Can you pay taxes with a credit card?

Editor's Note

Have you thought about paying your taxes with a credit card but weren't sure if that was a smart move?

On the one hand, charging your tax payment to a rewards credit card could mean earning cash back or points or miles toward travel. Plus, depending on the card, you might be able to make progress toward elite status with an airline or hotel loyalty program.

On the other hand, depending on how much tax you charge on a card, you could incur hefty service fees.

Taxes for the second quarter of 2026 (April 1 to May 31) are due by June 15. Your quarterly tax payments for the rest of the year look like this:

- Tax payments for June 1 to Aug. 31, 2026, are due by Sept. 15, 2026.

- Tax payments for Sept. 1 to Dec. 31, 2026, are due by Jan. 15, 2027.

Although you'll usually get dinged with service charges and other fees for using a credit card to pay your taxes, it could be worthwhile for a few reasons.

For instance, you might need to hit a minimum spending threshold to earn the welcome bonus on a new card. Or, you may want to score a spending-based perk, such as elite qualifying miles with an airline card or a free night certificate with a hotel card.

You may also have a card offering a 0% annual percentage rate on purchases for a set period, giving you some breathing room to pay off your tab.

Here's what you need to know about paying your taxes with a credit card.

Different ways to pay your taxes

If you owe taxes to the IRS, you can choose from several payment methods. Most people opt for one of the following:

- You can make a direct payment from your bank account, and the IRS won't charge any extra fees for this type of payment.

- You can wire the money from a bank account, although this option usually incurs a fee.

- You can mail a check or money order to the IRS without any fees, aside from postage and possibly the money order (depending on where you get it).

If you need more time to pay your taxes, you can file for an extension with the IRS or set up an installment agreement with a payment plan. However, you will likely pay penalties and interest on that payment plan.

You can also pay your taxes with a debit card. While the fee is minimal, you generally won't earn valuable travel rewards or cash back unless you have a debit product that earns rewards.

Fortunately, the IRS lets you pay your tax bill with a credit card through several third-party payment processors.

But be warned: These companies can — and usually do — tack on their own fees to your payments. You can see a list of these companies and their convenience fees on the IRS website.

Related: If I cash out my points and miles, do I have to claim them on my taxes?

