The first major bank now gives cardholders the option to choose your name -- here's why it matters

Citi is a TPG advertising partner

For nonbinary or transgender individuals, paying with your own credit card can be a fraught experience.

According to a 2015 report by the National Center for Transgender Equality, nearly one-third (32%) of people who showed an ID with a name or gender that did not match their gender presentation were harassed, denied service, assaulted or otherwise discriminated against.

There is progress on that front, however. Last year, Mastercard launched the "True Name" card feature, allowing nonbinary and transgender customers to insert their chosen name, rather than their legal birth name, on their credit card.

Now, Citi is teaming up with the "True Name" initiative to give cardholders the option to use preferred names on most U.S.-issued Citi cards.

Want more credit card news and travel advice? Sign up for our daily TPG newsletter.

This marks the first major bank to partner with Mastercard to make this feature widely available to most cardholders.

For nonbinary and transgender individuals, that means you can now easily change your first name on your credit card in three simple steps -- and you can even do it online here.

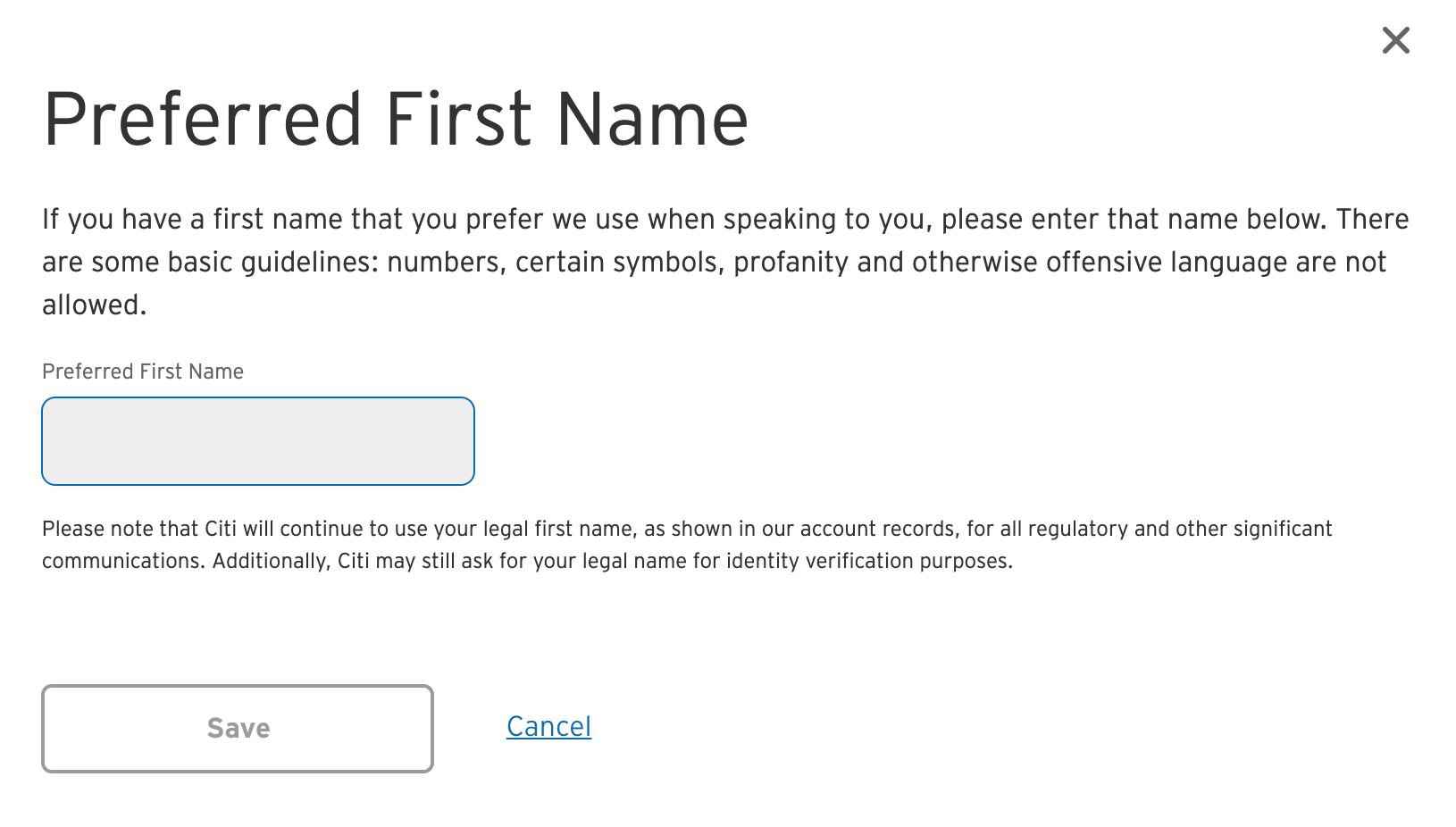

Here's how to change your name on a Citi card:

- Log in to your Citi-branded credit card account (or you can call the number on the back of your card).

