The best way to pay your credit card bills

Editor's Note

Credit card debt is increasing nationwide. In fact, according to data from CNBC, U.S. credit card debt just hit an all-time high of $930 billion. Debt rates and figures vary by state, but one trend is common: Credit card debt is going up.

Credit card bills can be confusing to decipher for some cardholders. They can also be a source of concern and anxiety if you owe a large amount on your cards.

Whether you're simply trying to figure out how much to pay on your credit card bill or you're looking to pay down your credit card debt, this guide is here to help. Paying your credit card bill the best way can make a big difference. Here's what you should know about the best way to pay your credit card bills each month.

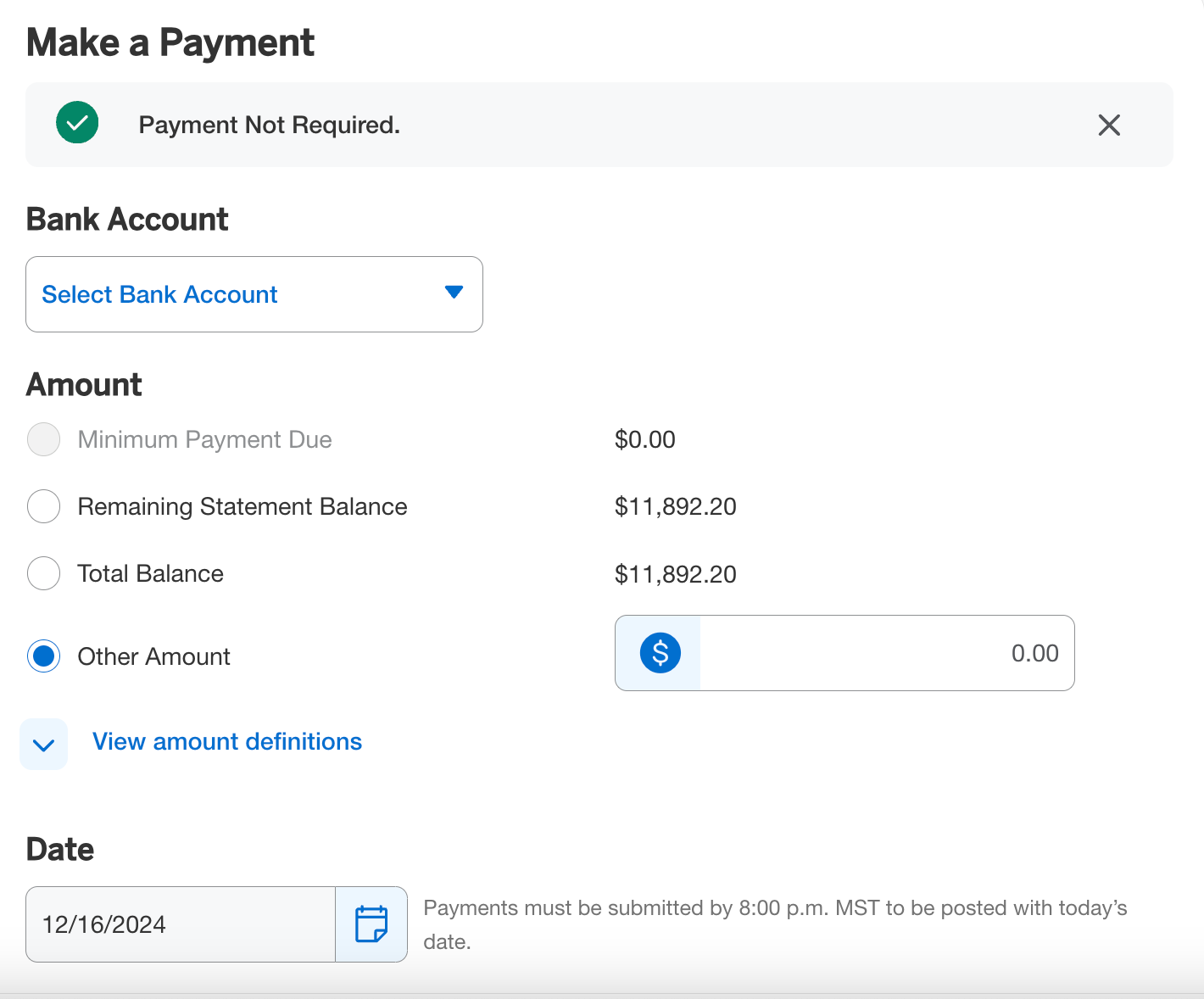

How to pay your credit card bill

Most credit card companies provide four options for paying your monthly credit card bill. Here's what you should know about each option.

Minimum payment due

Making the minimum payment due will allow your account to remain in good standing, so this is the least you should pay each billing cycle if at all possible. Paying the minimum amount due will allow you to avoid paying late fees or interest at a higher penalty rate — but you will still accrue interest on your unpaid balance.

Even if you pay the minimum balance on your account each billing cycle, your balance may still increase. This can happen when you accrue interest on your balance at a quicker rate than you're paying it off. This can happen if you pay just 10% off your bill but have an interest rate of 15%, for example. So, you'll want to pay more than the minimum amount due if possible.

