Why I charged $50,000 on my United card to get closer to Platinum elite status

This fall, I found myself facing a lot of very large expenses all within a short timeframe.

Think: Braces/pricey dental work, years of adjusted property taxes due as our house was finally appraised years after it was built and a good-sized deposit on a car. That doesn't even begin to scratch the surface, with all the normal end-of-year holiday expenses looming.

Thankfully, since we've been planning for most of these expenses for years, we already had the cash set aside.

So while this was a very painful series of financial events (RIP to my high-yield savings account balance), it was a moment that we were ready for and had an opportunity to maximize from the lens of points, miles and credit card benefits.

Call it a silver — or platinum — lining, if you will.

Here were some things I considered when deciding how to make the most of the expenses I was facing, and what I ultimately decided on, even though it was the least popular option in my circles.

Related: 10 ways to meet the spending requirements and earn the bonus on a new card

Option 1: Big, hard-to-meet credit card bonuses

Far and away, the most recommended course of action in my Instagram DMs when I informally polled what others would do in my situation was to earn big welcome bonuses, which would otherwise be tough to unlock due to their high spending requirements.

Even a $20,000-$30,000 minimum spending requirement would have been an "easy" hurdle with all these expenses hitting in short succession, so I'd have had my pick of the litter when it came to achieving the spending portion of almost any welcome bonus on the market.

For example, the The Business Platinum Card® from American Express has an outstanding offer right now where new cardmembers can earn 200,000 bonus points after spending $20,000 on purchases in the first three months of card membership.

And the Chase Sapphire Reserve for Business℠ (see rates and fees) has a bonus I'd love to unlock: 150,000 bonus points after spending $20,000 on purchases within the first three months from account opening.

Even though I do have an LLC and related business expenses, spending money on dental work, a car, and my home's property tax on a business card just didn't pass the sniff test for me. Everyone has their own reasons for things, but that just didn't pass my own personal muster as being a hive worth poking.

Option 2: Earn a variety of smaller welcome bonuses

Of course, there are several cards and welcome bonuses out there beyond just the small business ones.

The second most recommended course of action in my very informal poll was to just rack up a range of welcome bonuses, especially those with increased offers right now. I have many of the popular 'usual suspect' credit cards already, but there are some that are new or just haven't made it into my wallet yet that I could consider.

For example, I could earn 80,000 bonus Atmos Rewards points and a 25,000-point Global Companion Award after spending $4,000 on purchases within the first 90 days from account opening with the new Atmos™ Rewards Summit Visa Infinite® Credit Card card, which I may do at some point.

I could also get 75,000 bonus points after spending $6,000 in the first three months of account opening on the Citi Strata Elite℠ Card card (see rates and fees) — and it's very possible I will do that at some point in the not-too-distant future, too.

But there was one new card I did apply for and get approved for just as this expense onslaught began.

When I wasn't sure if it was going away near-term due to the Alaska-Hawaiian Airlines merger, I grabbed the Barclays-issued Hawaiian Airlines® World Elite Mastercard®. It awarded me 80,000 Hawaiian miles (now Atmos Rewards) with just $2,500 in spending in the first 90 days (offer no longer available). That took just a small percentage of my spending, but still netted a nice stash of Atmos Rewards.

The information for the Hawaiian Airlines World Elite Mastercard has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.

Related: 10 best ways to redeem Alaska Airlines Atmos Rewards points

Option 3: Go for higher-tier United elite status by using my existing United credit card

