Savvy Saturday: The secret to getting food with Capital One miles

Update: Some offers mentioned below are no longer available. View the current offers here.

Editor's note: Some travel cards come with awkward benefits that are difficult to maximize. This article is part of a series that shows you unique, fun and unintended ways to use your credit card benefits. If you've got any questions or have an example of a unique way to maximize a credit card perk, tweet us at @thepointsguy, message us on Facebook or email us at info@thepointsguy.com.

Every merchant in the world that accepts credit cards is assigned a merchant category code by each credit card network (American Express, Visa, Mastercard, etc.). Credit card issuers (Amex, Chase, Capital One, etc.) then use these codes to determine which categories your purchases fall into. These codes are important because they determine:

- How many points your rewards card will earn for your purchase

- If you can redeem credit card rewards points toward your purchase

For example, when you swipe a Visa card at Walmart, your purchase will often code as "5310," which tells your card issuer that you've shopped at a "discount store." However, a Walmart just down the road may code as "5411," which indicates to Visa that you were shopping at a "grocery store." So if you've got a credit card that earns bonus points for groceries, you may get a bonus at one Walmart but not the other. The same is true with other categories as well, such as travel or dining.

By now, you probably know or have heard how easy it is to redeem Capital One miles at a rate of one cent each toward travel purchases when you have either the Capital One Venture Rewards Credit Card or the Capital One VentureOne Rewards Credit Card (miles' value is less than that when cashed in for statement credits toward other types of purchases). That makes Capital One miles great for lowering your out-of-pocket vacation expenses for things like airfare, hotels, rental cars and more. As long as a purchase you make with your Capital One card codes as some type of travel category, you should be able to redeem Capital One miles at that rate of one cent apiece for it.

But did you know you can also use miles at that preferential rate for food purchases? Capital One doesn't necessarily intend for their miles to be used in this way, but I'll show you how to do it.

The secret: Restaurants inside hotels

The Capital One Venture and Capital One VentureOne cards are issued by Visa. Restaurants generally code with Visa as "5812" (Eating places and Restaurants), or "5814" (Fast Food Restaurants), which are not travel-related. That's disappointing because eating out can be a big expense during your travels -- the ability to offset the price of food would be a huge boon to folks with Capital One miles.

But there actually is a way to use Capital One miles toward dining: Eat at restaurants inside hotels. They're not hard to find if you're in the city or a popular tourist destination and purchases at them usually code as a hotel charge rather than a restaurant one. So if you have Capital One miles, you might be able to redeem them for purchases at the 1-cent rate since hotels fall into Capital One's travel category.

