How I learned that my credit card number was stolen

Update: Some offers mentioned below are no longer available. View the current offers here.

Data breaches, identity theft and other forms of fraud are rampant these days. I've been fortunate to avoid any potential issues along these lines — until today, that is. My Chase Freedom Unlimited account number somehow fell in the wrong person's hands. And here's how Chase let me know about it.

At 10:33 a.m. on Tuesday morning, I received this email from Chase:

"We've sent an important communication to your Secure Message Center, available on Chase Online or on the Chase Mobile app.

The subject is: URGENT: Action needed to confirm activity on your Chase Freedom Unlimited account."

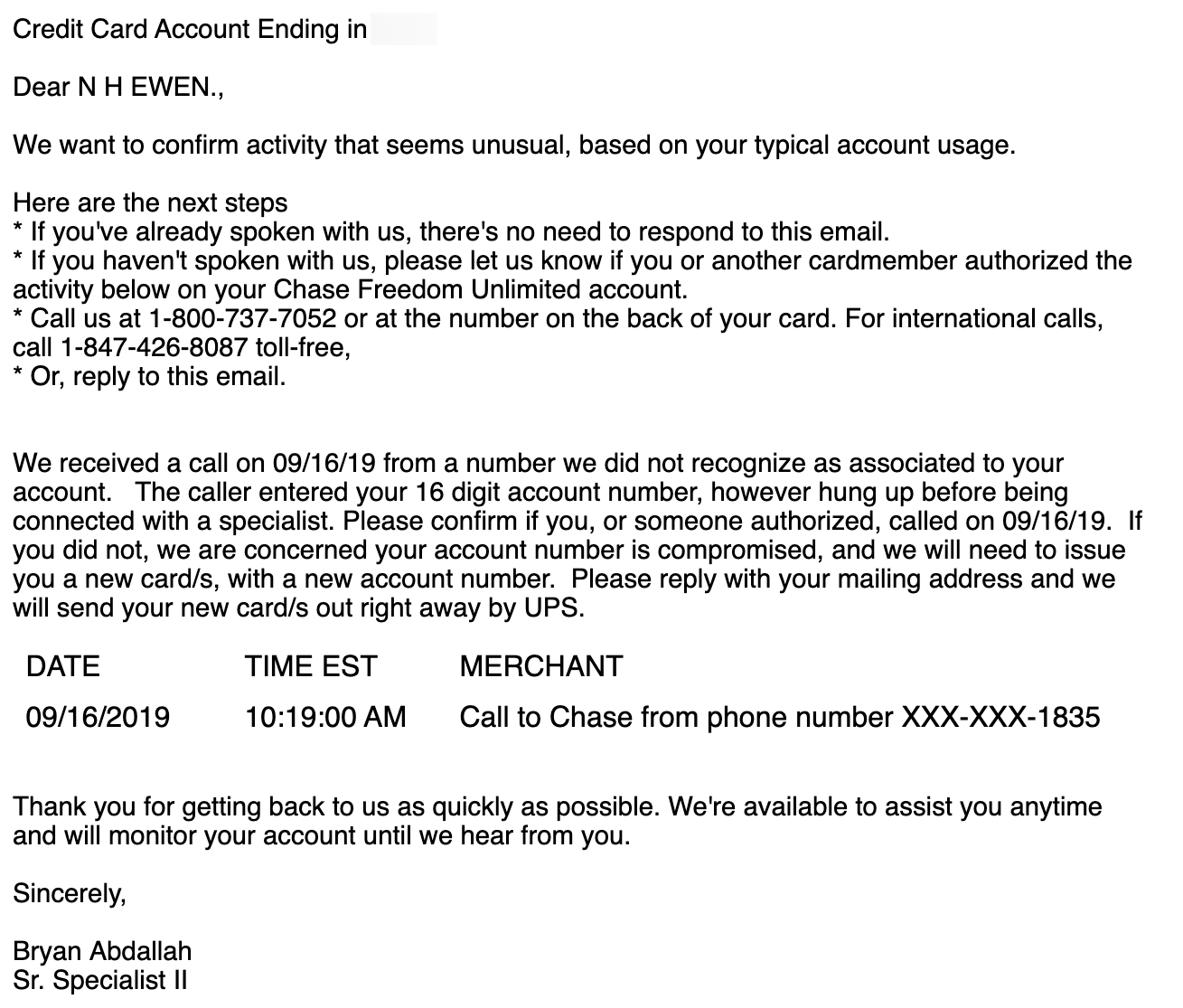

Not one to ignore an alert from a verified source with "URGENT" in all caps, I immediately logged into my account and accessed my secured messages. This is what awaited me:

I immediately called the number on the back of my card and was prompted to enter the last four digits of my account. After a few recorded messages, I was connected with an agent who quickly pulled up my account. I let her know about the message I had received and that the call was most definitely not from me, nor had I authorized anyone to call on my behalf. In an abundance of caution, I asked for the card to be cancelled and a new one sent.

