Should I buy a used car instead of renting this summer?

Update: Some offers mentioned below are no longer available. View the current offers here.

The coronavirus pandemic has changed travel plans for millions of people around the world. Here in the U.S., many have taken their travel from the skies to the road, with AAA estimating that Americans will take 700 million road trips this summer

Despite only 45% of New Yorkers owning cars, the trend hasn't skipped America's largest city. NYC-based TPG staffers like myself, TPG Reporter Chris Dong and TPG Editorial Director Scott Mayerowitz have rented cars numerous times during the coronavirus outbreak, heading to other parts of the Northeast.

For me, renting cars has become a habit during the pandemic — sometimes for a day or sometimes for a week. That said, it's an expensive habit too. Despite using my alumni code and other methods for lowering rental prices, it's still started to add up over time, leading me to wonder: should I just buy a used car?

I've been wrestling with this dilemma for a couple of months and wanted to share my findings with you today. I'll compare the price of owning a car — and all of its associated costs — with renting at least twice a month. Let's get started!

For more TPG news delivered each morning to your inbox, sign up for our daily newsletter.

The cost of frequent car rentals

Renting a car may seem easy on paper, but as discussed in previous articles, this isn't always the case. The first order of business is finding the best deal on a rental car — you can do this by searching for rentals with Autoslash, using alumni and corporate codes and cross-checking prices with various rental companies.

But here's the thing: rental prices can change on a whim. Like airfare, the cost of a rental car fluctuates by date, time and the length of rental. This makes actually planning car rental prices difficult.

For this article, I've based my findings on booking a Friday to Sunday and Thursday to Sunday rental. The rentals will be picked up from two different neighborhood locations in New York, both with my rental car company of choice: Hertz.

