Don't let Chase's shutdown pattern bite you

Update: Some offers mentioned below are no longer available. View the current offers here.

In December 2017, TPG readers and members of several online points and miles communities began alerting us to a troubling experience: Chase shutting down of all their credit card accounts, and in many cases, terminating all of their Chase banking activities. Since 2018, I've continued to read and hear from many Chase customers who are now casualties of credit behavior which has resulted in losing access to arguably the most valuable credit cards and loyalty currency.

Related reading: How to maximize your Chase Ultimate Rewards points

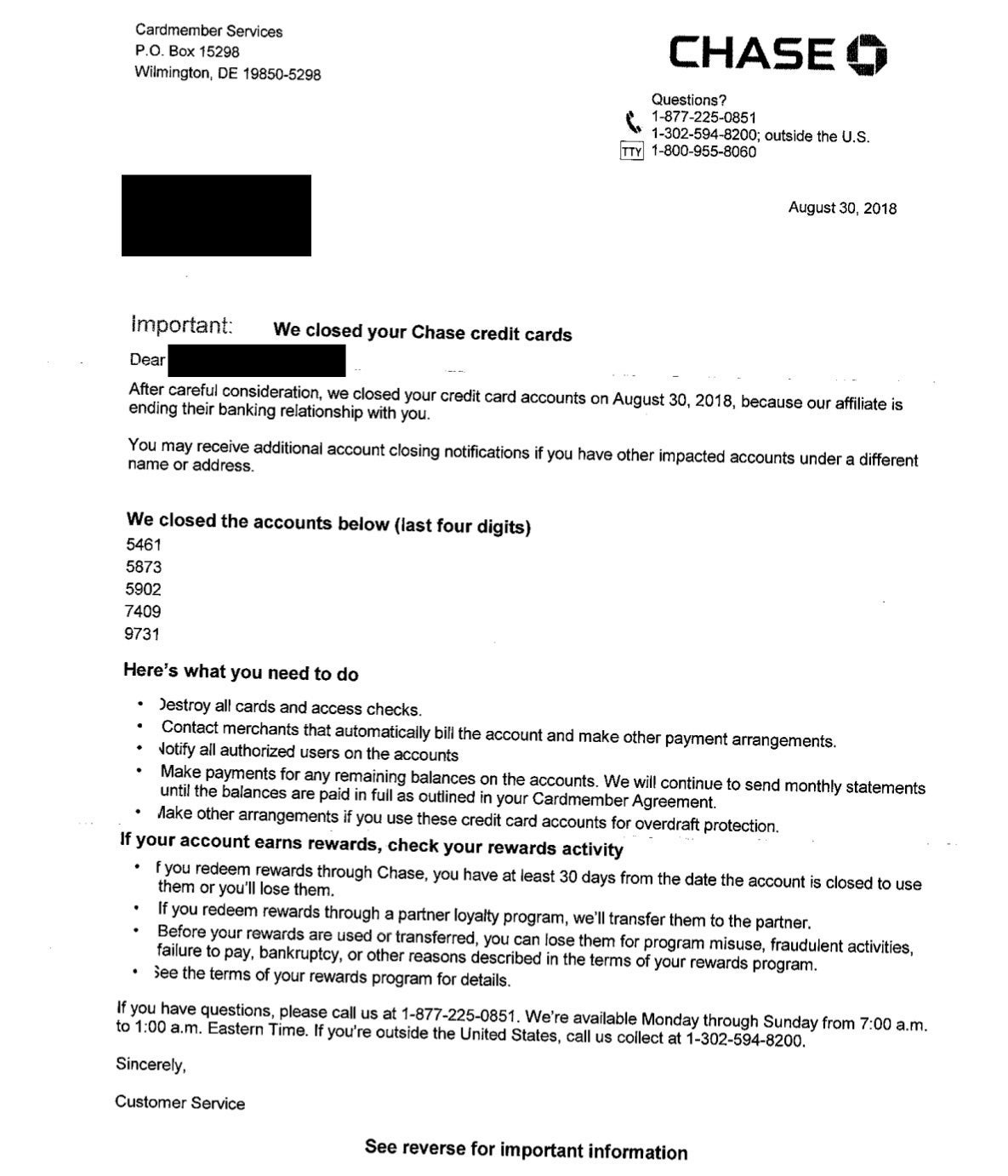

The notification of shut down begins one of a few ways: 1) Your card is declined at time of purchase and you call in, only to be told your accounts have been closed; 2) You log in to your online account to a notification that your accounts are closed or 3) You receive the following letter in the mail:

Cardholders' accounts are closed immediately, and they are given 30 days to use any Ultimate Rewards points left in their account. In some cases (but not always), personal cards and business cards are closed, while others reported that all of their Chase accounts, including non-credit card deposit accounts, were closed. There's been no official timeline of when an affected customer can/could come back to the bank, but many people report being successful two years after the initial account closures.

Risky behavior

After speaking to at least a dozen people who've lost their Chase accounts and reading dozens more stories across Reddit and other online communities, there is a clear (but not exact) list of common behaviors that will put your relationship with Chase at risk.

Too many applications

There isn't a precise limit on the number of Chase credit cards you can hold at a time. The 5/24 rule aside, I think it's safe to say that if you get to six, you should probably refrain from further applications with the issuer. Many customers told me that they had between nine and 10 personal cards (as well as business cards) and then were flagged when they applied for the Iberia Visa Signature Card or World of Hyatt Credit Card. However, some were flagged only holding five and applying for a sixth, so there is some variation here.

