You can now book Southwest flights now and pay later, but should you?

Last week, Southwest Airlines became the latest carrier to offer travelers the option to book flights now and pay later with the travel finance services company, Uplift. (Previously, this service was only available on Southwest Vacations packages.)

The service's main focus is making travel more attainable for some by offering monthly payment options when purchasing flights. The service is currently available for a number of airlines, including Alaska Airlines, Allegiant, Air Canada, Frontier, Spirit, United and others. It also has partnerships with a handful of online travel agencies, cruise lines and resorts.

It's always great to have more payment options, but there's a question on all our minds: is taking out a loan for travel a good idea? Here, I'll show you how Uplift works when booking airline tickets and the costs associated with using the service.

Let's dive in!

How Uplift works

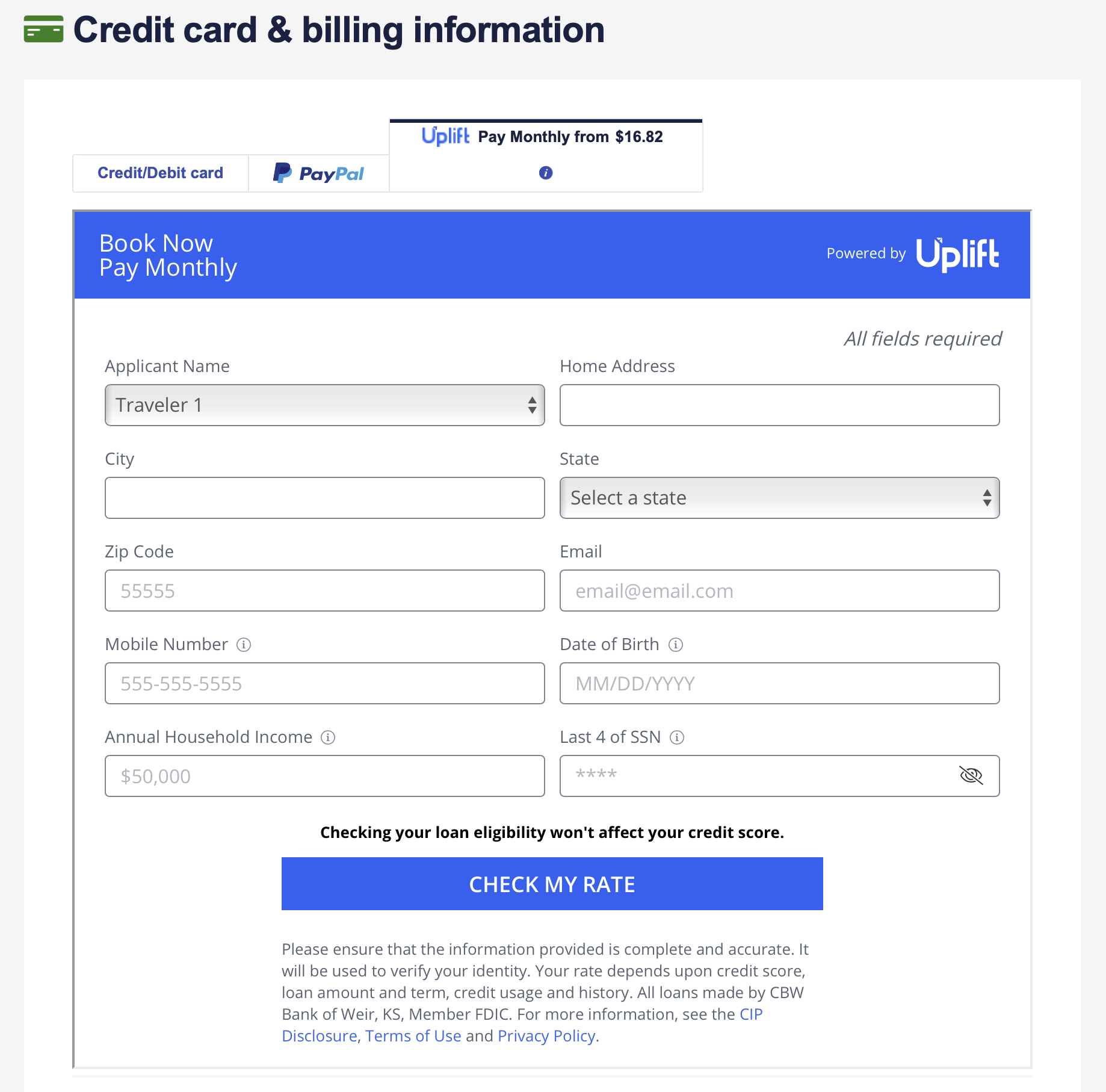

Using Uplift is simple. Head to Southwest's website, enter your desired itinerary and continue through the booking process as usual. You'll see a "pay monthly" option at the check-out screen where you can quickly apply for an Uplift loan. Uplift can be used on purchases of $100 or more.

The loan application asks for basic information like your address, income and last-four of your Social Security Number. The website states that loan applications are processed immediately and that checking loan eligibility doesn't affect credit, so it's likely a soft credit pull.

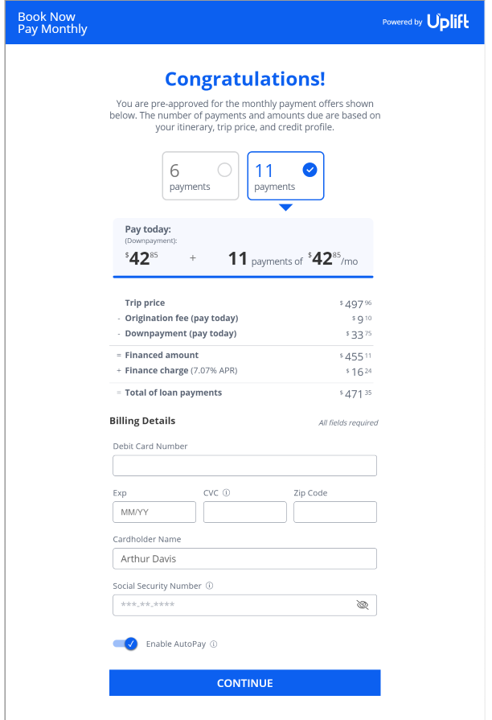

If approved, you'll be presented with your loan options. This includes a 6-month and 11-month loan term alongside their respective interest rates and monthly payments. There's may be a downpayment due at the time of booking on some bookings. Uplift states that your loan terms are based on your itinerary, trip price and credit profile.

You'll also be prompted to set up payments before completing your booking. You can pay with a debit card and have the monthly payment automatically charged to your debit card.