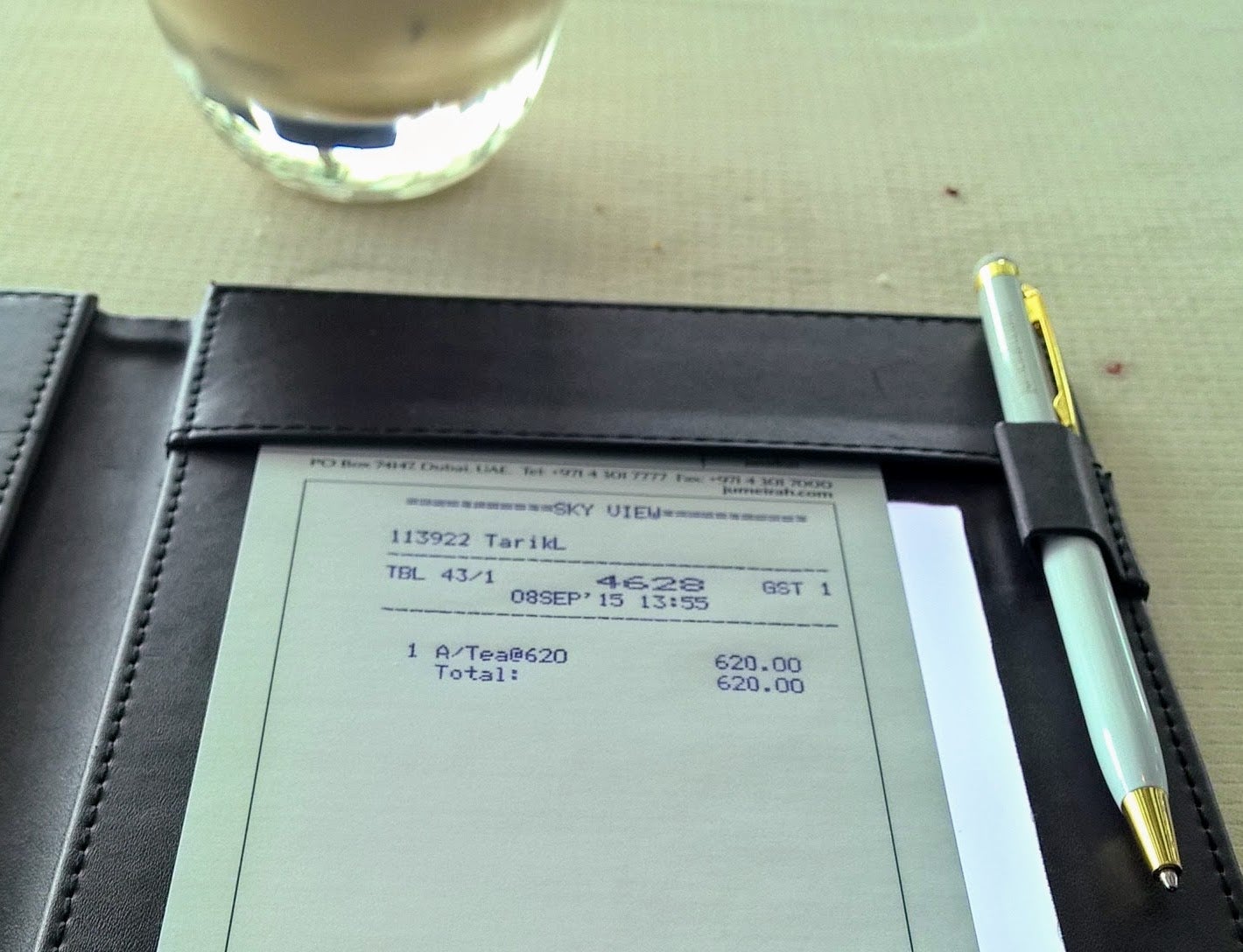

I personally used Capital One miles to offset the cost of afternoon tea at the Skyview Bar & Restaurant in Dubai at the top of the legendary Burj Al Arab hotel. Because the charge was coded as hotel purchase, it was easy to redeem miles from my Capital One Venture for the charge at 1 cent apiece.

The seven-course tea costs approximately $170 per person and it's an experience I wouldn't have booked unless I knew I could offset the cost with rewards and save a few hundred dollars. In hindsight, though, it was so lavish and delicious that I would have paid cash for it. I highly recommend it.

Not all hotel-operated restaurants code as travel, however. When that happens, there's a simple solution.

