4 types of travelers who should convert Southwest funds to points

Travel disruptions, cancellations and reschedules have become a commonplace occurrence, especially in 2020. Southwest's solution to travel changes often comes in the form of travel funds, whether as flight credit from a cash trip you canceled, a paper certificate from a flight delay or leftover value from a fare difference after you changed a flight.

Last week, Southwest announced that travelers can now convert some travel funds to Rapid Rewards points. This is exciting news for a lot of people, even if it isn't always the best possible value.

For more TPG news and travel tips delivered each morning to your inbox, sign up for our free daily newsletter.

While my colleague Zach took a numbers-based approach to the conversion news, I have a different take: Whether or not you convert your Southwest funds should depend on your personal travel habits — not just on the best cash value.

If you consider yourself one of the traveler types below, here's why and when converting your Southwest credit into Rapid Rewards points might make sense for your lifestyle.

Related: Southwest current credit card offers

If you're an infrequent Southwest traveler

If you don't fly Southwest often, you might not want to bother tracking your airline credit. Perhaps you usually fly American but booked Southwest for a destination wedding that got canceled. Or you primarily fly overseas to destinations that Southwest doesn't serve. Whatever your reason, keeping track of airline details can be pesky, whether it's paper vouchers or email itineraries with travel details and confirmation numbers you may no longer remember. Not to mention the annoyance of planning how to use your funds before the expiration date hits.

If this applies to you, go ahead and convert your credit to points. That way, you'll have a stash of points to use for the next time you unexpectedly need to fly Southwest for any reason. I consider this move to be the equivalent of taking my coin jar to the grocery store and converting it into a Starbucks gift card at the Coinstar machine. A handful of change doesn't count for much on its own, but it does add up, little by little. Before I know it, I've got a free treat courtesy of a 15-second action.

Related: These are the best Southwest credit cards for 2020

If you value simplicity over savings

I have a confession: I work for TPG, yet I haven't been able to convince certain family members to track their loyalty program account numbers, let alone keep track of travel credit (no, I don't want to talk about it.) Those family members consider travel credit to be "bonus money," and don't want to "sweat the small stuff."

If this paragraph above applies to you, log into Southwest right now and convert your all of credit into Rapid Rewards points. In your situation, forget about the cash-to-points conversion value of your travel funds: The value of your travel credit is going to be a big, fat goose egg if you forget to use it before it expires.

If you often book travel for your whole family

If you are the main revenue traveler of the family, you might also want to convert your travel credit to Rapid Rewards points. Let's say you travel for work and pay cash for your flights but want to use the points you earn to book vacations for the whole family.

You can book flights for yourself with your travel credit, and those flights will toward A-List and Companion Pass requirements. But you can't book flights for someone else using your travel credit; that's linked to you and your name only. If you don't like that limitation, you're best off converting your travel credit into points.

If your travel credit doesn't hold a lot of cash value

This conversion scenario is less about your travel profile as it is about your situation.

If you booked a $200 flight, then switched to a different flight later on that cost $193, you now have a $7 travel fund from Southwest. This is great and one of the many reasons that diehard loyalists love Southwest: No hidden fees, and you can even get some money back on travel that's already booked. (Who does that?!)

Unfortunately, there is one catch: You can only use two forms of travel credit on any flight booking; if your funds aren't sufficient to cover the cost of your ticket, the third and final form of payment on your itinerary has to be a credit or debit card that covers the remainder of the balance.

In most cases, that $7 credit from your flight refund will cost you one of those two precious travel credit "slots" without skimming off a lot of the actual ticket price. In these situations, I'd suggest you convert your credit to points.

Related: The best Southwest Airlines credit cards for family travelers

Here's what I did with my own Southwest credit

So what did I do with my own travel credit? I was sitting on a fat stack of travel funds worth more than $600 before the pandemic hit the U.S. I do travel pretty frequently and track my flight credit expiration dates like a hawk. But I had a handful of funds that just weren't worth very much individually.

Like many of my colleagues, I often book separate one-way flights even for round-trip travel for several reasons. One of them is ease of itinerary management. Southwest allows you to change flights for any reason, including repricing your ticket if you find the same route for cheaper later on. I personally find it far easier to make changes on a single flight than it is for my whole reservation.

The downside is that when I get travel credit for repriced flights, all of my small savings end up broken out into relatively small travel funds, such as the $5.60 and $37 funds above. You'll see from the screenshot that none of my travel funds are worth more than a cheap one-way flight on their own.