Related: Tuesday Travel Tip: The top 3 easiest ways to save on rental cars

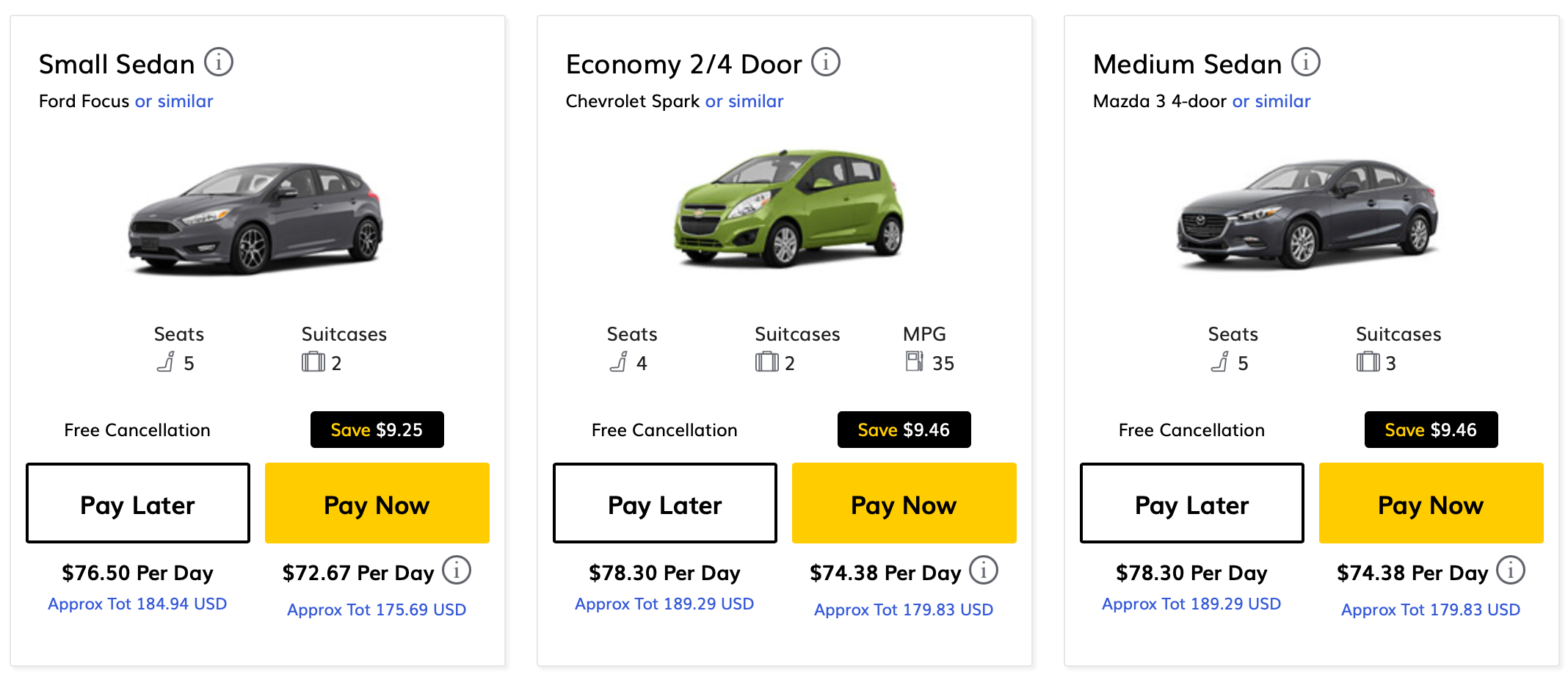

Pricing out a standard weekend rental

The shorter Friday to Sunday rental priced out at $175.69 when using the AAA Northeast corporate code. I have access to this code with my AAA membership, and it's supposed to provide up to a 20% discount on the car's base rate. This rental is set to be picked up at Hertz's 55th St Manhattan location and dropped off at LaGuardia airport.

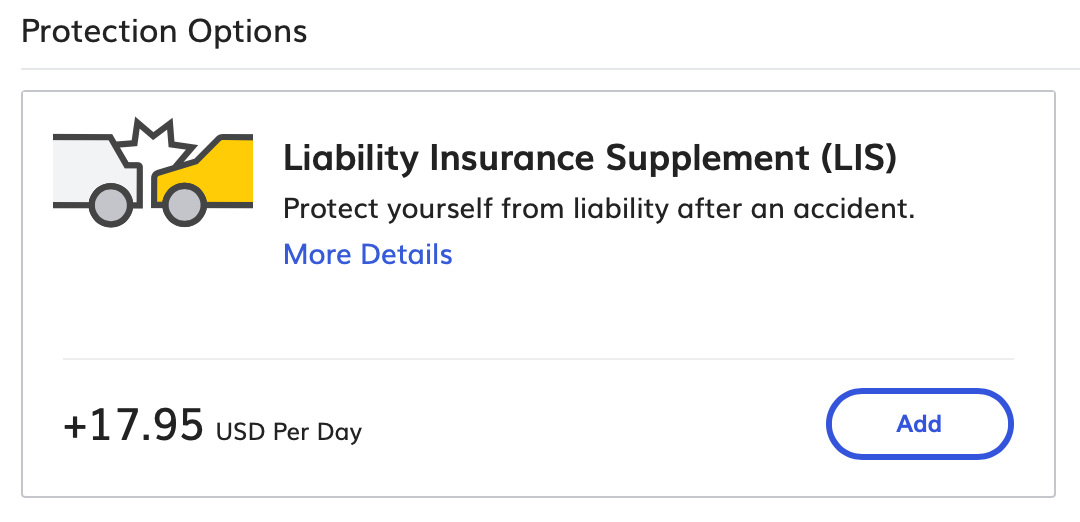

This is — however — before factoring in other associated costs. Since I don't currently own a car or have car insurance, I opt to pay for the Liability Insurance Supplement from Hertz. This costs an additional $17.95 per day. Thankfully, I don't have to pay for the $12 per day damage waiver — since I use my Chase Sapphire Preferred Card and this coverage is already included.

I generally do not prepay for gas since it's more expensive than refueling at a nearby gas station. I'm not going to include gas pricing in this article, as that would be a wash whether or not I own or rent a car.

There is one more cost to keep in mind, though: getting to and from the Hertz location. I live in Long Island City, Queens, so I can take the F train to the 55th Street Hertz location pretty easily. This is a cost of $2.75 per ride.

Getting home from the LaGuardia Hertz location is a bit more complicated. There's no direct way to get from the rental car area to my apartment, so I usually opt to pay for a Lyft home. Including my Lyft Pink discount, it costs about $18.56 to get home.

All in all, this means a two-day weekend car will cost a whopping $232.90 after insurance and transportation to and from the rental car lot. This is a pretty penny for a weekend away but would be less than airfare. It's also comparable to Amtrak tickets for two in the Northeast.