How to find qualifying restaurants

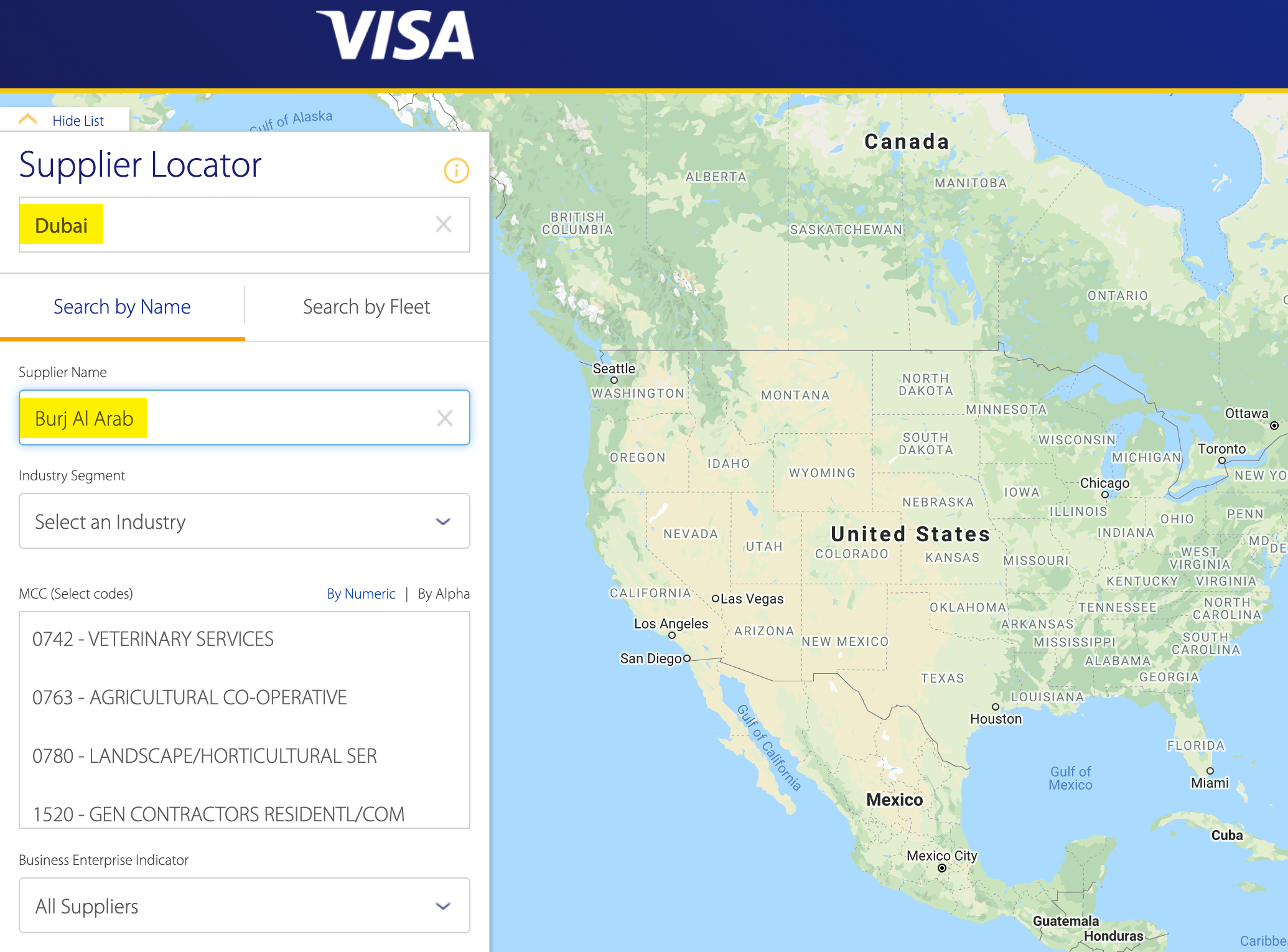

How will you know if your hotel restaurant purchase will code as a travel merchant? Because the Capital One Venture is a Visa card, you can use this Visa Supplier Locator to determine how your purchase will code with reasonable accuracy.

What works

Let's run through my above meal in Dubai. I'll enter the location and hotel into the Visa Supplier Locator.