Related: 5 mistakes to avoid when you get your first credit card

Statement balance

Your statement balance is the total of your charges during the last billing cycle. By paying the full statement balance each billing cycle, you'll avoid paying any interest.

You should aim to pay the statement balance on your account by your due date each billing cycle. If you don't have cash flow issues, it can be a good idea to set up autopay on all of your credit cards to pay the statement balance before your due date each month.

Pay the current balance

Your current balance consists of the total amount spent to date, including any unpaid balance from previous and current billing cycles. Put simply, your current balance is the most up-to-date snapshot of what you owe.

Paying the current balance (as opposed to the statement balance) is not necessary if you're looking to avoid interest and fees. Paying the statement balance is sufficient for that. However, paying the current balance can reduce your credit utilization ratio, which may be useful if you're looking to boost your credit score.

Custom amount

Most card issuers will also let you pay a custom amount. If you're short on money, paying a custom amount can be useful if you want to pay more than the minimum balance due but less than your statement balance.

Remember that if you pay less than the statement balance, you'll accrue interest, and if you pay less than the minimum balance due, you'll incur penalties and fees. It's best to pay the full statement balance if possible.

What is the best way to pay your credit card bill?

The best way to pay your credit card bill is to pay the statement balance by the due date each month. Doing so will allow you to avoid incurring any interest or fees.

In case you weren't aware, you do not automatically pay interest simply by having a credit card. You only pay interest if you do not pay the full bill each month by the due date. If you pay the statement balance by the due date, there's no interest to pay.

You could alternatively pay your current balance, which could be higher than your statement balance since it includes charges from the current billing cycle. Doing so will decrease your credit utilization ratio.

Related: How to earn points and miles with a low credit score

Are you supposed to pay your credit card bill in full?

Yes, you should pay your credit card bill in full, if at all possible. Doing so means you'll pay the statement balance on your credit card bill and avoid paying any interest or late fees.

Although you may have heard a rumor that carrying a small balance on your credit cards helps your credit score, this is incorrect. By carrying a balance, you'll pay interest on this balance but reap no benefits for doing so.

Methods for paying off credit card debt

If you have a lot of credit card debt, you probably already know the reasons why you need to pay it down. Paying off your credit card debt can save money, reduce stress and boost your credit score.

But paying off credit card debt doesn't come with a one-size-fits-all solution. Instead, there are numerous ways to tackle the problem, and you should choose the option that works best for you. Below are four smart debt elimination approaches to consider.

Snowball method

If you owe outstanding balances on multiple credit cards, the "snowball method" can be a great way to start chipping away at your credit card balances. With this approach, you pay down your cards in a particular order — starting with the smallest balances and working your way up.

First, make a list of all of your credit cards with balances. Order the cards from the largest balance at the top to the smallest at the bottom. It might look something like this:

- Capital One: $5,000 balance

- Chase: $3,000 balance

- Citi: $2,000 balance

- Retail store credit card: $500 balance

You'll need to continue making the minimum payment due on every card since this will keep your accounts in good standing and avoid late payment fees. On the card with the smallest balance, you'll pay as much money as you can each month toward wiping out the full debt. In the example above, you'd make minimum payments on your Capital One, Citi and Chase accounts each month before funneling all of your extra money toward paying off the retail store credit card.

Once you pay off the card with the lowest balance, move up the list to the next account. Repeat the process. At this point, you should have more money each month to put toward the second card on your list since you've eliminated the first debt. Follow this pattern until all of your credit cards have $0 balances.

Why use the snowball method?

Each time you eliminate a credit card balance, you'll begin saving money that was previously going toward interest. Each card that you pay off to $0 also is a personal victory that can have a positive impact on your credit score. After all, credit scoring models pay attention to the number of accounts on your credit report with balances, so reducing the number of accounts with balances can improve your credit score.

Related: From debt to over 20 credit cards: the story of my personal finance journey

Avalanche method

Although the snowball method is great for building momentum and knocking out small balances quickly, you may still be accruing interest at a high rate on some cards. So some people prefer the "avalanche method."

With this approach, you start with the highest-interest cards and work your way down to the lowest-interest cards.

To use the avalanche method, make a list of all of your credit cards with balances and interest rates. Your list should order the cards from the highest interest rate at the top down to the lowest interest rate at the bottom. It might look something like this:

- Chase: $3,000 balance with a 23.99% interest rate

- Capital One: $5,000 balance with a 21.49% interest rate

- Retail store credit card: $500 balance with a 15.49% interest rate

- Citi: $2,000 balance with a 13.99% interest rate

As with the snowball method, you'll need to continue making the minimum payment due on every card on your list. For the card with the highest interest rate — in this case, the Chase card — pay as much money as you can each month.

Once you pay off the card with the highest interest rate, move down the list to the next account (Capital One in the example above). Repeat the process. As before, you'll have more money each month to put toward the second card on your list since you've eliminated the first debt. Follow this pattern until all of your credit cards have $0 balances.

Why use the avalanche method?