She verified several pieces of information to ensure that it was (in fact) me this time, and then let me know that a replacement card would be sent via UPS to my home address with overnight shipping at no charge. She asked me if there was anything else she could help me with and then thanked me for my loyalty to Chase.

Total call time: 3 minutes, 56 seconds.

Just 32 minutes after the fraudster called Chase, my (apparently stolen) card number was cancelled, all because Chase's system flagged an unknown phone number from someone that was in possession of my 16-digit account number.

The Freedom Unlimited is my go-to card for everyday spending and a key part of what I consider to be the perfect quartet of Chase cards. While it's a bit inconvenient to need to update that card with the various providers that have it on file, it's a small price to pay to prevent unauthorized use of my account.

How to protect your credit card accounts

Here are things you can do to protect your accounts, many of which may have saved me this time:

1. Enable two-factor authentication wherever possible

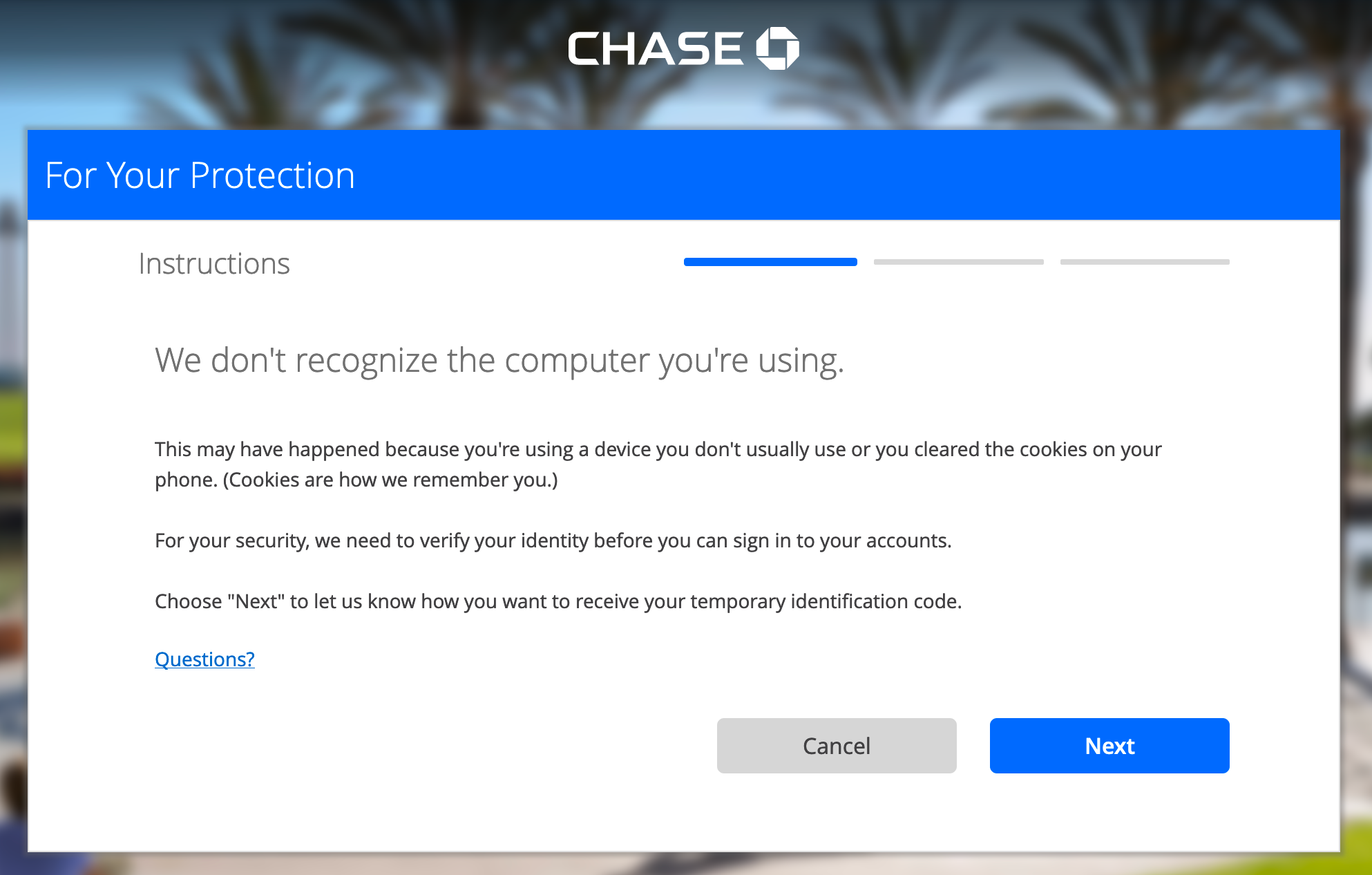

