How Do Charge Cards Affect Your Credit Score?

Update: Some offers mentioned below are no longer available. View the current offers here.

"Reader Questions" are answered twice a week by TPG Senior Points & Miles Contributor Ethan Steinberg.

With all the hype surrounding the Platinum Card® from American Express and the recently refreshed American Express® Gold Card, it's easy to forget that these aren't actually credit cards but charge cards. TPG reader Nodisha wants to know how using an Amex charge card will affect her credit score...

[pullquote source="TPG reader Nodisha"]I just got approved for the new rose gold Amex. I understand that this is a charge card — how does that appear on your credit report?[/pullquote]

Nodisha is spot-on with this question. It's important to understand the factors that affect your credit score so you can avoid violating the ten commandments of travel rewards and damaging your credit.

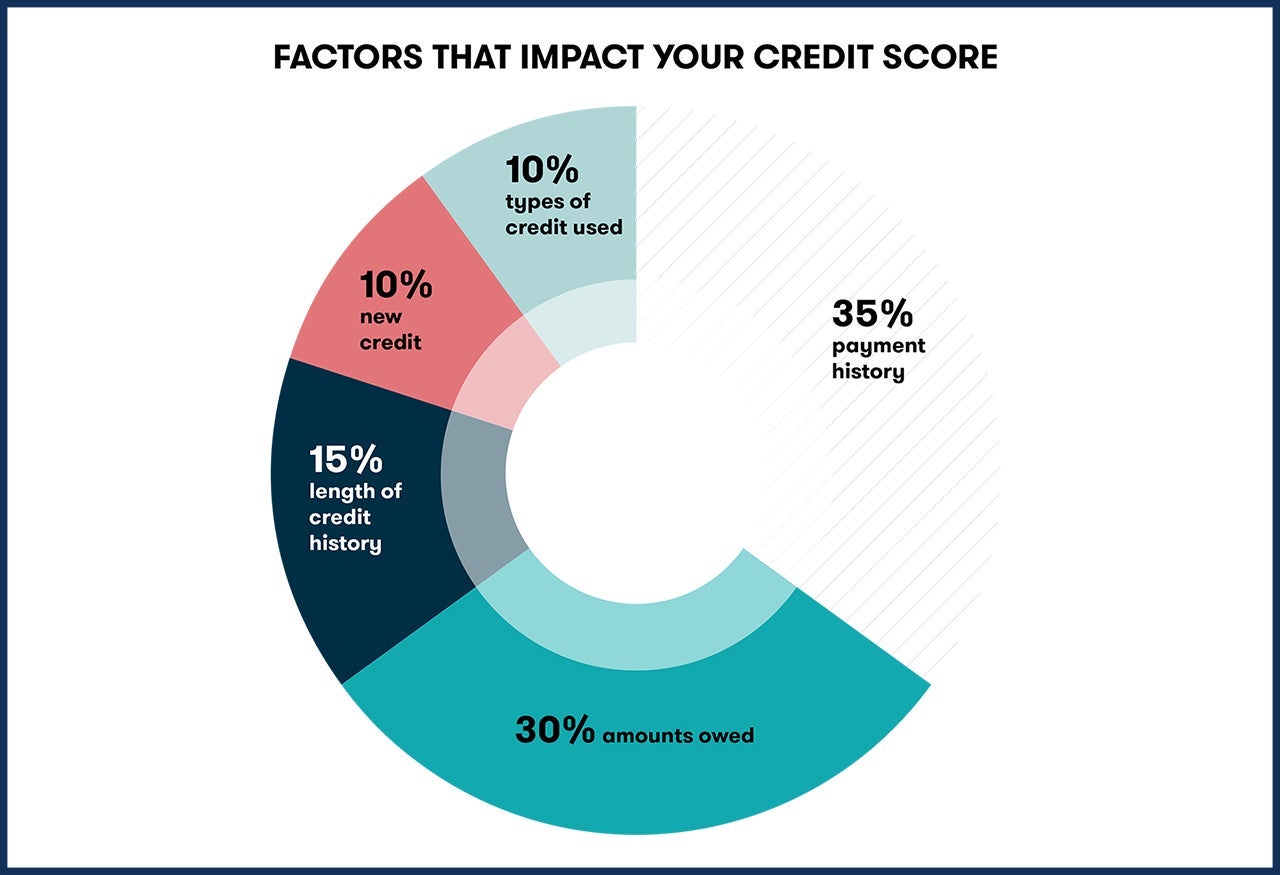

About 30% of your credit score is calculated based on your utilization, which is simply your total balances (amount owed) divided by your total credit. The lower your utilization, the higher your score.