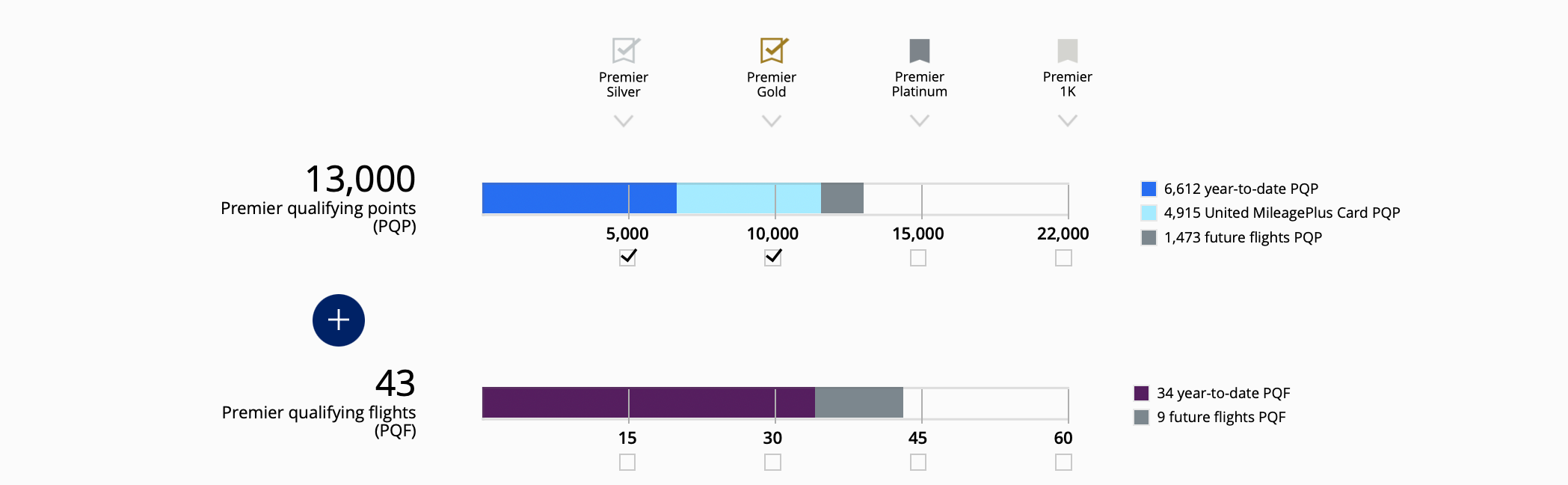

I hit United Premier Gold mid-tier status by September with three full months of 2025 left to go.

United's Gold status has benefits I value, but I do miss the perks of the higher status tiers I've had in the past, when they were easier to earn. Namely, the up to eight E+ seats at booking I can get at the Premier Platinum status level and the handful of United PlusPoints you get at that tier, which I'd like to try to use for a trip to Hawaii in the 'good seats' next year. That'll be a tough upgrade to clear with PlusPoints, but it's always fun to at least try.

The E+ extra legroom seats alone are a huge boon as a family traveler, as I only get two included at the Gold level I'm at, and they sell for $100-$300 per person on most of our United flights. For our family of four, that's just not happening on most trips. That means we usually sit in regular economy instead of enjoying those few more all-important inches.

Related: United Premier status: What it is and how to earn it

I'll also theoretically be higher on the upgrade list with United Premier Platinum than with United Premier Gold, but I don't place a ton of value in that part of the process, since not clearing as the 12th person on the list as opposed to the 20th person on the list doesn't make a ton of difference.

It's hard to earn the United PQPs you need to unlock status levels at scale with United credit cards, but if you are dealing with truly large charges, it is possible for them to add up.