Related: The Critical Points: Here's how to avoid letting rental car companies take advantage of you

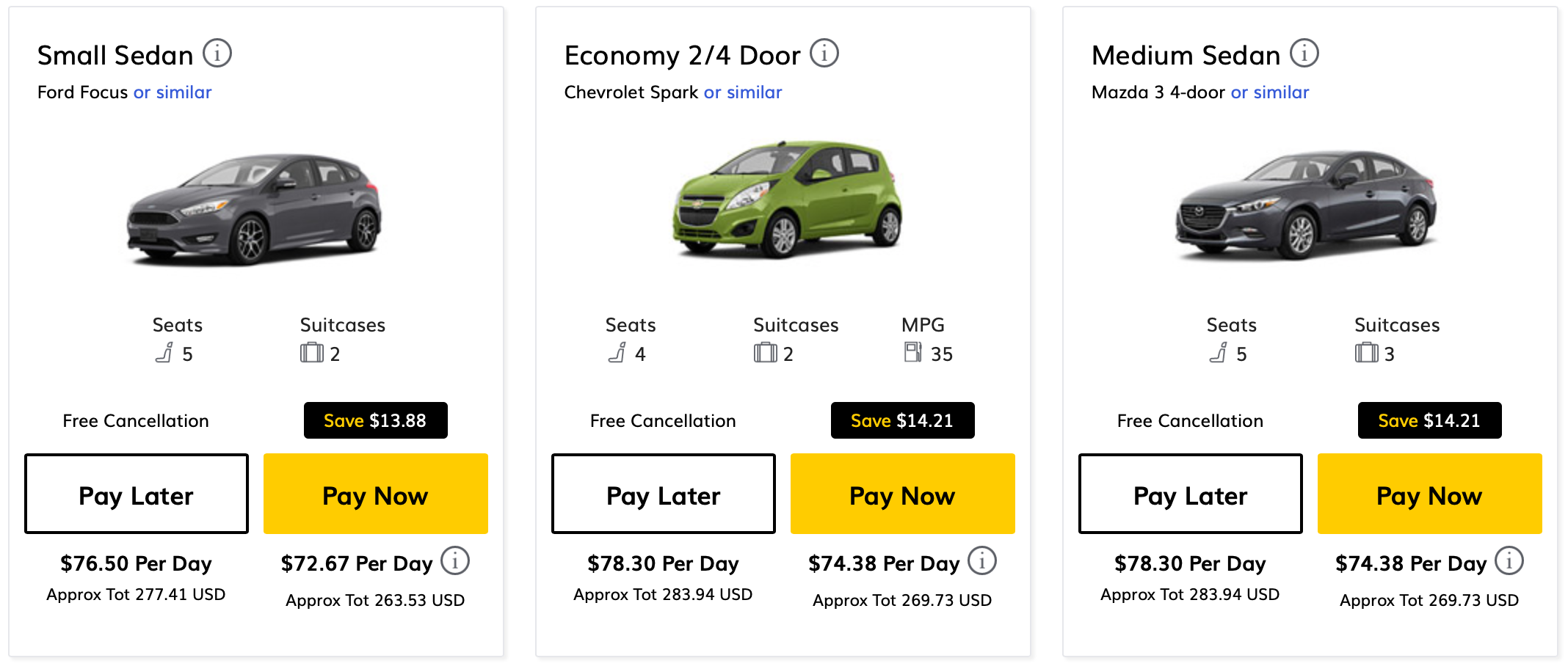

Pricing out a long weekend rental

For the long weekend rental — a Thursday to Sunday night — I will be pricing out a rental taking place roughly a month in advance. This will be to and from the same locations using the same AAA corporate code.

This time around, the rental costs $263.53 before insurance. The insurance charge is the same $17.95 for Liability Insurance Supplement. Since we're picking up and dropping off at the same location, I'll factor in the same $21.31 in transportation costs.

This gives us a long weekend total of $377.95. Again, this is a pretty penny, but it's not terrible for using a car for a weekend.

Related: Your points, miles and loyalty guide to Hertz car rentals

Recap of my findings

If I was to make two car rentals in a given month, I would pay $610.85 total for a weekend. Obviously, this isn't a fixed cost as I won't rent twice a month every month, but it's been the norm for me since May.

The monthly cost of owning a used car for leisure

Owning a car has never been a true necessity for me. I grew up in a suburb near Chicago but was able to bike or take public transportation to get around. The same goes for when I lived in Chicago and New York City.