Related: 6 simple rules to stay out of credit card debt

costs associated with Uplift

There are a few costs associated with using Uplift to pay for your travel. As you'd expect, the most obvious expense is your interest. Uplift charges simple interest on all bookings, and — as discussed — your rate depends on your credit profile. Unlike carrying a balance on a credit card, Uplift only charges interest on the purchase, not the interest incurred over the life of the loan.

According to Uplift's website, APR can range between 0% and 36%. At the high-end, this is an incredibly high interest rate that's more than most credit cards. It's unclear when the company offers a 0% interest rate, but I suspect this is reserved for special limited-time offers. For example, Carnival Cruises is currently offering 0% promotional loans on cruises with $0 down.

You may be subject to a loan origination fee on some Uplift loans too. This fee varies based on your loan and doesn't look to be charged on all loans. Thankfully, Uplift has confirmed that origination fees are not charged on Southwest bookings. You'll also be asked to pay a downpayment when you first open your loan.

Related: 5 personal finance strategies that will help you to travel more this year

Does it make sense to finance travel with Uplift?

As a general rule of thumb, it's not the best idea to buy something you can't afford. However, there are certain situations where it's out of our control and having an option like this can save the day. For instance, if you have to book a last-minute emergency flight and can't swing the cost then this could be an option worth exploring.

If you do take advantage of Uplift's payment option, then you'll want to pay it off as soon as you can to avoid accumulating interest. However, you may be better off putting it on a credit card that has 0% or a low APR rate to avoid unnecessary interest charges. It depends on what interest rate you're quoted for and how soon you expect to pay the loan back.

