Here's why I'm keeping my Chase Sapphire Reserve

Update: Some offers mentioned below are no longer available. View the current offers here.

Like every other Chase Sapphire Reserve cardholder, I've been crunching the numbers after Chase announced this week that the annual fee on the CSR will be going up $100. I've also had multiple family members and friends ask me if I plan to keep the card -- or whether they should keep theirs. Here are my thoughts.

For the latest credit card offers and deals, sign up for our free daily newsletter

As senior travel features reporter at TPG, my job involves less work-related travel than you'd think; the majority of my 90+ flights each year are booked on credit cards, like most travelers. To pay for my travels, I've been a CSR cardholder since May 2018.

I've been a Chase client since 2012 with almost a dozen products under my account, although I also hold cards with American Express, Barclays, Schwab and Capital One.

You've probably already read the thorough Q&A about the new CSR fees by TPG Editor-at-Large Zach Honig. But for quick reference, here are the major changes:

- The annual fee will increase from $450 to $550.

- The higher fee will apply to new applicants as of Sunday, Jan. 12, 2020 (so if you want to avoid the increase, apply quickly).

- The higher fee will apply for renewals as of April 1, 2020.

- Cardholders will be eligible for one free year of Lyft Pink (valued at $19.99 per month) and 10x points on Lyft rides.

- All new benefits will begin Sunday, Jan. 12, 2020.

Related reading: My elite travel status strategy for 2020

I'm keeping it. Here's why.

I'm still keeping this card, and many of you who fit my consumer profile should consider doing so as well. To put it in context:

- I'm a young professional without kids.

- I live in Austin, Texas, a mid-sized city where downtown parking is a nuisance on most days.

- I use ride-hailing apps between four and 10 times a month (no drinking and driving).

- I eat out way more often than I admit to my mom.

- I max out my CSR's $300 annual travel credit in a month or less.

- I live close enough to my local airport that hailing a Lyft ride both ways is cheaper than long-term parking.

I also have some fairly unique reasons for keeping the new $550 card:

- My CSR provides Priority Pass lounge memberships and excellent travel protection for my entire family (more on this later). As authorized users, they're also eligible for the bonus 10x on Lyft spend.

- Although I have an annual travel insurance plan that has been very good for me, I rely on my CSR for everyday trip protection, such as delays on routine work trips or weekend getaways.

- I earn additional Ultimate Rewards points through my Chase Freedom and Chase Ink cards, but use my CSR to book travel through the UR portal for the 1.5x boost. (Chase Freedom is no longer open to new applicants)

- I'm not a big fan of the electric scooters that pepper downtown Austin, but I hop on one once every month or two for a quick ride across town during rush hour; now, I will get three free rides a month with the card's Lyft Pink membership.

Lyft all day, every day

When it comes to ride-hailing apps, I definitely shop for the best rate. I was a diehard Lyft user a couple of years ago when I received a 50% discount on rides for many months, and still default to Lyft out of habit.

But since that promotion expired, my loyalty has wavered since I discovered that Uber almost always gives me slightly better rates as well as marginally better pickup times. Over the last six months, I primarily use Lyft in Austin only for airport rides, which earn 2x Delta SkyMiles per dollar through Lyft's partnership with Delta. But in New York City, prices have been 50/50 for me, so I usually stick with Lyft because of the triple-dip impact of each dollar I spend, especially on airport rides.

Starting Jan. 12, I'll be eligible for Lyft Pink, which normally costs $19.99/month and includes 15% off on all Lyft rides. I wouldn't sign up for it on my own, but I will since it's "free" for me as a cardholder this year.

Related: I saved $43 with Lyft Pink

I'm marginally excited about the other "elite" benefits I'll get for free under Lyft Pink, but I'm more thrilled about the 10x points I will earn for each dollar I spend with Lyft. My ride history shows that I spent $133.66 on personal Lyft rides between February and August of 2019, which would earn me 1,337 Ultimate Rewards points for similar activity in 2020.