Related: Everything you need to know about getting the best seats on Southwest Airlines

In the list above, I chose to convert my $5.60 travel funds to 437 Rapid Rewards points. It isn't worth much either way — just a drop in the bucket either in cash value or as points — so I'd prefer to keep that value as part of my points stash rather than forgetting about it or losing a valuable travel fund "slot" that I could use for a higher-value voucher.

For my particular situation, that was the only voucher that made sense to convert to points. I have a domestic trip coming up in the next few months, which I broke up into two bookings: One for just over $100, which I paid for using my Feb. 4, 2021 voucher, and the other for about $80, which used up my two lowest-value travel funds of $37 and $40.27, respectively. I paid the final few dollars using my Southwest Rapid Rewards Premier Credit Card, although I realized just a second too late that I actually should've used my Chase Sapphire Reserve in order to qualify for the excellent trip protection benefits.

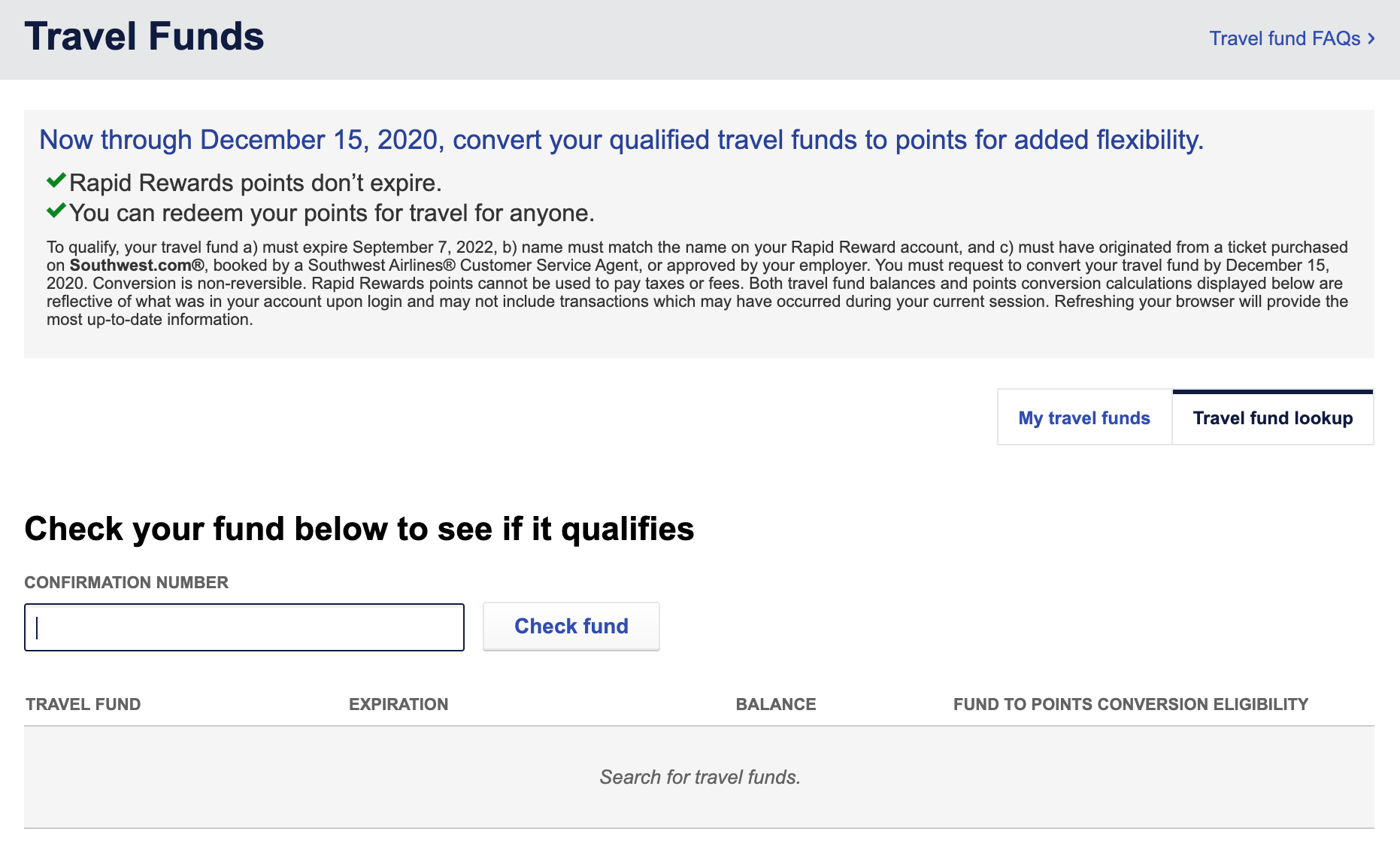

How can you check your own travel fund balance?