The cost of paying taxes with a credit card

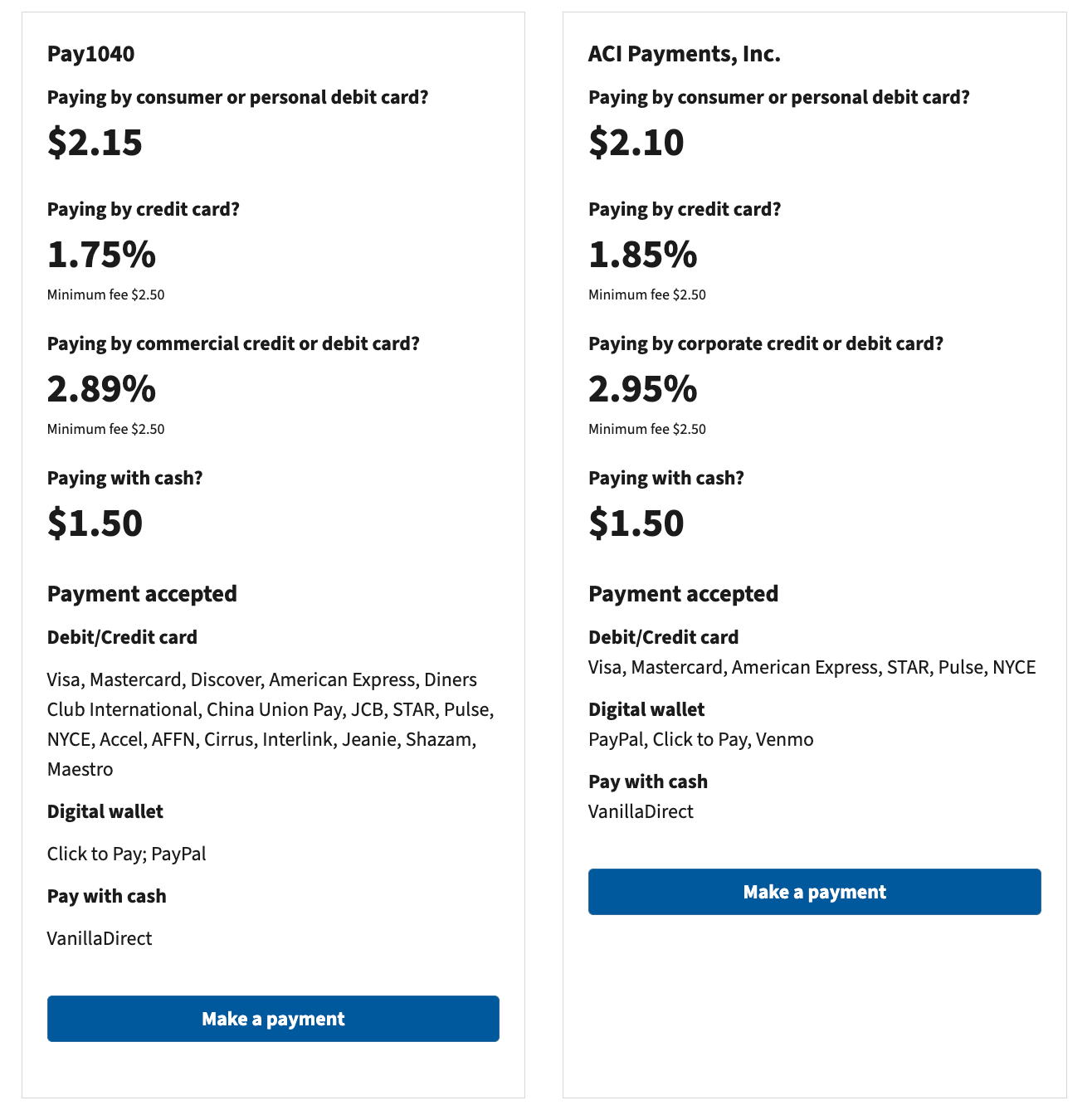

When you use a credit card to pay your taxes, the fee is calculated as a percentage of the amount paid. There are two payment processors the IRS uses for taking credit card payments: Pay1040 and ACI Payments, Inc.

Currently, those fees range from 1.75% to 2.95%. So, if you owe $10,000 and want to pay via a credit card, you'll be on the hook for an extra $175 to $295 in fees, depending on the service you use.

Despite Pay1040 showing a 1.75% fee on the irs.gov website, the 1.75% processing fee applies only to consumer Visa and Mastercard payments. If you use a business credit card or a personal or business Amex card, you will be charged 2.89%.

Just keep in mind that some TPG readers have reported that ACI Payments, Inc. does not accept business cards when they're used to pay personal taxes.

Related: Are your credit card rewards taxable? Here's why you're receiving 1099s

Reasons to pay your taxes with a credit card

Despite those surcharges, there are plenty of reasons why paying your taxes with a credit card can make sense.

First, doing so can help you earn valuable rewards and give you more time to pay off a high tax bill if you have a 0% APR offer on a new card or are targeted for a no-fee, pay-over-time plan.

However, if your purchase is subject to standard credit card interest rates, you should consider other options, as paying it off over time could be exceedingly expensive.

Here are some instances when it makes sense to use a credit card for your taxes.

It can help you earn a big welcome bonus

Many rewards cards extend welcome offers worth hundreds (and sometimes over $1,000) in cash back or tens of thousands of points or miles if you spend a certain amount on your new card within a specific time frame.

The single most significant reason to use a credit card when paying a sizable tax bill is that you can earn a high number of points or miles from one of these offers. That's because the value of the points or miles you earn can help offset the cost of fees for using your card for your taxes.

Some rewards cards have high minimum spending requirements for earning a bonus, so a tax payment might be just the thing to put you over that threshold.

Before you choose to pay your taxes with a credit card, make sure you can pay your card balance off in full. If you don't, you can get hit with interest charges and late fees that quickly wipe out the value of any rewards you might earn.

Accruing 20% to 28% interest on your credit card bill will easily negate a 3% to 4% return on spending through the points or miles you earn.

