How to earn points and miles with a low credit score

Editor's note: This is a recurring post, regularly updated with new information and offers.

Travel rewards cards can be incredibly lucrative. Although the best sign-up bonuses or welcome offers often require high credit scores and unblemished borrowing histories, you can still get into the game even if your credit record isn't sparkling. Whether you're building credit for the first time or looking to rebuild, you have options.

Today, we will look at how your credit score is calculated and discuss strategies for earning points and miles while you build or repair your credit.

Credit score basics

Credit scores affect everything from interest rates on auto loans and your monthly mortgage payment to insurance rates and employee background checks when looking for a new job.

The Fair Isaac Corporation (FICO) produces the most well-known personal credit rating, and lenders commonly use this number as the first metric to analyze your risk as a borrower. As such, your credit score is the biggest factor in whether you're approved for a credit card.

What is a good credit score?

The FICO score ranges from 300 (bad) to 850 (excellent).* Generally speaking, having a higher score makes you a more attractive candidate for a loan. "Good" credit includes scores of 670 or above, and "poor" credit includes scores of around 600 and below. Top-tier or "excellent" credit starts around 740-750 and gives you a good chance of being approved for credit cards and other loans.

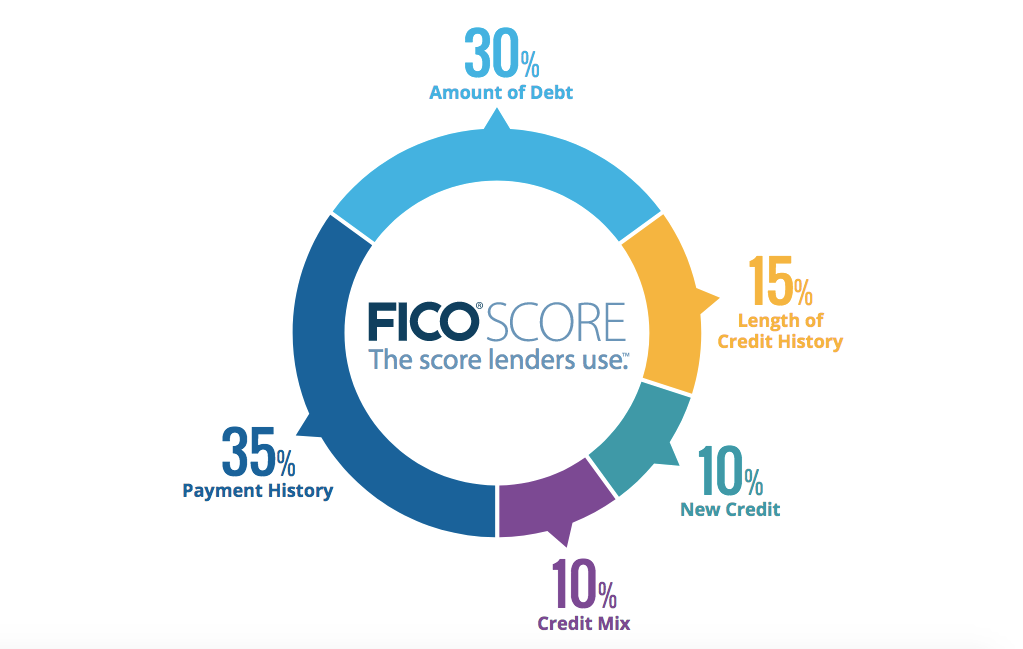

Your credit score is comprised of several different factors, as shown in this chart:

Related: What is a good credit score?

How can I check my credit score?

You can check your credit score for free in several places. If you already have a credit card, your issuer likely lets you check your credit score from within your account. Additionally, you can check your score through third-party sites, such as Credit Karma.

How can I improve my credit score?

The most critical credit score factors are late or missed payments and your credit utilization (the ratio of credit you're using to how much credit is available to you).

As such, the most important thing you can do to improve your credit score is to make your payments on time each month. Additionally, you can improve your score by opening an additional line of credit. It may seem counterintuitive, but increasing your available credit will decrease your credit utilization and increase your credit score.

Just remember that it will only help if you use it responsibly and pay it off each month. Late payments and accruing interest will do more harm than good.

Related: How a new credit card can increase your credit score

Rewards strategies for those with a low credit score

Consider cards in the same family

While you need an excellent credit score to be approved for most of the top travel rewards cards, plenty of rewards credit cards only require a good or fair credit score.

For example, you'll need an excellent credit score (740 and above) to be approved for the premium Chase Sapphire Reserve® (see rates and fees), but the Chase Sapphire Preferred® Card (see rates and fees) and Chase Freedom Unlimited® (see rates and fees) only require a good credit score (670 and above). And if you're just starting out and have limited credit, the Chase Freedom Rise can be a good option.

Similarly, Capital One offers products in the same card family geared toward different credit levels. For instance, TPG recommends at least a good, if not excellent credit score to be eligible for the Capital One Quicksilver Cash Rewards Credit Card, but they also offer the Capital One Quicksilver Cash Rewards for Good Credit and Capital One QuicksilverOne Cash Rewards Credit Card, which caters to those with fair credit (580 and above).

The information for the Freedom Rise has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.

Get a secured credit card

A secured credit card can be a great option if you're building or repairing your credit. With a secured credit card, you'll put down a deposit when you open the account, and that deposit usually serves as your credit limit at the beginning.

Not all secured credit cards earn rewards, but getting one that does is a way to earn rewards while working to improve your credit score. The Capital One Quicksilver Secured Cash Rewards Credit Card, for example, is the secured card in the Quicksilver family and earns 1.5% cash back on all purchases. Another option is the Discover it Secured, which earns 2% cash back on the first $1,000 spent at gas stations and restaurants each quarter.

The information for the Discover it Secured card has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.

Related: What is a secured credit card?

Get a rewards debit card

While most debit cards don't earn rewards, there are a few that do.

With the American Express Rewards Checking program, for instance, you'll earn 1 Membership Rewards point per $2 spent on your debit card. This isn't as high of an earning rate as you'll get with a credit card that earns American Express Membership Rewards points, but it's a great way to start earning if you aren't eligible for one of our favorite American Express credit cards.

Use shopping portals

We recommend that everyone use a shopping portal to earn bonus rewards when shopping online — but they're especially valuable for those who aren't eligible for a top travel rewards credit card.

You can shop through our favorite portal, Rakuten, and earn rewards in the form of cash back or American Express Membership Rewards points. Plus, many rewards programs offer their own shopping portals, so you can choose one that earns your favorite type of rewards.

Related: How one Chrome plug-in can earn you rewards

Bottom line

The travel rewards game isn't just for those with high credit scores. You can earn rewards while building or repairing your credit by getting a credit card or rewards debit card that you are eligible for, as well as taking advantage of shopping portals when you're shopping online.

Regardless of the route you choose, ensure you're boosting your credit score by paying off all your bills in full and on time each month. By practicing good credit habits, you'll be ready to get some top travel rewards cards in no time. And when you get there, you can use your points from a new welcome bonus to celebrate with a trip you've booked courtesy of the rewards you've earned.

Related reading:

- The beginner's guide to credit cards

- The beginner's guide to points and miles

- Does applying for a new credit card hurt your credit?

- How to improve your credit score

*The Points Guy credit ranges are derived from FICO® Score 8, which is one of many different types of credit scores. If you apply for a credit card, the lender may use a different credit score when considering your application for credit.