Charge cards, which include both the personal and business versions of the Amex Platinum Card, Amex Gold Card and Amex Green Card, don't have a preset credit limit. Instead, your purchases are approved on a case-by-case basis based on your history with Amex. While this case-by-case approval sounds scary, I've never had my Platinum card denied before even when I had to use it for a five-figure emergency medical bill in a foreign country. With charge cards, you have to pay your balance in full every month so there's no option to carry a balance and rack up expensive interest payments.

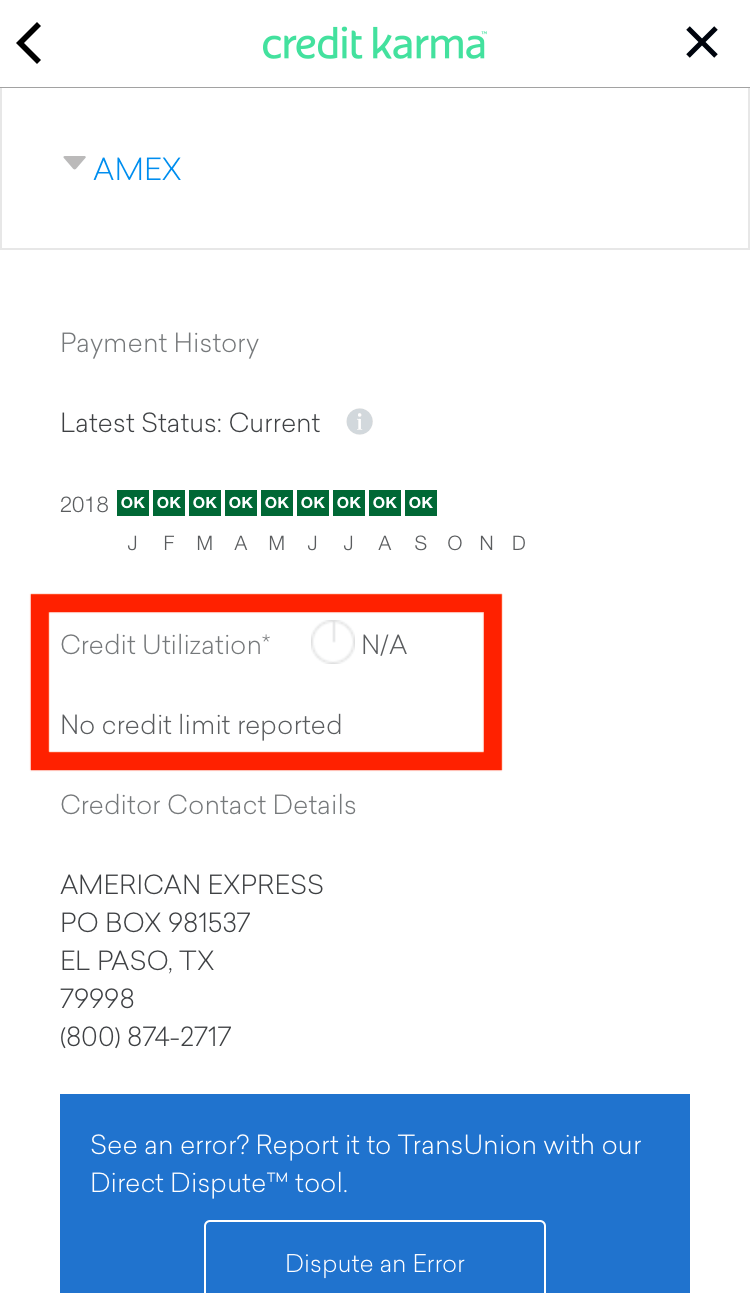

Because there's no preset spending limit with charge cards, it's mathematically impossible to calculate your utilization. Take your balance at the end of the month and... divide it by zero? If you check your credit report for an Amex charge card, you'll see that there is no utilization calculated:

In many ways, this means that charge cards share one of the best benefits of business credit cards, namely that purchases you make don't directly affect your personal credit report. Note that Amex will still report your statement balances to the credit bureaus, even if they don't affect your credit score. This means that other creditors looking at your report (for a mortgage or car loan, for example) will see the balance when deciding whether to approve you.

Bottom Line

Unless you're making an abnormally large purchase, it doesn't make sense to go out of your way to use a charge card, but Amex has given us plenty of reasons to use these cards in many aspects of our day-to-day lives anyway. From the Amex Platinum's 5x bonus category on select airfare purchases to the 4x on US restaurants and US supermarkets (on the first $25,000 in purchases each year) with the refreshed Amex Gold to 4X points applying to the first $150,000 in combined purchases from these 2 categories each calendar year on the American Express® Business Gold Card, which automatically rewards you in your top two spending categories each month (from a preset list), many of the best Amex cards happen to be charge cards. This credit reporting quirk is just an added bonus.

Thanks for the question, Nodisha, and if you're a TPG reader who'd like us to answer a question of your own, tweet us at @thepointsguy, message us on Facebook or email us at info@thepointsguy.com.