It can make it easier to meet a credit card spending threshold for extra benefits

Many credit cards offer benefits that trigger after you reach a particular spending threshold. These might be based on the calendar year or your cardmember anniversary, but in either case, making large tax payments could help you earn these rewards when that amount of spending might be out of range otherwise. For example:

- Spend $15,000 on eligible purchases with the Hilton Honors American Express Surpass® Card in a calendar year to earn a free night reward.

- Earn an additional free night award good at any Category 1-4 property after spending $15,000 on your World of Hyatt Credit Card (see rates and fees) in a calendar year. (You'll receive your first night award automatically after your card anniversary.)

With perks like this, putting your taxes on the right credit card can help you earn valuable extras like a boost toward elite status and free night awards.

It can get you elite status through spending

Several credit cards allow you to boost your elite status — or earn status outright — by spending on a credit card. These cards include:

- United℠ Business Card (see rates and fees): Earn 1 Premier qualifying point for every $20 in card spending (up to 4,000 PQPs in a calendar year). This can be applied to Premier 1K elite status.

- Citi / American Airlines credit cards: Earn 1 Loyalty Point per eligible dollar spent on these cards, boosting your elite status through credit card spending.

- Atmos™ Rewards Summit Visa Infinite® credit card: Earn 1 status point per $2 spent. You only need to spend $20,000 annually on this card to earn Alaska Airlines Atmos Rewards Silver status.

- World of Hyatt Business Credit Card (see rates and fees): Earn five tier qualifying night credits for each $10,000 spent on the card, which will help you attain elite status with World of Hyatt.

- World of Hyatt Credit Card: Receive five tier qualifying night credits each year you hold the card, plus earn two additional tier qualifying night credits for each $5,000 spent on the card.

It can help you maximize earnings when paying with multiple credit cards

If you have a large tax bill, you don't have to spend the entire amount on one credit card.

The IRS page explaining credit card payments says that you can only use debit or credit cards to make up to two payments per tax period (year, quarter or month, depending on the type of taxes you're paying), but that means you could use two different cards to make two different payments.

For example, say you have a $28,000 business tax payment due. You could apply for both The Business Platinum Card® from American Express and the Ink Business Preferred® Credit Card (see rates and fees).

You could put the first $20,000 on your Business Platinum. Since your purchase is more than $5,000, you could earn 2 points per dollar spent (on up to $2 million of these purchases per calendar year, then 1 point per dollar spent thereafter), which means you'd earn 40,000 points.

Then, you could charge the additional $8,000 balance due on the Ink Business Preferred and earn an additional 8,000 points (1 point per dollar spent on everyday purchases).

In this scenario, you'd end up with almost $1,000 in travel rewards, according to TPG's May 2026 valuations. (These figures don't take into account the points you'd earn on the fees you are charged for paying your taxes with these cards or any welcome offers you may earn through this spending.)

It can buy you some extra time to pay your taxes

One of TPG's 10 commandments for earning credit card rewards is never to pay interest charges. It's paramount that you never bite off more than you can chew.

When paying your taxes with a credit card, note when the first day of your new statement period begins on the card you want to use. This way, you may have up to 30 days until your statement closes and nearly 60 days until you must pay off your balance in full.

Some credit cards even offer 0% APR for an introductory period on new purchases, which can provide 12 to 18 months of interest-free payments on your tax bill. You must pay off the entire balance in full before the promotional period ends — otherwise, you risk incurring interest charges.

Finally, be sure to check your eligibility for a pay-over-time installment plan, as issuers sometimes provide introductory offers. This could be a great way to finance a large tax bill over time without incurring massive interest charges.

Related: A comparison of the top 'buy now, pay later' services — and what to watch out for

The downside of using a credit card to pay your taxes

Despite the benefits listed above, using a credit card to pay your taxes can be a reckless strategy, as the interest rate on most rewards credit cards can severely hurt your finances should you have to pay it.

If you don't have a no-fee, 0% APR option and cannot pay your statement balance in full after charging your taxes to a credit card, you should reconsider using a credit card to pay your taxes.