In a world before coronavirus, I commuted to the TPG Manhattan office via the subway or worked remotely while traveling. Further, most of my everyday transportation was taken care of by the subway, my bike, or Lyft.

Beyond this, I used Amtrak for short trips while frequent travels back to Chicago and other domestic jumps were all on flights, usually booked with miles and points.

In today's world, however, a car looks more appealing than ever. I could use it for all of my weekend trips and drive my girlfriend to work when she goes to the office two times a week, saving her subway and rideshare expenses.

So, let's run the numbers and see if it makes sense to buy a car during the pandemic.

Related: The best credit cards for purchasing a car

The car in question

Over the past few weeks, I've researched buying a car extensively. I can't justify the cost of a new car as this vehicle will mostly be used during weekends. I still want to own a vehicle that is reliable, eco-friendly and has modern technology like a backup camera and Apple CarPlay.

In my dream world, this would be a Tesla or another high-range electric vehicle. That said, most of these vehicles are out of my $15,000 price range, so I decided to look for a plug-in hybrid.

For this article, let's assume that I purchased a used 2016 Ford C-Max Energi. This is the plug-in hybrid model that has approximately 19 miles of all-electric range, which would fit my needs well.

Further, the Kelly Blue Book fair value is $13,840 when equipped with the options I require. I'm going to assume that I'll able to purchase the car, used, for $13,000 from an individual.

Related: Can you buy a car with a credit card?

Breaking down the monthly cost of low-mileage ownership

There are four major parts to car ownership: car payment, insurance, maintenance and gas.

Let's look at how this is broken down for the 2016 Ford C-Max I discussed earlier. Since I don't own the car, I'm going to use publicly available data to figure these costs.

Before we dive in, I want to stress that this pricing is for low-mileage car ownership. If I do buy a used car, I plan on using it for weekend and day trips, occasional jaunts around town and (maybe) picking friends up from the airport. I do not plan on using it to commute regularly.

Figuring the car payment

While I plan on paying for the car in full, I do want to calculate the monthly expense over three years. For simplicity's sake, I'm not going to factor depreciation into this equation. Instead, I'll look at how much it will cost to pay myself back for the purchase over 36 months.

There's one more thing to figure here: used car tax. Here in New York City, we're charged a 8.75% tax (4% state and 4.75% city) on all used car purchases, which would be $1,137.75 on a $13,000 purchase price.

Doing this is pretty straightforward: if I paid $14,137.75 for the car (including taxes) and divided that cost over 36 months, we get $392.72 per month for the car. Again, this may be different when factoring in depreciation, but this is a good baseline.

Car insurance

Before we start this section, I want to make a quick disclosure: I'm a 24-year-old living in New York City with no driving history (beyond rentals). This may make my insurance quote higher than yours, so I'm going to use the New York City average insurance premium price for this article.

According to our friends at Bankrate, the average car insurance rate for those in New York City is $2,814. This works out to $234 per month, which is a high price to pay for simply insuring your vehicle.

That said, there are a lot of things we don't know about that number. For example, the true insurance rate for a used C-Max could be lower, especially for an older vehicle. But for this article, I think it makes sense to use that number.

Maintenance costs

Assuming I get the car without any major issues, Edmond's estimates that the first three years of used C-Max Energi ownership would have $3,562 in associated maintenance costs. This number is based on driving 15,000 miles per year, which is not anywhere near how much I expect to drive.

Since this is a weekend car, I expect to drive closer to 400 miles per month, mostly around the Northeast U.S. That said, I will likely take the car to my hometown of Elmhurst, Illinois twice a year instead of flying, which is 1,624 miles round-trip from Queens.

So in the end, I expect to drive closer to 8,000 miles per year. In a perfect world, this would mean that I will spend $1,857.59 on maintenance over three years, which equals out to $51.58 per month.

Gas cost

One of the reasons I picked the C-Max Energi for this article is its fuel efficiency. When you consider the car's plug-in battery with its gas mileage, the EPA estimates that the car gets 88 MPGe on combined city/highway driving. On the other hand, the car gets 38 MPG in combined gas mileage when you don't factor in the electric motor.

I mention this because I don't have an electric car charger at home. This means that I will have to rely on public chargers, which is fine by me: there are a bunch of these in New York City and I can charge at hotels during road trips.

So for this article, let's say I can top-up the electric battery five times in a given month, giving me roughly 100 miles of electric range total. This means I would drive 300 gas miles in a given month (assuming 400 monthly miles), which is just under 8 gallons of gas.