Recently, at the end of 2019 and into 2020, there seems to have been an increased scrutiny on too many applications. TPG Senior News Editor Clint Henderson, a Chase deposit account and credit card customer for years and also well below 5/24, applied for the Chase Ink Business Preferred Credit Card and two personal cards all within three days. He did not receive approval decisions on any of the cards during his application process. His personal deposit and credit card accounts were shut down the next week and he was left with very little information as to why. He completed no other risky behaviors listed here. At the time of his applications, he held a Chase Sapphire card (a card only available to Chase cardholders) and the IHG Rewards Premier Credit Card (more on his story below).

Too much credit extended

If you reported your annual household income as $80,000 and have $150,000 in credit lines from Chase, a scenario like this could raise a flag to Chase underwriters. We can't be sure how much is too much, and you could question why Chase would be willing to give this to you and then flag you for review. However, it's Chase's rules and algorithms, and they're allowed to determine if you've been given too much credit, even after the fact.

Spend that does not match your income

In a similar manner, if you're spending hundreds of thousands of dollars on your Chase cards, either for personal or business reasons, and your reported income is far below that, that could invite a review from the bank. This is an easy situation to avoid but one that evidently created unwanted attention for many former customers.

Cycling credit limits

If you're given a $7,000 credit limit, max it out and pay it off multiple times within a single statement period, you're cycling your card limit. This is a clear indicator of some of the above flags and another behavior commonly reported from those who have been shut down.

Payment variations

This is very hard to define, but I heard this multiple times when speaking with those that were shut down. If you're paying your bill at various times throughout the month from a variety of checking accounts or other bill pay methods, it could get your accounts flagged. Moving money through multiple accounts is a common money laundering method and thus a likely reason why Chase would question the activity.

Too much spend too quickly

You've got your brand new World of Hyatt card, and you know you're going to be a few elite-qualifying nights short of Hyatt Globalist status, so you quickly throw $15,000 or so on the card to earn six additional elite nights (two for every $5,000 you spend on the card). Without a pattern of large expenses to go on, Chase could question why a consumer would begin using such a large amount of credit so quickly. Once again, many customers with whom I spoke reported a large expense as the likely cause of the initial account review. It's easy to wonder why Chase would give you a large credit line and then flag you for using it, but again, it's the issuer's rules and algorithms that govern your account status.