It's easy to manage your travel funds, thanks to a new tracker Southwest implemented on its website in 2019. Just log in to your account — you'll see a white banner with a green label that says "New: Convert qualified travel funds to points." To the right, you'll see a button that says "View travel funds." Click on that and you'll be able to see all of your travel funds in list form, the same way I did.

You may have a few funds from past travel that may not have made it into the Southwest system, especially if you have changed or canceled trips that took place before December 2019. If that's the case, I suggest taking a few minutes to dig through your email or travel archives to look up past confirmation numbers, just in case. You can access this tool on the "Travel Funds" page and plug in your previous confirmation number to check for any extra funds.

Bottom line

Converting cash to points isn't always the right move, particularly if you're gunning for elite status or want to keep business and personal travel separate. But if you fall into one of the three traveler categories mentioned above, you'll definitely want to consider swapping your travel funds for some Rapid Rewards points.

TPG featured card

at American Express's secure site

Terms & restrictions apply. See rates & fees.

| 4X | Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 4X | Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 5X | New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App. |

| 3X | Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines. |

| 2X | Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com. |

| 1X | Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases. |

Pros

- Valuable dining and food-related credits

- Flexible rewards with airline and hotel transfer partners

- Multiple travel and purchase protections

- No foreign transaction fees

- Access to Amex Offers for additional savings (enrollment required)

Cons

- Not as useful for those living outside the U.S.

- Some may have trouble using Uber and other dining credits

- You may be eligible for as high as 100,000 Membership Rewards® Points after you spend $8,000 in eligible purchases on your new Card in your first 6 months of Card Membership. Welcome offers vary and you may not be eligible for an offer. Apply to know if you’re approved and find out your exact welcome offer amount – all with no credit score impact. If you’re approved and choose to accept the Card, your score may be impacted.

- Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year.

- Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year.

- New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App.

- Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines.

- Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com.

- Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases.

- Pay It® lets you tap in the American Express® App to quickly pay for small purchase amounts throughout the month and still earn rewards the way you usually do. Plan It® gives you the option to split up big purchases into equal monthly payments with a fixed fee. You’ll know upfront exactly how much you’ll pay.

- Updated! $120 Dining Credit: Earn up to a total of $10 in statement credits monthly when you pay with the Gold Card at Grubhub (including Seamless), Buffalo Wild Wings, Five Guys, The Cheesecake Factory, and Wonder. This can be an annual savings of up to $120. Enrollment required.

- $100 Resy Credit: Get up to $100 in statement credits each calendar year at over 10,000 qualifying U.S. Resy restaurants after you pay for eligible purchases with the American Express® Gold Card. That’s up to $50 in statement credits semi-annually. Enrollment required.

- $84 Dunkin' Credit: Earn up to $7 in monthly statement credits after you pay with the American Express® Gold Card at U.S. Dunkin’ locations. Enrollment required.

- $120 Uber Cash on Gold: Enjoy up to $120 in Uber Cash annually with your Gold Card. Just add your Card to your Uber account and you'll get $10 in Uber Cash each month to use on orders and rides in the U.S. when you select an Amex Card for your transaction.

- New! As an American Express® Gold Card Member, you can enjoy complimentary Hertz Five Star® Status. Enjoy benefits like skipping the counter at select locations, adding an additional driver at no additional cost*, and vehicle upgrades**. Benefit enrollment and Hertz Gold+ registration are required. *Additional drivers must meet standard rental qualifications and must be a spouse or domestic partner to qualify as complimentary. Other additional drivers subject to fees. **Benefits are subject to availability and vary by location. Additional Hertz program Terms and Conditions including age restrictions apply.

- Take advantage of a $100 credit towards eligible charges* at over 1,300 upscale hotels worldwide when you book The Hotel Collection through AmexTravel.com or the Amex Travel App **. *Eligible charges vary by property. **The Hotel Collection requires a two-night minimum stay.

- Book your travel through the Amex Travel App with added peace of mind – backed by American Express® service and support. Only for American Express® Card Members.

- Whenever you need us, we're here. Our Member Services team will ensure you are taken care of. From lost Card replacement to statement questions, we are available to help 24/7.

- No Foreign Transaction Fees.

- Annual Fee is $325.

- Terms Apply.