For any online account — be it a bank, credit card or merchant — you should always take advantage of two-factor authentication. This prevents someone from accessing your account with just your password, instead requiring an added authorization via a text message, phone call, email or third-party verification app. Chase, for one, sends a temporary verification code whenever I try to log in to my account from a browser it doesn't recognize.

The extra step may seem like a hassle, but it's far better than having your account compromised.

2. Update your email address and phone number(s)

Setting up two-factor authentication may only work if you have the right email address and phone number(s) on your account, so you want to make sure those are accurate. This has the added ability of getting quick notification of possible fraud, like I did this morning.

Speaking of fraud alerts ...

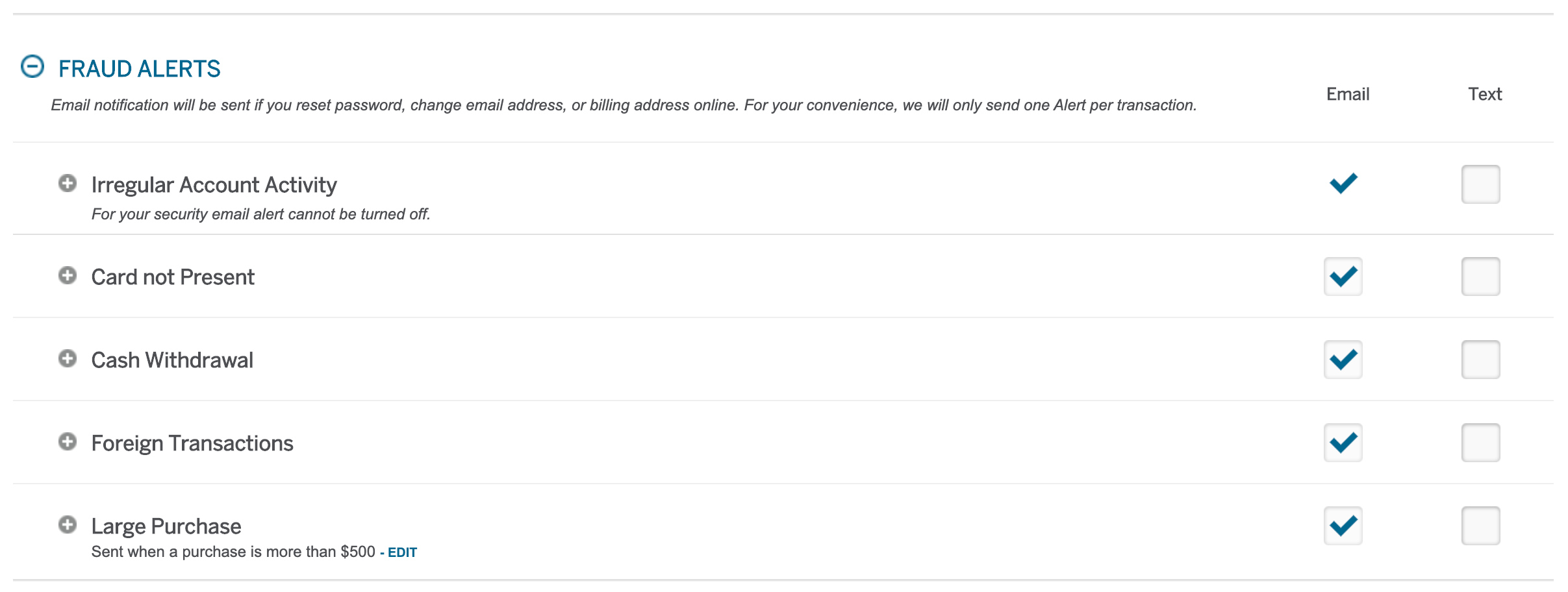

3. Ensure alerts are sent where you want

Many companies allow you to specify where you want to receive notification of potential fraud. For example, American Express has an Account Alerts section of your online profile that allows you to specify the kind of alerts you get and where you get them — including the ability to customize the threshold of a "large" purchase.

