What is a credit card welcome offer? How they work and how to maximize value

If you've been considering opening a credit card, you've likely come across the term "welcome offer."

These bonuses can be one of the most valuable parts of a new card — sometimes worth hundreds of dollars in cash back, points or travel rewards.

But they often come with specific requirements, timelines and rules that can feel complicated to understand, especially if you're new to the world of credit cards.

Knowing how these offers work and what it takes to earn them can help you get the most value from a new card.

Here's what to know.

What is a welcome offer?

A credit card welcome offer is a limited-time incentive offered by issuers to new cardholders. Typically, you'll earn a lump sum of points, miles or cash back after meeting a required spending threshold within a set time frame.

For example, a card might offer 80,000 bonus points after you spend $4,000 in the first three months from account opening. Depending on how you redeem them, those points could be worth hundreds (or even thousands) of dollars.

Welcome offers are one of the fastest ways to earn a large amount of rewards at once, which is why they're often a key factor not to be overlooked when choosing a new credit card.

Related: The current best credit card welcome bonuses

How do I know when a welcome bonus is "good"?

As a general rule, a good welcome offer is one that delivers strong value relative to the card's cost and aligns with how you plan to use the rewards.

A strong offer depends on a few key factors:

- The size of the bonus (points, miles or cash back)

- How much those rewards are worth when redeemed

- The minimum spending requirement

- The card's annual fee

- The card's ongoing benefits.

To estimate the value of a welcome offer, you can use TPG's valuations, which provide a cents-per-point value on a monthly basis for major U.S. airline, hotel loyalty programs and leading transferable rewards currencies.

For example, if a card offers 60,000 points and TPG values those points at 1.5 cents each, the bonus would be worth $900. From there, weigh that value against the card's annual fee and whether you can comfortably meet the spending requirement.

It's important to note that not all points are created equal. Their value varies by issuer, can fluctuate over time and can change depending on how you redeem them. Using points through an issuer's portal or a statement credit will usually yield less value than transferring them to travel partners.

Using these valuations as a baseline can help you compare offers more accurately and understand the potential "real-world" value of a bonus.

Timing is also an important consideration. Welcome offers often increase for a limited time, so applying when a bonus is elevated can significantly boost the value you get.

Check out our offer history guides when you're looking to apply for your next credit card:

- The best time to apply for these popular Chase credit cards based on offer history

- The best time to apply for these popular American Express credit cards based on offer history

- The best time to apply for these popular Citi credit cards based on offer history

- The best time to apply for these popular Capital One credit cards based on offer history

Related: Top welcome offers: Best credit cards to apply for right now

What counts toward minimum spending?

Most everyday purchases count toward a card's minimum spending requirement, including:

- Groceries

- Dining

- Gas

- Travel

- Online purchases

However, some transactions typically don't count, such as:

- Annual fees

- Balance transfers

- Cash advances

- Fees (like late payment or foreign transaction fees)

- Certain peer-to-peer payments

Because each issuer defines what qualifies as an eligible purchase, it's important to review your card's terms before you start working toward a bonus. When in doubt, assume transactions that don't involve a standard purchase (like moving money or paying fees) won't count.

In some cases, large planned expenses can make it easier to meet a spending requirement.

I recently earned a welcome offer by paying a tax bill with a new card. That said, payments like these often come with processing fees, so it only makes sense if the bonus's value outweighs the cost.

Related: 10 ways to meet the spending requirements and earn the bonus on a new card

How long do I have to earn the bonus?

Most credit cards give you anywhere from 90 days to six months to earn the welcome bonus, starting from the date you're approved — not when you receive your card.

That deadline is firm. If you're short by $1 or miss it by a few days, you'll usually forfeit the bonus.

Some issuers, including American Express and Capital One may provide an instant card number upon approval, so you don't have to wait for your card to arrive in the mail to start working toward the bonus.

In many cases, you can also add your card to a digital wallet before the physical card arrives, giving you a head start on meeting the requirement.