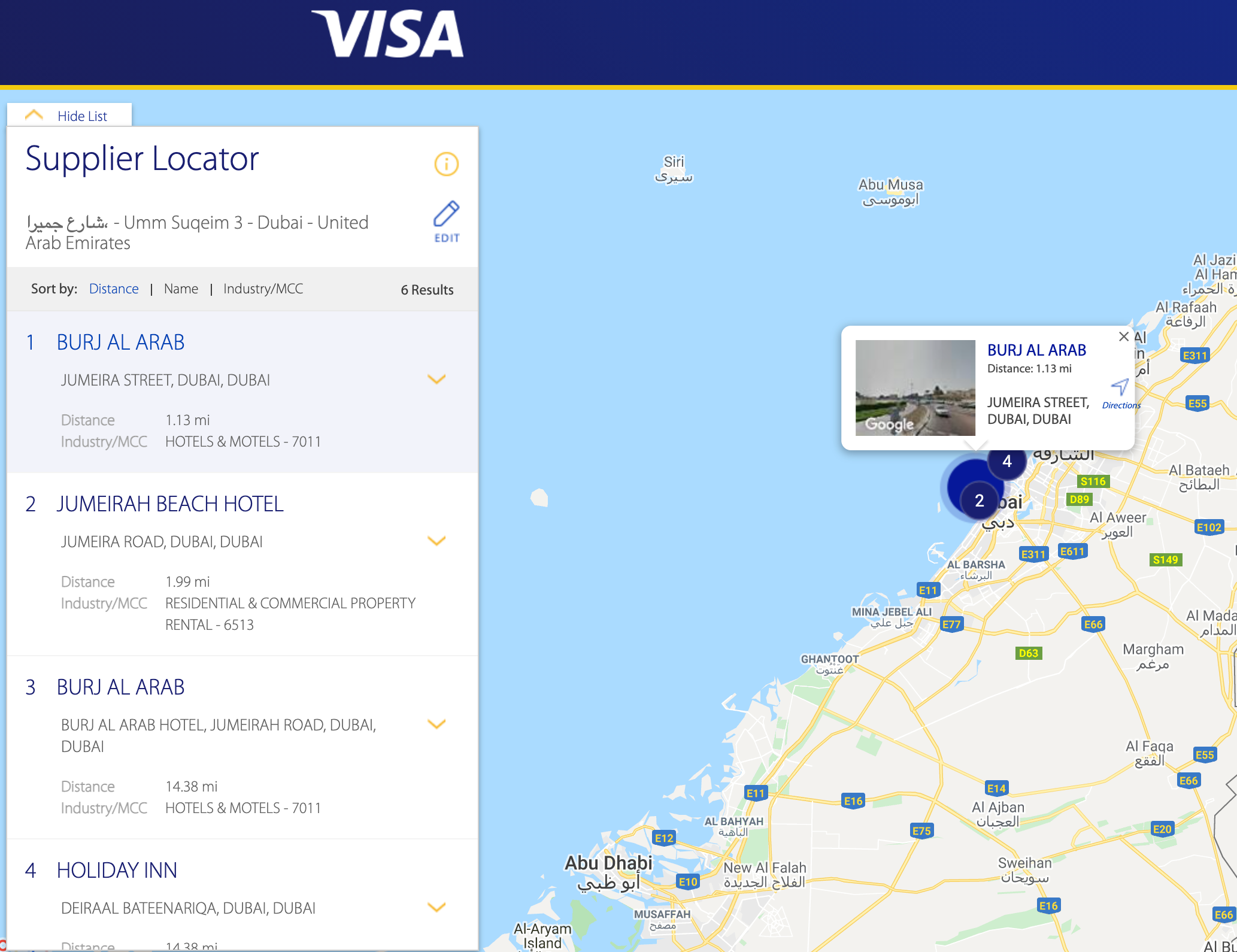

Visa then reveals that the Burj Al Arab codes as "HOTELS & MOTELS - 7011." That's definitely travel-related.

But when I search for the Skyview Bar & Restaurant instead of the Burj Al Arab, Visa cannot find the venue. That's because, as far as Visa knows, Skyview is the same entity as the Burj Al Arab. Whether I'm spending money on a hotel room at the Burj or just a meal at its restaurant, it will code as "HOTELS & MOTELS - 7011."