As of the time of writing this article, the average gas price in New York state is $2.20 per gallon. This gives me a monthly average gas price of just $17.60. Do note that this is subject to change, as gas prices fluctuate.

That said, I'm not going to factor this expense when choosing whether to buy or rent a car for leisure. You'll pay for gas regardless of whether you rent or buy, so it's a wash for the comparison.

Related: How I saved $1,000 on gas fill-ups in 1 year

Parking

Parking is a weird one — some New Yorkers opt to buy a covered parking spot while others rely on street parking.

I plan to fall into the latter camp here. One of the reasons I looked for an older car was so that I didn't have to worry about finding a garage. In my neighborhood, there's almost always available street parking near my place and I plan on getting comprehensive insurance that would cover my car against vandalism.

For this article, I'll factor $0 into the cost of parking the vehicle. The only time I foresee paying for parking is when I'm out-and-about. Even then, the cost would be the same for a rental or owned car.

Should I continue renting or buy a used car?

So far we've looked at the cost of renting a car twice a month and the cost of owning a used car for leisure in Queens, NY. Let's do a quick breakdown of the cost of both options.

Renting a car for five days a month could cost approximately $610.85. Obviously, this can change based on when and where you rent. However, it's a solid example for today's travel climate, where you may not want to fly.

| Rental | Cost |

|---|---|

Weekend rental | $232.90 |

Long weekend rental | $377.95 |

Total: | $610.85 |

On the other hand, I found that — excluding gas — the average monthly cost of owning a 2016 Ford C-Max Energi (or similar) would cost $678.30 when buying used. Here's a breakdown of all the expenses:

| Expense | Monthly cost |

|---|---|

Car payment | $392.72 |

Auto insurance | $234.00 |

Maintenance | $51.58 |

Total: | $678.30 |

Interestingly enough, these numbers are within $70 of each other, so the answer isn't quite as simple as I thought it would be. As you decide whether you should rent on the weekends or buy a car, here are a few things you'll want to keep in mind.

Will you have a place to park?

I discussed parking earlier in the article, noting that I plan to park on the street. That isn't an option for everyone though. For example if you live in Manhattan, your street parking options will be very limited.

With that in mind, you'll want to factor the cost of parking into your car purchase if you need to purchase a monthly parking spot. The New York City Parking Authority — an unofficial organization that tracks parking prices — estimates that the average monthly parking price is $430.

This is a valid concern anywhere in the world. Obviously, it's most convenient to have your own garage or a parking spot where you live, but apartment dwellers in big cities aren't usually afforded that luxury.

Will a car make your life easier?

One of the benefits of owning a car is that you have instant access to it any time you'd like. If you plan to drive more than twice a month — whether for short or long trips — this can be a huge draw. You can just hop in the car and head to your destination.

Even after the pandemic is over, a car can come in handy. It gives you the option to skip public transit when you want and drive yourself instead of taking a costly Uber or Lyft to a new part of town. This is especially true if you're worried about taking public transport while there's a global virus outbreak.

Will you really go on trips every month?

It's easy to say that you'll go on weekend road trips every month, but it's another to actually do it. You should only buy a car for leisure if you're sure that you have the desire to take these trips regularly.

I highly recommend starting by renting a car and taking a trip you've dreamed up before you buy a car, especially if you haven't driven in a while. After all, driving in cities can be stressful and not everyone enjoys driving for hours on end.

Consider a short-term lease

If you only need a car through the coronavirus pandemic, you may want to consider leasing a vehicle. You can do this through your local dealer or find a short-term leasing company that fits your needs — run the numbers and find what works for you.

Bottom line

In this article, I walked you through the price of renting a car twice a month and the cost of owning a car for leisure in New York City. Then, I compared the pricing and discussed some considerations you should make when deciding to rent or buy.

Obviously, there's no perfect answer to this question. It all boils down to whether or not you think you'll drive enough to justify the cost of owning a car. If you do, you'll save more by owning a moderately priced used car instead of renting twice per month.

On the other hand, you'll save money by renting if you don't plan on driving every month. Plus, rental car prices fluctuate, and there are plenty of ways to reduce the cost of your rentals if you know where to look.

I encourage you to do your own research before you make a decision. Think through all the points I made in this article and run your own numbers before you buy a used car. Make sure to adjust your numbers for your specific location, car requirements and how much you'll drive too.

Feature photo by Mikbiz/Shutterstock