At the same time, it's easy to see why airlines are adding Uplift as a payment method now. Leisure travel is recovering after being put on pause during the coronavirus pandemic. Splitting a travel expense up into monthly payments may be attractive to some travelers, even if it means paying interest and other fees.

Oh, and if you're curious: flights booked with Uplift will still earn miles like any other flight.

Related: 13 expenses that you should not put on your credit card

Bottom line

Using Uplift could be a great option if you have to take a last-minute emergency trip. Otherwise, it's generally best to not get yourself into debt just to take a spontaneous vacation. There are plenty of ways to earn points and miles every day that could ultimately lead to booking your dream vacation.

As the old saying goes: "Good things come to those who wait." In this case, don't rush a trip that you're not financially prepared for — focus on upping your points and miles game instead.

Additional reporting by Liz Hund

Feature photo by VDB Photos / Shutterstock.com

TPG featured card

at American Express's secure site

Terms & restrictions apply. See rates & fees.

| 4X | Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 4X | Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 5X | New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App. |

| 3X | Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines. |

| 2X | Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com. |

| 1X | Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases. |

Pros

- Valuable dining and food-related credits

- Flexible rewards with airline and hotel transfer partners

- Multiple travel and purchase protections

- No foreign transaction fees

- Access to Amex Offers for additional savings (enrollment required)

Cons

- Not as useful for those living outside the U.S.

- Some may have trouble using Uber and other dining credits

- You may be eligible for as high as 100,000 Membership Rewards® Points after you spend $8,000 in eligible purchases on your new Card in your first 6 months of Card Membership. Welcome offers vary and you may not be eligible for an offer. Apply to know if you’re approved and find out your exact welcome offer amount – all with no credit score impact. If you’re approved and choose to accept the Card, your score may be impacted.

- Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year.

- Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year.

- New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App.

- Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines.

- Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com.

- Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases.

- Pay It® lets you tap in the American Express® App to quickly pay for small purchase amounts throughout the month and still earn rewards the way you usually do. Plan It® gives you the option to split up big purchases into equal monthly payments with a fixed fee. You’ll know upfront exactly how much you’ll pay.

- Updated! $120 Dining Credit: Earn up to a total of $10 in statement credits monthly when you pay with the Gold Card at Grubhub (including Seamless), Buffalo Wild Wings, Five Guys, The Cheesecake Factory, and Wonder. This can be an annual savings of up to $120. Enrollment required.

- $100 Resy Credit: Get up to $100 in statement credits each calendar year at over 10,000 qualifying U.S. Resy restaurants after you pay for eligible purchases with the American Express® Gold Card. That’s up to $50 in statement credits semi-annually. Enrollment required.

- $84 Dunkin' Credit: Earn up to $7 in monthly statement credits after you pay with the American Express® Gold Card at U.S. Dunkin’ locations. Enrollment required.

- $120 Uber Cash on Gold: Enjoy up to $120 in Uber Cash annually with your Gold Card. Just add your Card to your Uber account and you'll get $10 in Uber Cash each month to use on orders and rides in the U.S. when you select an Amex Card for your transaction.

- New! As an American Express® Gold Card Member, you can enjoy complimentary Hertz Five Star® Status. Enjoy benefits like skipping the counter at select locations, adding an additional driver at no additional cost*, and vehicle upgrades**. Benefit enrollment and Hertz Gold+ registration are required. *Additional drivers must meet standard rental qualifications and must be a spouse or domestic partner to qualify as complimentary. Other additional drivers subject to fees. **Benefits are subject to availability and vary by location. Additional Hertz program Terms and Conditions including age restrictions apply.

- Take advantage of a $100 credit towards eligible charges* at over 1,300 upscale hotels worldwide when you book The Hotel Collection through AmexTravel.com or the Amex Travel App **. *Eligible charges vary by property. **The Hotel Collection requires a two-night minimum stay.

- Book your travel through the Amex Travel App with added peace of mind – backed by American Express® service and support. Only for American Express® Card Members.

- Whenever you need us, we're here. Our Member Services team will ensure you are taken care of. From lost Card replacement to statement questions, we are available to help 24/7.

- No Foreign Transaction Fees.

- Annual Fee is $325.

- Terms Apply.