As a result of this accelerated earning potential, I'm going to stop cost-comparing over pennies for the foreseeable future and only use Uber when the price difference is significant — say $5 or more.

And as I mentioned above, I truly hate those little scooters, but do find them useful for zipping across town during rush hour when it would take too long (or be too hot) to walk. Since I'm keeping my CSR, I will almost certainly use my free bike-or-scooter credits from Lyft each month. Maybe not all three, but even one free ride is a benefit.

To summarize all of the above, here's what I'll now earn per dollar when I use Lyft and pay with my CSR:

- 10x Chase Ultimate Rewards points per dollar spent on Lyft

- 15% off all Lyft rides for the next 12 months, thanks to complimentary Lyft Pink

- 2x Delta SkyMiles per dollar spent on Lyft rides to the airport, thanks to the partnership with Delta

- 1x Delta SkyMile per dollar on all non-airport Lyft rides

1.5x Ultimate Rewards portal redemptions

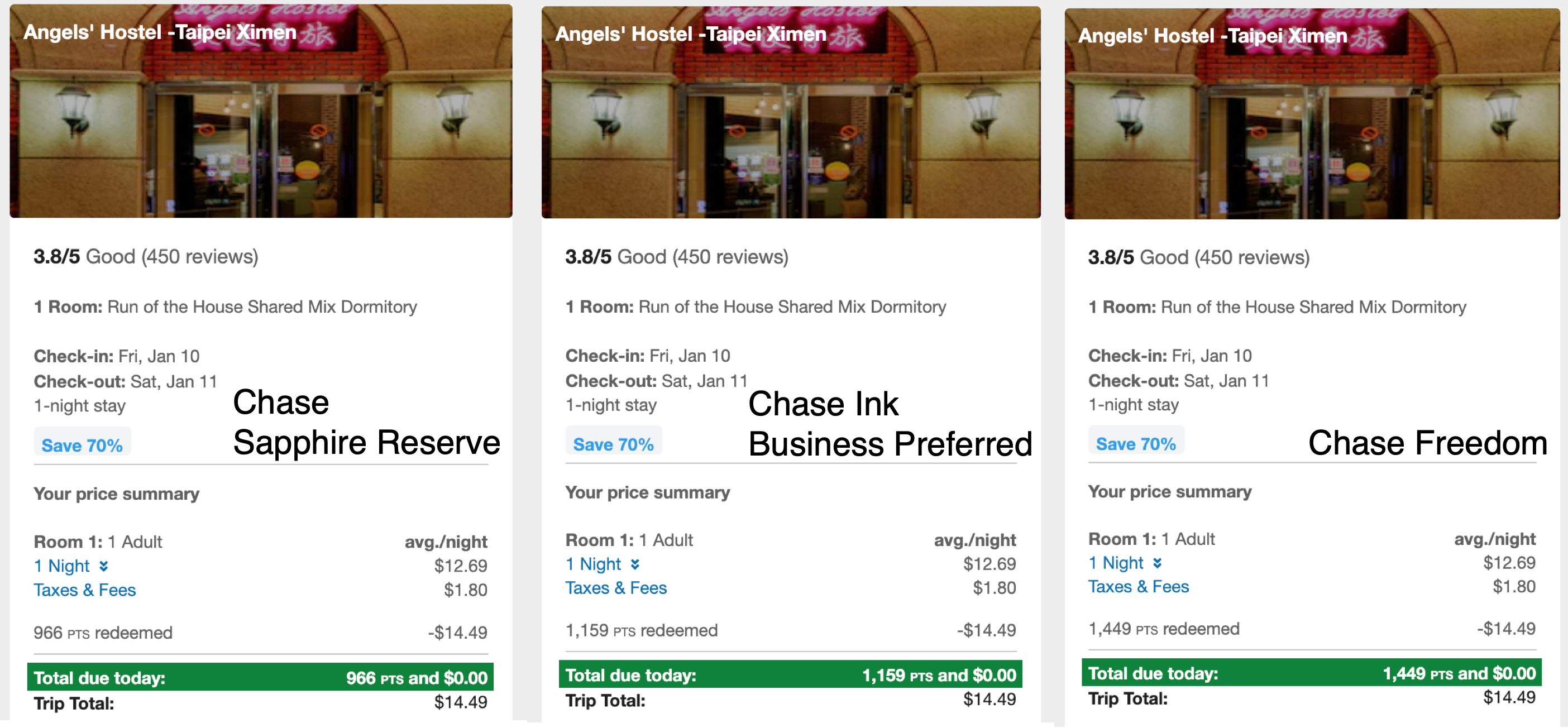

Here at TPG, we often talk about transferring credit card points to travel partners for outsized value. But every now and then, the best redemption does come directly through the Chase Ultimate Rewards portal itself.

In the example above, check out how much a $14.49/night hostel would cost me in points across my three Ultimate Rewards cards.

Related reading: Should I get the Chase Sapphire Preferred or Chase Sapphire Reserve credit card?

Priority Pass memberships for my family

One of the biggest perks on the CSR is the ability to add authorized users who then receive Priority Pass membership.

As mentioned above, I gift my family Priority Pass membership by adding them as authorized users on my Chase Sapphire Reserve. This is my annual Christmas present to everyone. My three adult brothers and my parents fly around the world regularly, and for $75 apiece each year, I can ensure we each have free food and a quiet place to rest in many airports worldwide. They're all even more budget-conscious than I am, so Priority Pass membership is a special treat they wouldn't otherwise splurge on for themselves.

I've had three authorized users on my account until this month, which means my annual CSR card fee has been $450 + $225 ($75 x 3) = $675. But I just applied for cards for the remaining two family members, so my next annual fee will be $550 + $375 ($75 x 5) = $925.

