Debunking Credit Card Myths: Can Authorized Users Affect Your Credit Score?

Update: Some offers mentioned below are no longer available. View the current offers here.

We spend a lot of time on travel rewards credit cards here at TPG. By leveraging top sign-up bonuses and strategically using these cards at different categories of merchants, you can unlock fantastic redemptions like first-class flights and luxurious hotel rooms. However, there are a number of misconceptions out there when it comes to credit cards, so today I'll continue our new series that debunks these myths and allows you to begin planning for your next vacation.

Previous entries included having too many cards, closing a card you don't use, not paying your balance in full and paying an annual fee. Today I'll continue looking at your credit score and debunk a common myth regarding the impact of authorized users.

Myth #14: Adding authorized users has no impact on your credit score.

There are many reasons why you'd want to add an authorized user to your credit cards. They can help you hit the spending thresholds required to earn a sign-up bonus or a calendar year bonus, and it also allows you to earn points and miles in your loyalty program accounts for someone else's purchases. It can also allow them to take advantage of a multitude of benefits on certain cards (like lounge access on The Platinum Card® from American Express or Admirals Club access on the Citi / AAdvantage Executive World Elite Mastercard). Most importantly, adding an authorized user is a critical first step in building up that individual's credit history.

Unfortunately, adding an authorized user is not risk-free. When you put an additional cardholder onto one of your credit card accounts, you're essentially telling the issuing bank that the individual is allowed to charge purchases to your account. It's true that this will help build up his/her credit history, but at the end of the day, it's your account and your credit score that's on the line.

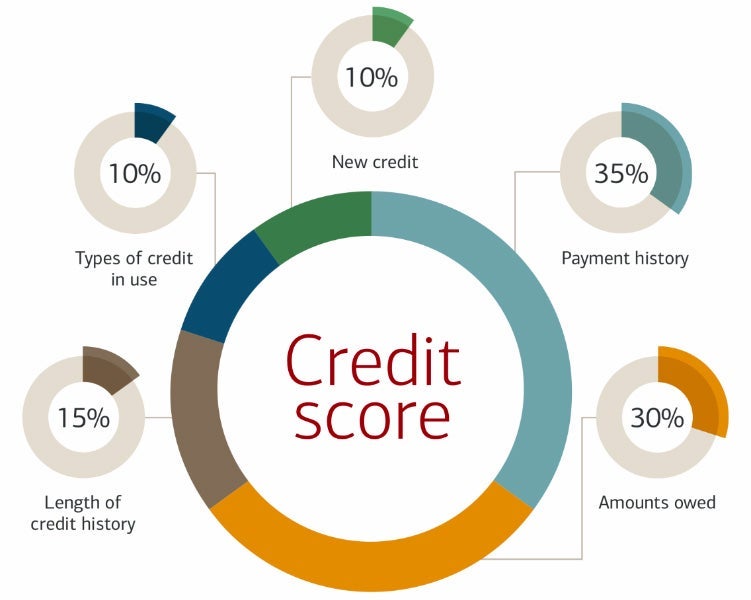

Let's quickly review the five main factors that contribute to your FICO score, the one most frequently used to determine creditworthiness:

- Payment history

- Amounts owed

- Length of credit history

- New credit

- Types of credit used

As we've mentioned before, these five factors are weighted based on how important they are to your score:

When you're considering adding an authorized user, it's the first two factors that come into play most significantly. Let's say that your authorized user goes on a spending spree and rings up charges that you can't pay off when your statement balance comes due. This will immediately impact your payment history, as you'll start to rack up interest charges and issuers will see that you aren't paying your balance in full.

It will also impact the amounts you owe on your cards, commonly referred to as your credit utilization rate. This is typically expressed as a percentage that indicates how much of your total available credit you are using, and if your authorized user brings your balance anywhere near your credit limit on that card, you (and your credit score) are in big trouble! Banks typically frown on utilization rates over 30%, so if you get above 50%, it can really impact your ability to gain approval for future lines of credit.

This is why it's critical to have a very frank conversation with your authorized user prior to giving them access to your line(s) of credit. American Express will even allow you to set individual limits on your additional cardholders, and you can easily track their spending through your online accounts. Just be aware that nothing can completely remove the liability you'll face when adding an authorized user to your credit card account.

For additional recommendations for managing your credit card account(s), be sure to check out my Ten Commandments for Travel Rewards Credit Cards.

Bottom Line

Adding authorized users to your travel rewards credit card account(s) can be a very positive thing, but it's not without risks. These additional cardholders are typically given full access to your credit limit and can quickly run up a balance for which you yourself are responsible. That being said, there are some important reasons why you would want to open up your credit card accounts to others, so be sure to factor those in when you're deciding whether or not to add authorized users the next time you open up a new card.

What are your thoughts on adding authorized users?