An email alert isn't of much use if you're traveling abroad and have turned your data off while roaming, but a text message may reach you.

4. Regularly monitor your accounts

Many TPG readers probably don't have the 20+ credit cards to monitor that I do, but even if you only have one or two, get in the habit of logging in at least a couple of times a week to note if there are any pending (or posted) charges you don't recognize. Fraudsters may start small, spending $5 here and $10 there, hoping you'll overlook them before making a massive purchase. Even though most credit cards offer fraud protection coverage, it's better to identify possible problems sooner rather than later.

Bottom line

I have to commend Chase for identifying this potential vulnerability on my account, not only for the speed in which it was done, but how it was done. It's the first time I've heard of an issuer flagging an unauthorized phone number that had my full card number, and I'm hopeful that my quick action has squashed any chance that Mr. or Ms. XXX-XXX-1835 could use my card. While there's no foolproof way to prevent fraud entirely, you can at least reduce your risk of it by taking a few simple steps to add additional layers of security to your accounts.

TPG featured card

at American Express's secure site

Terms & restrictions apply. See rates & fees.

| 4X | Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 4X | Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 5X | New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App. |

| 3X | Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines. |

| 2X | Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com. |

| 1X | Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases. |

Pros

- Valuable dining and food-related credits

- Flexible rewards with airline and hotel transfer partners

- Multiple travel and purchase protections

- No foreign transaction fees

- Access to Amex Offers for additional savings (enrollment required)

Cons

- Not as useful for those living outside the U.S.

- Some may have trouble using Uber and other dining credits

- You may be eligible for as high as 100,000 Membership Rewards® Points after you spend $8,000 in eligible purchases on your new Card in your first 6 months of Card Membership. Welcome offers vary and you may not be eligible for an offer. Apply to know if you’re approved and find out your exact welcome offer amount – all with no credit score impact. If you’re approved and choose to accept the Card, your score may be impacted.

- Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year.

- Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year.

- New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App.

- Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines.

- Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com.

- Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases.

- Pay It® lets you tap in the American Express® App to quickly pay for small purchase amounts throughout the month and still earn rewards the way you usually do. Plan It® gives you the option to split up big purchases into equal monthly payments with a fixed fee. You’ll know upfront exactly how much you’ll pay.

- Updated! $120 Dining Credit: Earn up to a total of $10 in statement credits monthly when you pay with the Gold Card at Grubhub (including Seamless), Buffalo Wild Wings, Five Guys, The Cheesecake Factory, and Wonder. This can be an annual savings of up to $120. Enrollment required.

- $100 Resy Credit: Get up to $100 in statement credits each calendar year at over 10,000 qualifying U.S. Resy restaurants after you pay for eligible purchases with the American Express® Gold Card. That’s up to $50 in statement credits semi-annually. Enrollment required.

- $84 Dunkin' Credit: Earn up to $7 in monthly statement credits after you pay with the American Express® Gold Card at U.S. Dunkin’ locations. Enrollment required.

- $120 Uber Cash on Gold: Enjoy up to $120 in Uber Cash annually with your Gold Card. Just add your Card to your Uber account and you'll get $10 in Uber Cash each month to use on orders and rides in the U.S. when you select an Amex Card for your transaction.

- New! As an American Express® Gold Card Member, you can enjoy complimentary Hertz Five Star® Status. Enjoy benefits like skipping the counter at select locations, adding an additional driver at no additional cost*, and vehicle upgrades**. Benefit enrollment and Hertz Gold+ registration are required. *Additional drivers must meet standard rental qualifications and must be a spouse or domestic partner to qualify as complimentary. Other additional drivers subject to fees. **Benefits are subject to availability and vary by location. Additional Hertz program Terms and Conditions including age restrictions apply.

- Take advantage of a $100 credit towards eligible charges* at over 1,300 upscale hotels worldwide when you book The Hotel Collection through AmexTravel.com or the Amex Travel App **. *Eligible charges vary by property. **The Hotel Collection requires a two-night minimum stay.

- Book your travel through the Amex Travel App with added peace of mind – backed by American Express® service and support. Only for American Express® Card Members.

- Whenever you need us, we're here. Our Member Services team will ensure you are taken care of. From lost Card replacement to statement questions, we are available to help 24/7.

- No Foreign Transaction Fees.

- Annual Fee is $325.

- Terms Apply.