Debunking credit card myths: Is a debit card better for your credit history?

Update: Some offers mentioned below are no longer available. View the current offers here.

It's no surprise that travel rewards credit cards are a popular discussion topic here at TPG. By strategically opening and utilizing them, you can earn large sign-up bonuses and extra points in a variety of categories of everyday spending, opening up fantastic redemptions like premium-class flights and luxurious hotel rooms.

However, there are a number of misconceptions out there when it comes to credit cards, so today we're continuing our series that debunks these myths and allows you to begin planning for your next vacation.

Today, we're debunking a common myth when it comes to debit versus credit cards.

Myth: A debit card is better for building your credit history than a credit card

Many beginners in the world of cards prefer to use a debit card as opposed to a credit card for the majority of their transactions.

While this may be rooted in fear of the unknown, it also may be simple recognition of the dangers of a credit card. When you open a new card and get a credit limit of $20,000, that's not just free money. You may not trust yourself with a large line of credit and, instead, prefer to rely on the immediacy of a debit card. After all, there's no "buy now, pay later" aspect of a debit card. That money comes out of your bank account (almost) immediately.

Unfortunately, there's an important misconception when it comes to debit cards: These products do not have any impact on your credit score.

Hopefully, this is clear simply through semantics; why would a debit card impact your credit score? Nevertheless, we hear many beginners asking this exact question, so it's clearly still on people's minds.

Related: Why a credit card is a smarter choice than a debit card

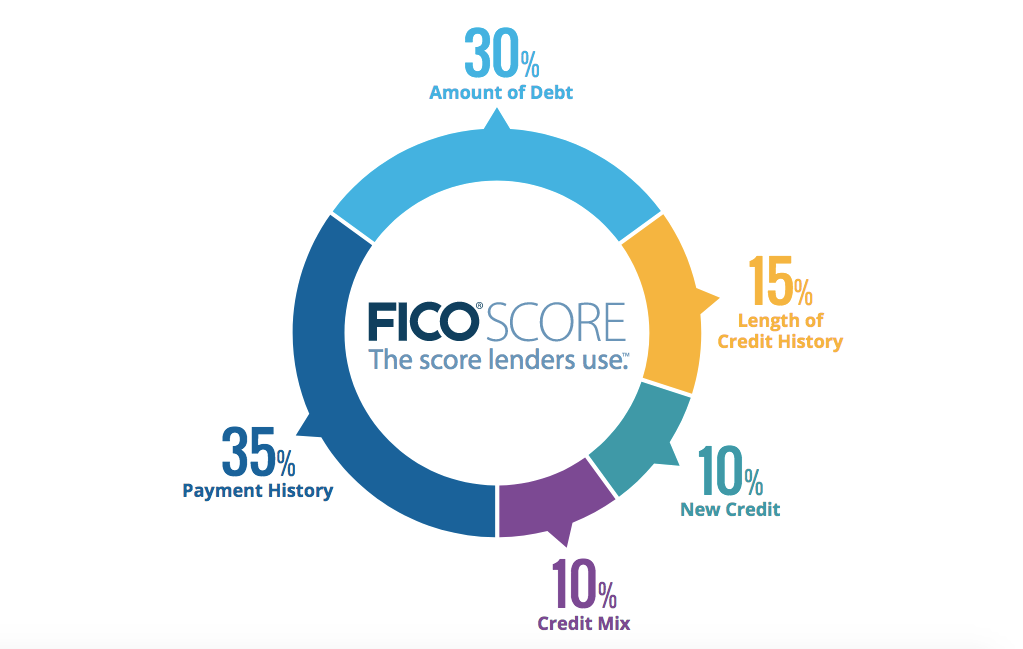

Credit score factors

At its most basic level, your credit score is a numerical representation of how well you manage lines of credit that have been extended to you. As we've covered in previous debunking myths stories, it's made up of five factors:

- Payment history

- Amounts owed

- Length of credit history

- New credit

- Types of credit used

Remember that these factors are not equal, as some are weighted more heavily than others:

As you can see, none of these apply to a debit card. There is no "payment history" on those accounts since every transaction comes out of your bank account individually. You'll never owe any amount on a debit card and since there isn't any type of credit line extended to you, the last three factors don't come into play either.

Related: How credit scores work

Use a credit card to improve your credit score

Unfortunately, over-relying on a debit card can come back to haunt you when you're looking to finance a new car or buy your first house or even apply to rent an apartment (where the landlord or leasing company runs your credit). If your credit history is minimal or even non-existent, you may run into difficulties securing these types of loans. Even if you do secure them, you may be charged higher interest rates due to the fact that the lender isn't sure of your creditworthiness.

All of this can be avoided by opening and utilizing a credit card. We recommend starting with a no-annual-fee card such as the Chase Freedom Unlimited® or Citi Double Cash® Card (see rates and fees) so you won't have to "invest" anything right off the bat. These cards also offer simple rewards for every purchase you make.

You'll want to carefully set boundaries for your spending so as not to rack up a huge bill. Also, be sure to pay off the balance in full every month. Even just a handful of transactions each statement period will demonstrate to the credit bureaus that you are responsibly managing your available credit, improving your credit score and making you more attractive to issuers down the road.

Related: Ten commandments for rewards credit cards

Bottom line

Debit cards often seem like a safer payment method than credit cards, since you aren't at risk of overextending yourself. The money comes out of your account right away, preventing a larger bill at the end of the month that will accrue interest charges at a very high rate.

However, using a debit card won't have any impact on your credit score, making it more challenging to obtain loans in the future. While you should always stay within the limits of what you can afford to actually purchase and pay for each month, a credit card should play at least some role in your financial strategy.

Additional reporting by Emily Thompson and Chris Dong.