Despite the fees, I still think the updated Chase Sapphire Reserve will be worth it.

Here's how I figure it: Each Priority Pass usage is worth up to $28 and most of us fly through airports with accessible lounges. We average about 150-180 flights a year between the six of us. If we use Priority Pass even 50% of the time, that's $2,100 in food/drink/rest value alone ($28 x 75 flights, conservative estimate). And that's not even factoring all the other excellent travel protection benefits that come with the card, even for authorized users.

And here's my estimate of the priceless emotional value:

- My dad often flies between Asia and Europe on business, and my mom travels internationally several times a year. Both parents exclusively fly economy, so their only source of airport relaxation comes from Priority Pass. My mom in particular is an anxious flyer, and it's been nice to see her kick back a little more or even get a shower during a long layover in SFO.

- It's rare that I hit upon a gift my family continues to appreciate, year after year.

- One of my brothers is a serious AvGeek, and many lounges offer unique views of the runways that the average gate does not.

- My other brothers are just beginning their careers, so all of their travel is done on tight personal budgets. One is in a long-distance relationship and another is about to begin residency interviews after medical school, so free lounge food is my way of loving on them from afar.

Even The Platinum Card® from American Express doesn't offer Priority Pass perks at such a low price: Amex Platinum cardholders can add up to three authorized users for $175 total (see rates and fees), but I would have to spend $525 each year to cover all five of my family members (although they would have access to the Centurion Lounges and other offerings). Enrollment required for select benefits.

Here are my favorite CSR alternatives

Here's a trick I didn't learn until a couple of years ago: If you don't want a credit card any longer, don't cancel it unless you absolutely have to. Instead, look around for a downgrade option so you can keep the same card number and credit history but drop the higher annual fee.

If you're ready to break up with your Chase Sapphire Reserve, consider the Chase Sapphire Preferred Card ($95 annual fee) or a card from the Chase Freedom family ($0 annual fee), all of which are eligible downgrade options for CSR cardholders.