The avalanche method eliminates the cards with the highest interest rates first. This means that you'll pay less interest using this method than when using the snowball method, assuming you put the same amount toward paying off your credit card balances. However, some experts recommend the snowball method instead of the avalanche method since the achievement you feel when paying off small debts quickly may encourage you to keep paying off remaining balances.

Related: Here are 3 reliable ways to pay off credit card debt

SHURKIN_SON/SHUTTERSTOCK

Balance transfer credit card

Some credit cards advertise 0% introductory APR balance transfer offers on new accounts. With a balance transfer offer, you may be able to move debt from existing credit cards and consolidate those balances on a single new account. You may even be able to find a no-annual-fee credit card with a 0% intro APR offer.

Be aware that most card issuers charge balance transfer fees; this is the immediate charge that's added to your account when you move a balance to the new card. For example, if a card issuer charges a 3% balance transfer fee, you'll pay $300 to transfer $10,000 worth of debt over to your new account. However, that $300 may be less than the interest you'd pay by keeping the balance on your current credit card.

Here are some current examples to give you an idea of how credit card balance transfer offers work:

- Citi Double Cash® Card (see rates and fees): 0% introductory APR for 18 months on balance transfers; after that, the variable APR will be 17.49% to 27.49% based on your creditworthiness. Balance transfers must be completed within four months of the account opening. There is an introductory balance transfer fee of 3% of each transfer (minimum $5) on balance transfers completed within the first four months of account opening. After that, your fee will be 5% of each transfer (minimum $5). If you transfer a balance, interest will be charged on your purchases unless you pay your entire balance (including balance transfers) by the due date each month.

- Citi Strata℠ Card (see rates and fees): 0% introductory APR on purchases and balance transfers for 15 months from the date of the first transfer; after that, the variable APR will be 18.49% to 28.49% based upon your creditworthiness. There is a balance transfer fee of $5 or 3% of the amount of the transfer, whichever is greater. Balance transfers need to be completed in the first four months of account opening. After that, your fee will be 5% of each transfer (minimum $5).

It's worth noting that some of your existing card issuers may also offer you low-rate balance transfer opportunities. You can log into your account to search for options or call the customer service number on the back of your credit card to see if any offers are available.

Why use a balance transfer credit card?

A 0% or low-rate balance transfer could help you save on interest as you work to pay off your credit card debt. That's because you may be paying less for the balance transfer fee than you would pay in interest by keeping your credit card debt as it is right now while making payments. But you should strive to pay off your account balance in full before the introductory interest rate expires and avoid adding more debt to your plate.

You don't want to transfer a balance away from an existing card just to charge up the balance again on your original account. On the flip side, opening another credit card could lead to just one more card on which you're carrying a balance if you don't focus on paying your credit card bills the best way each month.

In some cases, a new balance transfer card can improve your credit score. After all, using a balance transfer can reduce the number of accounts with balances and lower your overall credit utilization ratio. But a new balance transfer card will also result in a new hard credit inquiry and a new account on your credit report, which can decrease your credit score. So it's worth considering whether using a balance transfer is the right move for you.

Related reading: The best balance transfer credit cards

Personal loan

Another way to potentially speed up your debt pay-down process is by using a personal loan to consolidate your credit card balances. Similar to the balance transfer strategy above, this approach involves using a new account to pay off existing debt.

Unfortunately, you won't be able to secure a 0% APR on a personal loan like you often can with a balance transfer card. So, if you know that you can pay off your credit card debt quickly, a balance transfer offer may be a better option. If you believe it will take more time to dig yourself out of credit card debt, a personal loan might be a better long-term fit.

Why use a personal loan?

If you have good credit, you may be able to secure a lower interest rate on a personal loan than you're currently paying on credit cards. A personal loan with a lower APR could mean you'll pay less in interest fees.

Consolidating your credit card debt with a personal loan may also improve your credit score. First, if you pay off all of your revolving credit card debt with a personal loan, your credit utilization ratio should drop to 0% since a personal loan is an installment account that isn't factored into your credit utilization ratio.

Moving your credit card debt to a single installment loan could also help your credit in another way. When you pay off multiple cards, you'll reduce the number of accounts with balances on your credit reports — and the fewer accounts with balances on your credit, the better. Again, a personal loan will trigger a new hard credit inquiry and a new account on your reports, which could have a negative impact on your credit score. However, zeroing out your credit utilization ratio to 0% may overshadow this negative impact in many cases.

The best way to pay your credit cards is to bring their balances to zero each month, so consider whether achieving this goal is worth taking out a loan that you'll make payments on for the next several months or years.

Related reading: Can you pay your student loans with a credit card?

Bottom line

Credit card debt is notoriously expensive. The average rate on credit card accounts that assess interest is currently 23.37%, according to the Federal Reserve. If you pay 23.37% interest on $1,000 of credit card debt each month, that's around $19 per month — which adds up quickly when factoring in how many thousands of dollars you may owe.

However, if you use credit cards responsibly (focusing on the best way to pay, which is paying your entire statement balance each month), you can benefit. Well-managed credit cards can help you establish a better credit score, protect you from fraud and provide you the opportunity to earn valuable rewards. You can read more about how to pay credit card bills responsibly and use those rewards for travel in our beginner's guide.