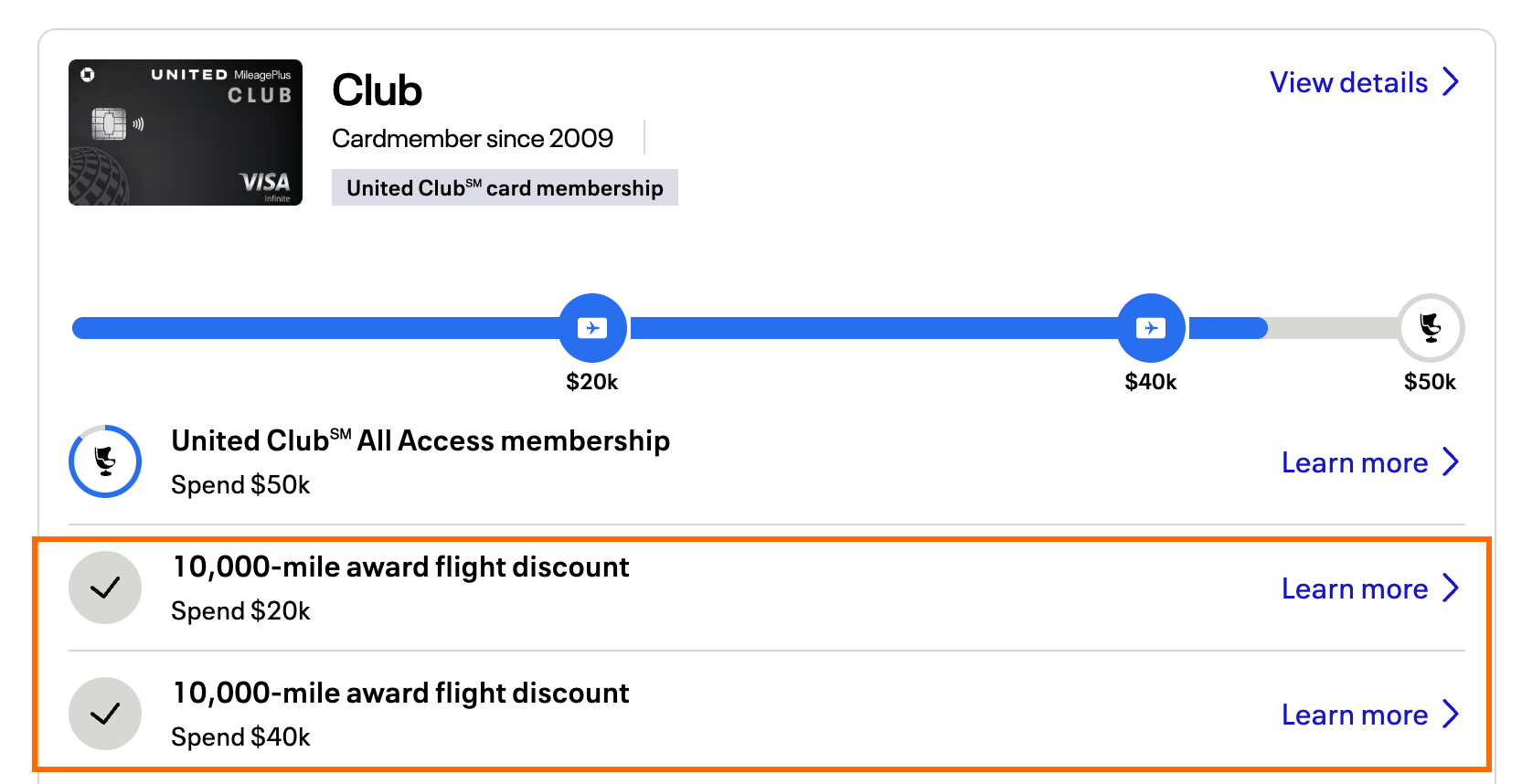

With my United Club℠ Card (see rates and fees), I can earn 1 PQP for every $15 charged to the card. That's in addition to the redeemable United miles you simultaneously earn.

So, if I charged $50,000 before the end of the year, I'd earn about 3,333 United PQPs towards this year's quest for United elite status from that spending.

As it turns out, when this all started, that was just about exactly the PQP gap I was facing between the Gold level I was naturally going to end at and the Platinum level I wanted to unlock.

But ... this plan gets a little better.

Once you hit $20,000 and $40,000 per calendar year on the United Club Card, which is something I'd never done before, you unlock 10,000-mile credits on award flights.

I had to book flights for 2026 travel, and they were priced at 13,500 United miles each way. I used each award to book two one-way flights, which reduced each flight to just 3,500 miles.

In addition, I was targeted for a spending offer that awarded a 10,000-mile bonus if I charged $9,000 between Sept. 1 and Dec. 31, 2025, which I was able to do.

If you add it all up, I earned:

- 50,000 United miles at 1 mile per dollar for all of my charges

- 30,000 bonus United miles between the flight discount and targeted bonus

- Enough PQPs for Platinum Premier status (assuming future travel and spend requirements are met)

That alone isn't a reason enough to do it this way, in my opinion (as there is about 2% in fees for some of the charges), but the redeemable miles are still helpful in the overall equation.

Related: United Club Card review: United Club lounge access and elite airline benefits

Bottom Line

Having large expenses pile up on you isn't always fun, but getting to earn some points and miles out of it makes it sting a little less.

Ultimately, my decision made the most sense for me and my family, despite being the least popular choice in my informal poll.

If all of this works as it should and my planned travel happens roughly as scheduled, I should be able to unlock United Platinum status (the second-highest published tier) that was otherwise out of reach, all by strategically using a card that was already in my wallet.

Related: 7 things to consider when choosing a credit card for large purchases

Updated 10/29/2025