- Under Profile, go to "Contact Information."

- Click "Use a Preferred First Name," enter the first name you go by and click save. Citi will attempt to use this name in most future communications, but for legal purposes may not be able to do so. Additionally, Citi may ask for your legal name for identity verification purposes.

Citi notes that a replacement card will arrive in about 4-7 business days once you finish the online (or phone) process.

"We're incredibly proud to launch the True Name feature, through our relationship with Mastercard, because we strongly believe that our customers should have the opportunity to be called by the name that represents who they really are," Citi's Chief Marketing Officer Carla Hassan said in a press release.

Related: The best LGBTQ+ friendly destinations

In the 2015 National Center for Transgender Equality study, more than two-thirds (68%) reported that none of their IDs had the name and gender they preferred. This may be a small, yet important step to changing that statistic.

Unfortunately, Citi bank accounts (including debit cards) are not yet eligible for preferred name changes. Additionally, you cannot use the name you go by on the following cards, according to Citi's website:

Small Business, Corporate, Professional, Shell Fuel Rewards® Mastercard®, L.L.Bean® Mastercard®, My Best Buy® Visa® Card, Shop Your Way Mastercard®, The Brooks Brothers Platinum Mastercard®, Meijer Mastercard® and Wayfair Mastercard®. Credit cards that display the American Express mark are also not eligible.

Although Citi may be the first major bank to allow a self-service option to print an entirely new name on your card, some banks have allowed name changes for years.

Chase, for instance, told TPG that they've allowed cardholders to use a preferred name for more than five years, as long as it's a "reasonable derivative" from a legal name.

That's progress for the approximately 1.4 million adults in the U.S. that identify as transgender, as well as those who identify as non-binary.

TPG featured card

at American Express's secure site

Terms & restrictions apply. See rates & fees.

| 4X | Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 4X | Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 5X | New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App. |

| 3X | Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines. |

| 2X | Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com. |

| 1X | Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases. |

Pros

- Valuable dining and food-related credits

- Flexible rewards with airline and hotel transfer partners

- Multiple travel and purchase protections

- No foreign transaction fees

- Access to Amex Offers for additional savings (enrollment required)

Cons

- Not as useful for those living outside the U.S.

- Some may have trouble using Uber and other dining credits

- You may be eligible for as high as 100,000 Membership Rewards® Points after you spend $8,000 in eligible purchases on your new Card in your first 6 months of Card Membership. Welcome offers vary and you may not be eligible for an offer. Apply to know if you’re approved and find out your exact welcome offer amount – all with no credit score impact. If you’re approved and choose to accept the Card, your score may be impacted.

- Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year.

- Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year.

- New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App.

- Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines.

- Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com.

- Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases.

- Pay It® lets you tap in the American Express® App to quickly pay for small purchase amounts throughout the month and still earn rewards the way you usually do. Plan It® gives you the option to split up big purchases into equal monthly payments with a fixed fee. You’ll know upfront exactly how much you’ll pay.

- Updated! $120 Dining Credit: Earn up to a total of $10 in statement credits monthly when you pay with the Gold Card at Grubhub (including Seamless), Buffalo Wild Wings, Five Guys, The Cheesecake Factory, and Wonder. This can be an annual savings of up to $120. Enrollment required.

- $100 Resy Credit: Get up to $100 in statement credits each calendar year at over 10,000 qualifying U.S. Resy restaurants after you pay for eligible purchases with the American Express® Gold Card. That’s up to $50 in statement credits semi-annually. Enrollment required.

- $84 Dunkin' Credit: Earn up to $7 in monthly statement credits after you pay with the American Express® Gold Card at U.S. Dunkin’ locations. Enrollment required.

- $120 Uber Cash on Gold: Enjoy up to $120 in Uber Cash annually with your Gold Card. Just add your Card to your Uber account and you'll get $10 in Uber Cash each month to use on orders and rides in the U.S. when you select an Amex Card for your transaction.

- New! As an American Express® Gold Card Member, you can enjoy complimentary Hertz Five Star® Status. Enjoy benefits like skipping the counter at select locations, adding an additional driver at no additional cost*, and vehicle upgrades**. Benefit enrollment and Hertz Gold+ registration are required. *Additional drivers must meet standard rental qualifications and must be a spouse or domestic partner to qualify as complimentary. Other additional drivers subject to fees. **Benefits are subject to availability and vary by location. Additional Hertz program Terms and Conditions including age restrictions apply.

- Take advantage of a $100 credit towards eligible charges* at over 1,300 upscale hotels worldwide when you book The Hotel Collection through AmexTravel.com or the Amex Travel App **. *Eligible charges vary by property. **The Hotel Collection requires a two-night minimum stay.

- Book your travel through the Amex Travel App with added peace of mind – backed by American Express® service and support. Only for American Express® Card Members.

- Whenever you need us, we're here. Our Member Services team will ensure you are taken care of. From lost Card replacement to statement questions, we are available to help 24/7.

- No Foreign Transaction Fees.

- Annual Fee is $325.

- Terms Apply.