What doesn't work

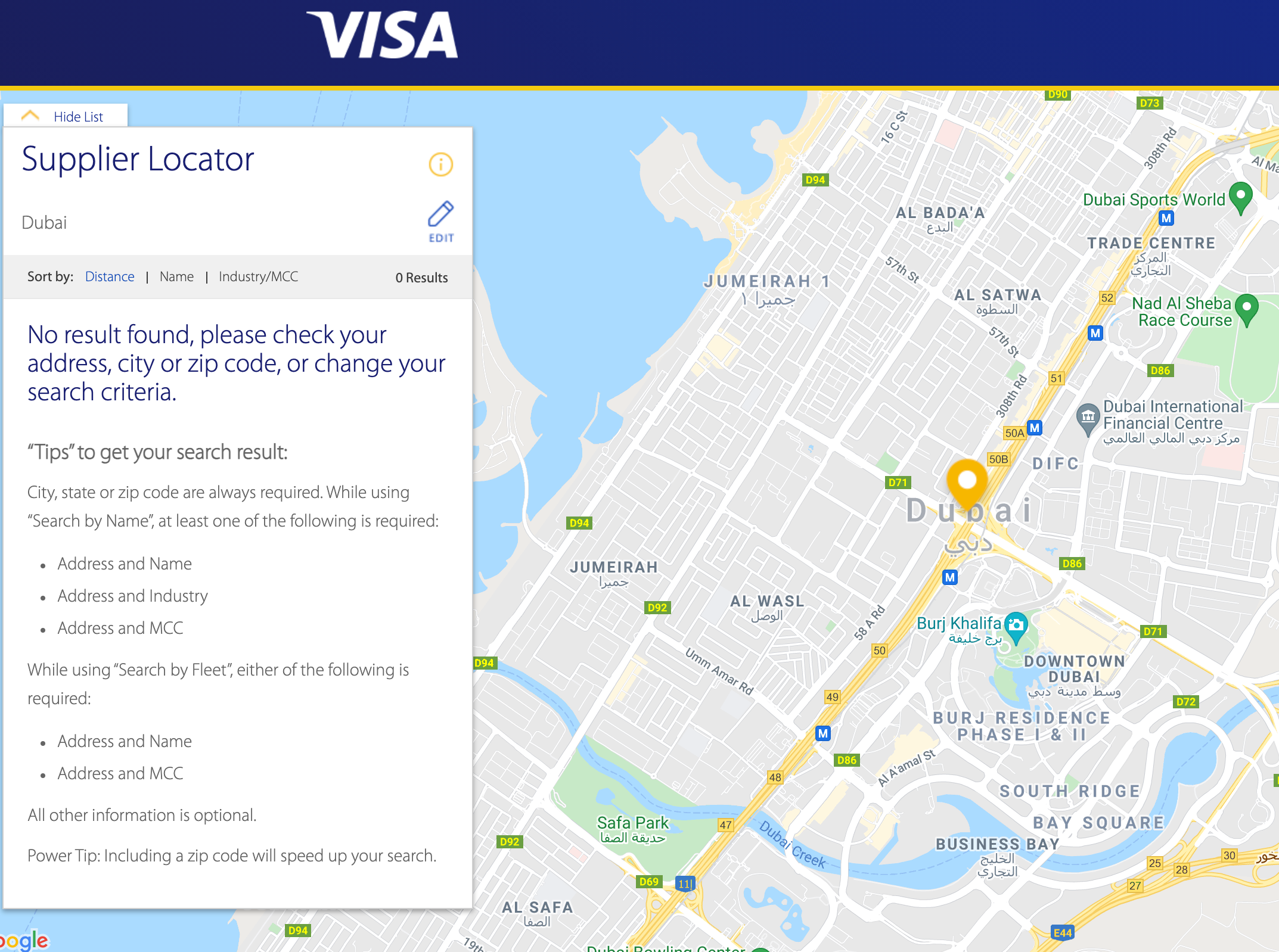

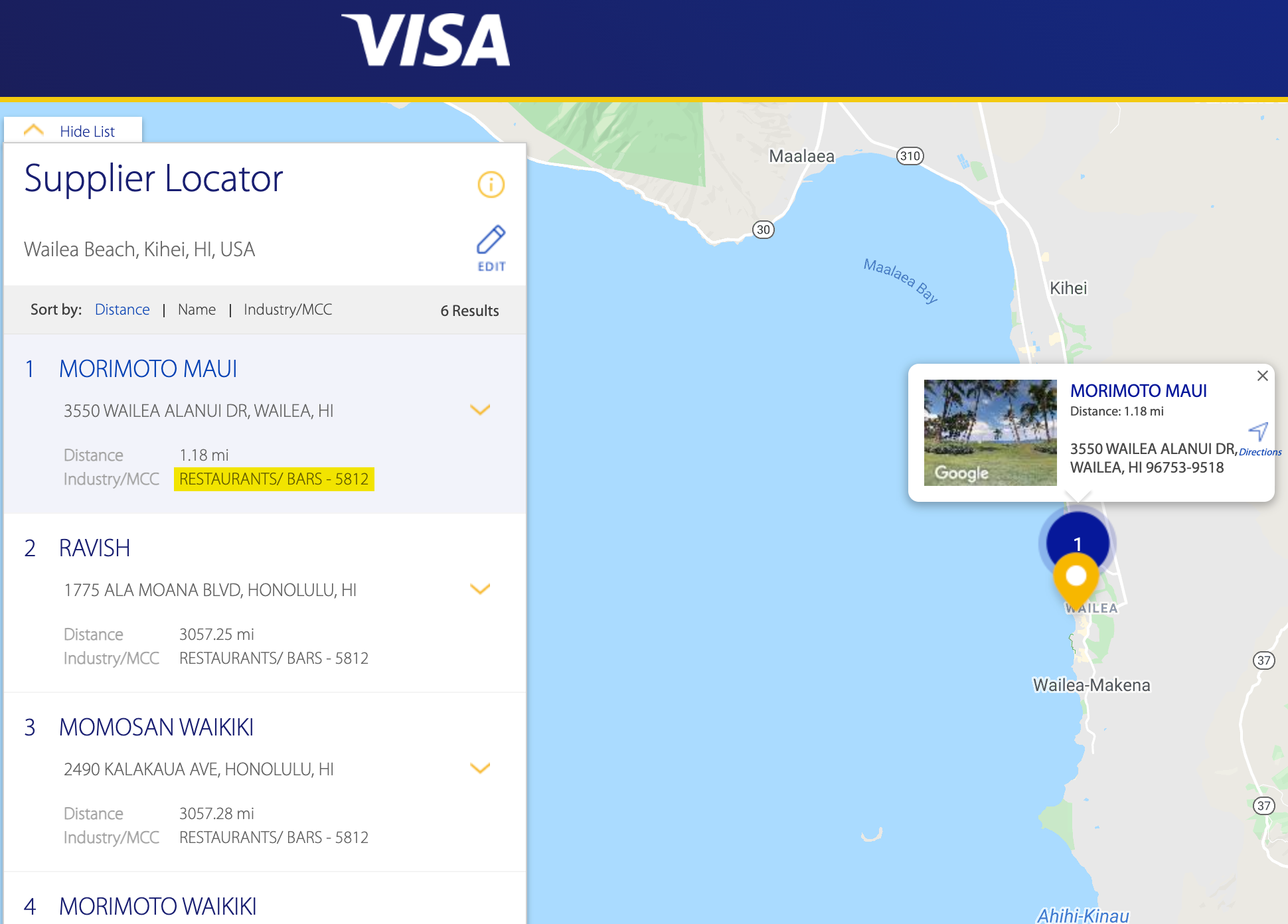

Now let's look at a hotel restaurant that doesn't code as travel. Admittedly, I haven't personally tested this hotel with a Capital One credit card, so if this doesn't work for some reason, I'd love to hear about it.

The Andaz Maui possesses a handful of quality dining options. On the premises is Morimoto Maui, an expensive Japanese fusion restaurant. Here it is with the Visa Supplier Locator, coding as "RESTAURANTS/BARS." That's not good. You won't be able to redeem Capital One miles for a meal here.

But if we look at another restaurant at the Andaz Maui, Ka'ana Kitchen, Visa can't find it. It's the same entity as the Andaz Maui. That's good. When you spend money at Ka'ana Kitchen, Visa should indicate to Capital One that you're at a hotel.

Earn Capital One miles

Until 2019, there was only one reasonably valuable option for redeeming Capital One miles: Redeeming them at a rate of 1 cent each for travel charges. Now, you can transfer Capital One miles to airlines and hotels to potentially get even more value from them. Per TPG valuations, Capital One miles are worth 1.85 cents each when you transfer to travel partners.

However, using your points to offset travel purchases is by far the easiest way to use your miles -- and still a very popular option. No matter which avenue you choose, you can earn Capital One miles quickly by earning the sign-up bonuses on and spending regularly with credit cards, including:

