TPG reader credit card question: How bad is it to get denied for a credit card?

Editor's note: This post has been updated with new information.

The fastest way to accumulate a meaningful amount of points and miles is by opening new travel rewards credit cards to earn the intro bonuses they offer. However, if you keep at this long enough and apply for a lot of cards, you are almost certain to get rejected on a credit card application eventually. So the question becomes: Are there any long-term ramifications if you get declined for a credit card?

This is an interesting question and one that readers have asked us many times. It's important to have a thorough understanding of the factors that affect your credit score before you start applying for credit cards so that you understand how a credit card rejection can impact you.

Are there long-term problems if I'm declined for a credit card?

Any time you apply for a new line of credit, whether it's a mortgage, car loan or credit card, the institution you're applying with will "pull" your credit report. These "hard inquiries" usually lower credit score temporarily by about five points. These types of credit pulls differ from "soft inquiries," which might happen when you open a new bank account or get your credit screened to sign a rental agreement. In a soft inquiry, the other party looks at your credit report but the inquiry doesn't then affect your credit score.

These inquiries fall off your credit report after about two years, though the temporary score drop usually rebounds before then. In most cases, you'll receive a hard credit pull whether you're approved for a card or rejected (although American Express has been known not to perform a hard pull for existing customers when it declines them for a new card).

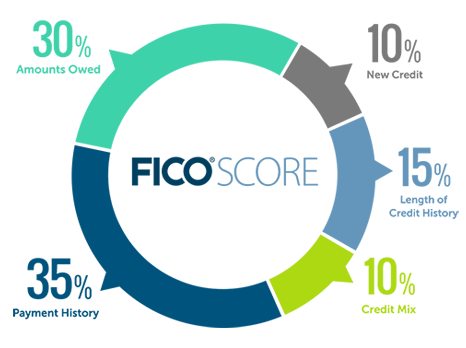

In this sense, the negative impact of applying for a new credit card is the same whether you get approved or rejected. Obviously, if you get approved, you get a new account and typically an increase to your total credit limit (not to mention a nice welcome bonus) which can help boost your credit score long term. On the other hand, since length of credit history and new credit account for 25% of your total FICO score, opening a new credit card account can also temporarily lower your score by bringing down the average age of your accounts. Overall, though, opening a new card and using it responsibly (i.e. paying it off on time and in full every month) should ultimately help raise your credit score.

As for rejections, there are not any uniquely negative effects if you're not approved for a new credit card. As a single data point, in over three years of collecting points and miles, I've been rejected for 12 different credit cards, and still have a credit score of about 780.

Study each issuer's application rules

While you shouldn't worry too much if your application gets rejected, you shouldn't just apply sporadically without understanding the unique eligibility rules of each different card issuer.

We're talking specifically about Chase 5/24 status and applying for Chase cards, since the issuer will probably automatically reject you if you've opened five or more credit cards in the last 24 months (except certain business credit cards). Even if you don't know your Chase 5/24 status off the top of your head, it's worth taking some time to sit down and figure it out instead of just applying randomly and hoping for the best.

The same goes for other issuers such as Amex, which limits you to only receiving the welcome bonus on each of its credit cards once per lifetime. You also have to be careful, as some issuers are especially sensitive to recent inquiries. Even if they don't have any formal rules like Chase's 5/24, Citi and Capital One have both been known to reject applicants with otherwise excellent credit for having too many recent inquiries on their credit report.

Read our ultimate guide to credit card application restrictions for everything you need to know.

Bottom line

Getting rejected for a credit card is unfortunate, but thankfully there should not be any permanent harm to your credit score. The five-point hit to your credit score from the hard pull and the inquiry itself will fade over time, meaning you shouldn't balk at applying out of fear of damaging your score for the long term. Still, you should make sure you know the rules of any issuer whose cards you're thinking of applying for. There's no good reason to waste a credit inquiry on a card you have absolutely no chance of getting, like applying for a Chase card when you're over that 5/24 limit.

Let us know if you have any head-scratchers you'd like answered for our weekly reader question series. You can tweet us @thepointsguy, message us on Facebook or email us at info@thepointsguy.com.

Additional reporting by Joseph Hostetler.

Featured photo by karen roach/Shutterstock.

TPG featured card

at Capital One's secure site

Terms & restrictions apply. See rates & fees.

| 5X miles | Earn 5X miles on hotels, vacation rentals and rental cars booked through Capital One Travel |

| 2X miles | Earn unlimited 2X miles on every purchase, every day |

Pros

- Stellar welcome offer of 75,000 miles after spending $4,000 on purchases in the first three months from account opening. Plus, a $250 Capital One Travel credit to use in your first cardholder year upon account opening.

- You'll earn 2 miles per dollar on every purchase, which means you won't have to worry about memorizing bonus categories

- Rewards are versatile and can be redeemed for a statement credit or transferred to Capital One’s transfer partners

Cons

- Highest bonus-earning categories only on travel booked via Capital One Travel

- LIMITED-TIME OFFER: Enjoy $250 to use on Capital One Travel in your first cardholder year, plus earn 75,000 bonus miles once you spend $4,000 on purchases within the first 3 months from account opening - that’s equal to $1,000 in travel

- Earn unlimited 2X miles on every purchase, every day

- Earn 5X miles on hotels, vacation rentals and rental cars booked through Capital One Travel

- Miles won't expire for the life of the account and there's no limit to how many you can earn

- Receive up to a $120 credit for Global Entry or TSA PreCheck®

- Use your miles to get reimbursed for any travel purchase—or redeem by booking a trip through Capital One Travel

- Enjoy a $50 experience credit and other premium benefits with every hotel and vacation rental booked from the Lifestyle Collection

- Transfer your miles to your choice of 15+ travel loyalty programs

- Top rated mobile app