizing bonus categories

- Rewards are versatile and can be redeemed for a statement credit or transferred to Capital One’s transfer partners

Cons

- Highest bonus-earning categories only on travel booked via Capital One Travel

- LIMITED-TIME OFFER: Enjoy $250 to use on Capital One Travel in your first cardholder year, plus earn 75,000 bonus miles once you spend $4,000 on purchases within the first 3 months from account opening - that’s equal to $1,000 in travel

- Earn unlimited 2X miles on every purchase, every day

- Earn 5X miles on hotels, vacation rentals and rental cars booked through Capital One Travel

- Miles won't expire for the life of the account and there's no limit to how many you can earn

- Receive up to a $120 credit for Global Entry or TSA PreCheck®

- Use your miles to get reimbursed for any travel purchase—or redeem by booking a trip through Capital One Travel

- Enjoy a $50 experience credit and other premium benefits with every hotel and vacation rental booked from the Lifestyle Collection

- Transfer your miles to your choice of 15+ travel loyalty programs

- Top rated mobile app