- Capital One Venture Rewards Credit Card: Earn 75,000 bonus miles when you spend $4,000 on purchases in the first three months from account opening.

- Capital One VentureOne Rewards Credit Card: Earn 20,000 bonus miles after spending $500 on purchases within the first three months from account opening

- Capital One Spark Miles for Business: Earn 50,000 bonus miles after spending $4,500 on purchases within the first three months from account opening

- Capital One Savor Cash Rewards Credit Card: Earn $300 after you spend $3,000 on purchases within the first three months of account opening (you can convert your $300 back into 30,000 miles if you also have a Capital One miles-earning card)

The information for the Capital One Savor Cash Rewards Credit Card has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.

Bottom line

Capital One miles are easy-to-use for travel purchases and get you a solid rate of return of 1 cent per mile when you redeem them this way. Unfortunately, miles are worth less when redeemed for statement credits toward non-travel charges, including dining and restaurants. However, if you find a restaurant inside a hotel, Capital One will often code this spending as a hotel charge instead of a restaurant one and thus allow you to redeem your miles at the higher rate against these purchases.

Tons of eligible restaurants worldwide code as hotels, and you can use the Visa Supplier Locator to find them easily. If you're actually staying at a hotel, you can order room service, and food that you pay for as part of your room bill should code as travel, too.