Related reading: 11 ways to meet credit card bonus minimum spending requirements

The dark side of rewards

There's another side to this story which is often the most likely culprit in Chase severing ties with a cardholder. Loyalty points and miles are undeniably valuable assets. Anytime something of value is in circulation, there will be efforts to garner more of said currency. Sometimes this activity walks the line (or outright crosses the line) between following the rules and violating the terms and conditions of the applicable program.

In the reward space, this has led to two strategies:

- Manufactured spending, or MS for short (not to be confused with minimum spend)

- Brokering

Manufactured spending is putting expenses on a credit card, liquidating the purchase (sometimes with a minimal cost) and then paying off the card, leaving you with only rewards points. A simple, above-the-line example would be paying for a group dinner and then collecting cash from your friends; you essentially "manufactured" points or miles on your card without any money leaving your wallet. Now, this type of manufactured spending would never be cause for account closure (unless it falls into the above categories). However, there are other MS methods that are sketchier and thus could trigger an account review.

Brokering, on the other hand, is always against a program's terms and conditions. This term refers to the selling, buying and/or trading of rewards points and miles between accounts. Discussion and execution of these practices now largely reside in secret Facebook, Slack and WhatsApp groups due to the quick closure of such techniques if they're available to the public. It's also highly likely that publicly advertising such behavior would result in immediate shut down of your account (hence the secrecy).

Now, it's worth noting that there are ways to share points and miles between accounts that are fully allowed — like combining points from different Chase cards or converting cash-back earnings from Citi into fully-transferable ThankYou points. These are carefully spelled out in a program's terms and conditions. It's anything explicitly against these policies that puts your accounts in jeopardy.

Using credit cards and loyalty programs in this manner severely cuts into a bank's revenue and is thus highly frowned upon. The majority of Chase shutdown stories I read and the people with whom I spoke had used one or both of these techniques with their cards and/or points, many to a rather eyebrow-raising level. Hundreds of thousands of dollars spent on cash equivalents like gift cards is now virtually certain to garner Chase's attention at some point. This may not happen instantly, but it almost surely will over time.

There's hope If you've received initial notification

Returning back to TPG Senior News Editor Clint Henderson's story above, there is hope if you are shut down. Clint spoke with the Chase reconsideration line after receiving a letter in the mail that all of his accounts had been closed. Three days later he received word his Chase Sapphire and deposit accounts had been reopened, and he eventually ended up getting approved for the Ink Preferred card.

After speaking to a few other Chase customers who received the initial shutdown notification, they shared how they were also able to have their accounts reinstated after calling and appealing the decision. Legitimate large purchases — such as estimated tax payments — were sometimes the culprit of the account being flagged. However, for this to work, you need to have thorough, valid explanations for the purchasing patterns on your accounts, and documentation always helps. In addition, you must appeal within 30 days of the accounts being closed or you have no hope.

Unfortunately, in a few rare cases, Chase denied the appeal and the accounts remained closed, even with seemingly adequate explanations.

If you have an established relationship with your local Chase banker, that could be a good resource for you if you're shut down when you should not have been. Head into your local branch and see what the staff could do for you.

Bottom line

Many of you are probably left wondering if this will impact you and will (naturally) want to ask about your specific situation: Will I be okay moving forward? The short answer is that we don't know, and no one can give you a definite answer on what exactly will lead to Chase severing its relationship with you. However, if you're using the rewards cards you have in the manner intended and your spending patterns match your reported income, then there's little reason to worry.

The world of credit cards, points and miles is a long-term hobby. It's important to think of it as a marathon, not a sprint. I want to be able to utilize every loyalty program in existence 15-20 years from now. I understand first hand how tempting it can be to jump on limited-time offers, and it's not surprising that you want all of the points and miles now. I've had to tailor my own credit card spending patterns and behavior, as it has become clear that banks are on the lookout for anything seemingly suspicious. If you don't want to risk being shut down, keep the long-term goals in focus and be responsible with the way you handle your credit from all banks, not just Chase.