Related: Credit cards that offer instant card numbers upon approval

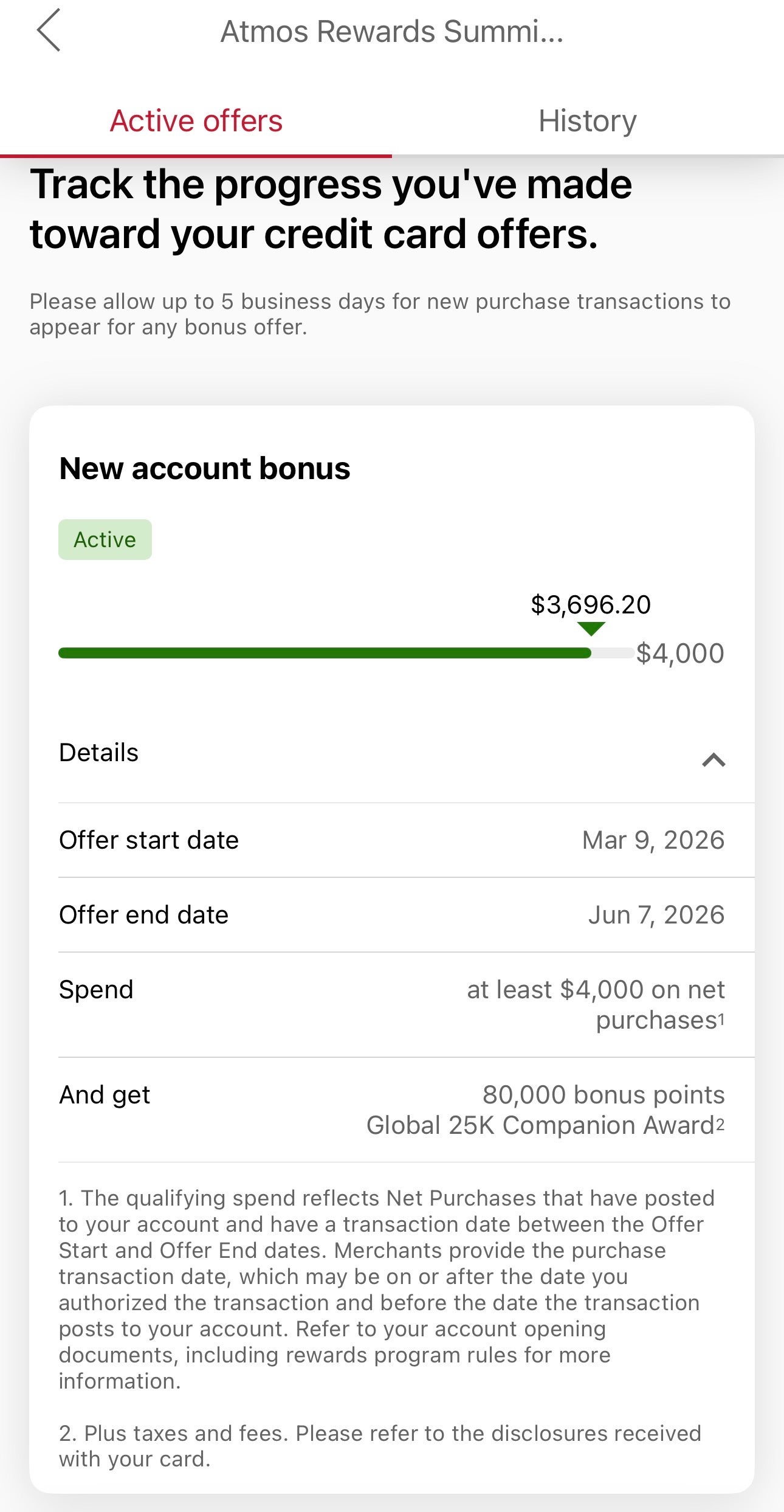

When will I receive the bonus?

Once you meet the spending requirement, your welcome bonus will typically post within one to two billing cycles.

In some cases, it may appear sooner, especially if you meet the requirement early in your statement period. You can usually monitor your progress through your issuer's website or mobile app.

Most issuers, such as Capital One, American Express, Citi and Chase have built-in trackers in their portals so that you can clearly track how close you are to earning the bonus.

Related: How to track your progress toward a credit card welcome bonus

Can I earn a welcome offer more than once?

It depends on the issuer. Each bank has its own rules for how often you can qualify for a welcome offer — and some are much stricter than others.

Here's how the major issuers approach eligibility:

- American Express: Limits welcome offers to once per lifetime ,per card.

- Chase: Applies restrictions like the 5/24 rule and may limit eligibility if you've previously earned a bonus on the same card.

- Citi: Generally allows you to earn a welcome offer again after a set waiting period.

- Capital One: May restrict eligibility based on how many cards you've opened or currently have.

Because these rules vary and individual offers may include additional terms, it's important to check the details on any offer before applying.

If you're not eligible for a welcome offer or don't meet the spending requirements in time, you won't receive the bonus.

Related: The ultimate guide to credit card application restrictions

Do returns affect minimum spend?

If you return a purchase, the refunded amount is typically deducted from your progress toward the minimum spending requirement.

This can drop you below the required threshold, so it's a good idea to spend slightly above the minimum if you're thinking about returning anything to give yourself a buffer.

Related: How to maximize credit cards to become points-rich without spending a ton

Examples of current welcome offers

Here's a look at some current welcome offers, including spending requirements and total value, according to TPG's valuations:

| Card | Annual fee | Welcome offer | Welcome offer value* |

|---|---|---|---|

$895 (see rates and fees) | Find out your offer and see if you are eligible for as high as 175,000 bonus points after spending $12,000 on purchases in the first six months of card membership. Welcome offers vary, and you may not be eligible for an offer. | Up to $3,500 | |

$395 | Earn 75,000 bonus miles after spending $4,000 on purchases in the first three months from account opening. | $1,388 | |

$325 (see rates and fees) | Find out your offer and see if you are eligible for as high as 100,000 bonus points after spending $8,000 on purchases in the first six months of card membership. Welcome offers vary, and you may not be eligible for an offer. | Up to $2,000 | |

$95 | Earn 75,000 bonus points after spending $5,000 on purchases in the first three months from account opening. | $1,538 | |

$595 | Earn 75,000 bonus points after spending $6,000 on purchases in the first three months from account opening. | $1,425 | |

$95 | Earn 70,000 bonus points and a $99 Companion Fare (plus taxes and fees from $23) after spending $2,500 on purchases in the first 90 days from account opening. | $1,085 (based on TPG's July 2026 valuations) |

*Offer value based on TPG's April 2026 valuations.

Targeted or limited-time offers can significantly increase these values, so it's worth checking the latest offer details before applying.

Related: 16 cards currently offering welcome bonuses of 100,000 points or more

Bottom line

A credit card welcome offer can be one of the fastest ways to earn hundreds (or even thousands) of dollars in value, but only if you understand how to earn it.

To get the most out of it, focus on the details: meet the spending requirement on time, understand what purchases count and pay attention to timing when offers are elevated.

With the right approach, a welcome bonus can significantly boost the value you get from a new card.

For rates and fees of the Amex Platinum, click here.

For rates and fees of the Amex Gold, click here.

Related: 11 credit cards that can get you $1,000 or more in first-year value

Updated 07/01/2026