Chase Sapphire Preferred Card

If you love the CSR for its travel perks, you'll still be able to earn 2x points on travel and 3x on dining spending with the Chase Sapphire Preferred, which only carries a $95 annual fee and doesn't charge foreign transaction fees. You won't have Priority Pass lounge access any longer, but you'll still be eligible for primary rental car insurance, up to $500 per ticket in trip delay insurance and up to $10,000 in trip cancellation insurance. You'll even be eligible for up to $100 per day in delayed baggage expenses.

Furthermore, the Sapphire Preferred comes with purchase protection up to $500 per claim and $50,000 per account and extended warranty protection that provides an additional year of coverage on eligible purchases with a manufacturer's warranty of three years of less. You can read more about the CSP's shopping and travel benefits in the card's guide to benefits.

There are many other reasons why this workhorse of a card remains one of the best options on the market, and I would go back to it in a heartbeat if I ever had to let go of my CSR. But I'll let you read about the perks yourself here.

Chase Freedom Unlimited or Chase Freedom

These two no-annual-fee cards are pretty similar, and it took me a while to figure out the subtle differences. You earn 1.5% cash back (1.5x points) on pretty much every purchase using the Chase Freedom Unlimited. Chase Freedom earns you 1x on all purchases except on monthly rotating categories. TPG contributor Ethan Steinberg wrote a nice breakdown of both cards' benefits and differences. If you want to do away with annual fees altogether without losing your Ultimate Rewards points, one of these cards is perfect for you.

The information for the Chase Freedom has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.

Do you work for yourself? Switch to this card instead

I worked as a freelancer for many years before joining TPG full time. If you, like me, are more accustomed to 1099 forms than W-2s — or even if you just have a side hustle — let me introduce you to one of the most underrated credit cards of all time.

Chase Ink Business Preferred Credit Card

I love my CSR, but I really, really love my Chase Ink Business Preferred. Here's why: For a $95 annual fee, I earn the same 3x per dollar on travel expenses as I do on the Chase Sapphire Reserve, with very similar trip protection for delays, interruptions and cancellations. I also earn 3x points on shipping and advertising expenses, so this is great if you do a lot of Facebook ads or mail packages to clients often. (Note that the CIBP does not earn 3x on dining, however, unlike the CSR.) The 3x points is on up to $150,000 in combined category purchases each account anniversary year.

Even better, the CIBP comes with great cellphone insurance when you pay your monthly bill with this card; purchase protection; extended warranty; primary rental car insurance; and a lot of other great perks. There are lots of other benefits to this card, although you do have to meet more stringent requirements to qualify.

Related reading: Ink Business Preferred Credit Card review

Since this is a business credit card, you cannot switch the Chase Sapphire Reserve (which is a personal card) to the Ink Business Preferred. You will still have to decide what to do with the CSR, either by downgrading it or canceling it outright. But the Ink Business Preferred offers many of the elevated earning perks of the CSR, without the high annual fee (and unfortunately, also without Priority Pass access).

If you do decide to cancel

If you do decide to cancel your Chase card relationship altogether, make sure you time your downgrade or cancellation correctly. If you've already paid your annual fee for the year, don't cancel or downgrade your card until your renewal date, since you've already paid for the benefits.

Also, keep in mind that if the Chase Sapphire Reserve is the only Chase Ultimate Rewards card you hold, you will lose all of your points when you close your account. So if you've got some stray points lying around, make sure you transfer them to a travel partner before you call to cancel, because there's no reclaiming them once the account is shut down. (If you do have another Ultimate Rewards card, transfer your CSR points to that card first.)

Bottom line

I wrote about the Chase Sapphire Reserve changes because I found myself making the same points to friends over and over again. I'll follow up at the end of this year to let you know if the cost was worth the benefits. But for now, I'm confident in my decision to keep my card.

The Chase Sapphire Reserve won't make sense for every household now that the annual fee has gone up by $100. But the card still makes sense for me, and I hope my logic helps you decide if it still does for you as well.

For rates and fees of the Amex Platinum card, click here.