Instead, consult your tax professional about your options. The IRS offers payment plans with lower interest rates than most credit cards.

Plus, it's worth noting that all the cards included in the Bilt 2.0 suite — the Bilt Blue Card (see rates and fees), the Bilt Obsidian Card (see rates and fees) and the Bilt Palladium Card (see rates and fees) — do not earn points on tax payments.

Related: Earn points, miles and cash back while doing your taxes

Bottom line

With the second-quarter tax filing deadline approaching soon, paying your taxes with a credit card can be a lucrative way to earn points or miles as part of a large welcome offer.

Plus, having a 0% APR card may give you more time to pay off a higher tax balance without worrying about high credit card interest rates.

Either way, do the math to ensure the benefits you receive from paying your taxes with a credit card are worth the added cost.

Related: The best credit card welcome offers available this month

TPG featured card

at American Express's secure site

Terms & restrictions apply. See rates & fees.

| 4X | Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 4X | Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 5X | New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App. |

| 3X | Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines. |

| 2X | Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com. |

| 1X | Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases. |

Pros

- Valuable dining and food-related credits

- Flexible rewards with airline and hotel transfer partners

- Multiple travel and purchase protections

- No foreign transaction fees

- Access to Amex Offers for additional savings (enrollment required)

Cons

- Not as useful for those living outside the U.S.

- Some may have trouble using Uber and other dining credits

- You may be eligible for as high as 100,000 Membership Rewards® Points after you spend $8,000 in eligible purchases on your new Card in your first 6 months of Card Membership. Welcome offers vary and you may not be eligible for an offer. Apply to know if you’re approved and find out your exact welcome offer amount – all with no credit score impact. If you’re approved and choose to accept the Card, your score may be impacted.

- Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year.

- Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year.

- New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App.

- Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines.

- Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com.

- Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases.

- Pay It® lets you tap in the American Express® App to quickly pay for small purchase amounts throughout the month and still earn rewards the way you usually do. Plan It® gives you the option to split up big purchases into equal monthly payments with a fixed fee. You’ll know upfront exactly how much you’ll pay.

- Updated! $120 Dining Credit: Earn up to a total of $10 in statement credits monthly when you pay with the Gold Card at Grubhub (including Seamless), Buffalo Wild Wings, Five Guys, The Cheesecake Factory, and Wonder. This can be an annual savings of up to $120. Enrollment required.

- $100 Resy Credit: Get up to $100 in statement credits each calendar year at over 10,000 qualifying U.S. Resy restaurants after you pay for eligible purchases with the American Express® Gold Card. That’s up to $50 in statement credits semi-annually. Enrollment required.

- $84 Dunkin' Credit: Earn up to $7 in monthly statement credits after you pay with the American Express® Gold Card at U.S. Dunkin’ locations. Enrollment required.

- $120 Uber Cash on Gold: Enjoy up to $120 in Uber Cash annually with your Gold Card. Just add your Card to your Uber account and you'll get $10 in Uber Cash each month to use on orders and rides in the U.S. when you select an Amex Card for your transaction.

- New! As an American Express® Gold Card Member, you can enjoy complimentary Hertz Five Star® Status. Enjoy benefits like skipping the counter at select locations, adding an additional driver at no additional cost*, and vehicle upgrades**. Benefit enrollment and Hertz Gold+ registration are required. *Additional drivers must meet standard rental qualifications and must be a spouse or domestic partner to qualify as complimentary. Other additional drivers subject to fees. **Benefits are subject to availability and vary by location. Additional Hertz program Terms and Conditions including age restrictions apply.

- Take advantage of a $100 credit towards eligible charges* at over 1,300 upscale hotels worldwide when you book The Hotel Collection through AmexTravel.com or the Amex Travel App **. *Eligible charges vary by property. **The Hotel Collection requires a two-night minimum stay.

- Book your travel through the Amex Travel App with added peace of mind – backed by American Express® service and support. Only for American Express® Card Members.

- Whenever you need us, we're here. Our Member Services team will ensure you are taken care of. From lost Card replacement to statement questions, we are available to help 24/7.

- No Foreign Transaction Fees.

- Annual Fee is $325.

- Terms Apply.