Increase your credit score instantly: A guide to Experian Boost

Experian is best known as one of the three major credit bureaus alongside Equifax and TransUnion. Each of these three agencies collects your financial information and compiles that into a report for lenders, like credit card companies, to determine your creditworthiness.

However, you might not be as familiar with the various credit tools that are offered to help consumers better manage and understand your credit. After all, what good is a report if you can't parse out what it means?

Today, we'll take a look at Experian Boost, a relatively new tool from Experian that has the potential to increase your credit score instantly -- and for free. Too good to be true? Let's take a look at how "Boost" works and if it's right for you.

New to The Points Guy? Sign up for our daily newsletter and check out our updated beginner's guide.

What exactly is Experian Boost?

All of the credit bureaus gather, process, and analyze sensitive personal data for millions of Americans. Some of it -- either for a fee or free of charge -- is made accessible to you.

The premise behind Experian Boost is simple. It launched in 2019 as a tool to help individuals instantly increase their FICO score by including utilities and phone payments as part of their overall credit profile. Even on-time streaming service payments, such as Netflix, can help you improve your score.

The key is that those payments need to be completed on-time, and then they become baked into your credit score. As an added side benefit, Experian Boost also includes free credit monitoring and alerts.

Related: Should you invest in a credit monitoring service?

How does it work?

Experian markets Boost as an instant way to increase your FICO score. Here is how it works:

- First, you must connect your bank account that you use to pay your bills with Experian.

- Next, you'll select the positive utilities and telecom payment history to add to your credit profile.

- Finally, Experian says you should be able to instantly see an increase in your FICO score (if the bills make a material difference).

As you'll notice, you have to be willing to trust Experian to securely analyze your banking information. The credit bureaus (and banks for that matter) haven't had a sterling reputation in recent years when it comes to handling your personal data securely. This is just something to keep in mind if you decide to use the program.

Related: How paying your utility bills could help your credit score

Can it increase my credit score?

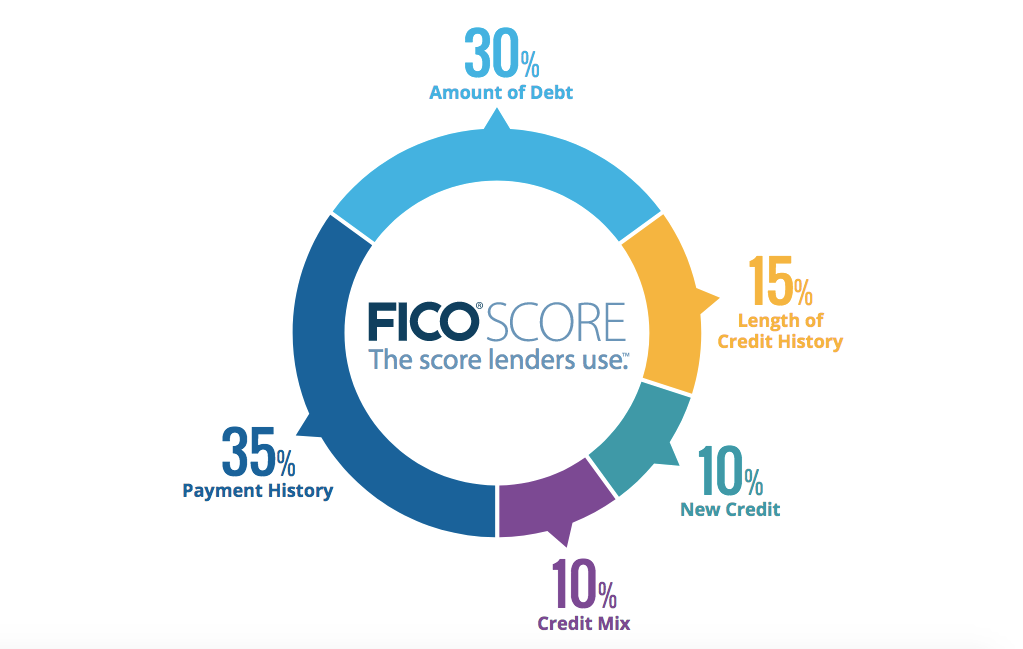

Experian Boost can possibly improve your credit score. By scanning for on-time bill payments, you can build positive payment history which is the most important factor in calculating your FICO credit score.

In addition, the length of your credit history is another crucial component of your score (15% of it). By adding more applicable data points, you'll have more proof of active accounts.

Experian Boost only applies to lenders that check Experian's records. It won't affect what's in your credit files with the two other major credit bureaus -- Equifax and TransUnion.

How does this impact you? Well, for instance, when you apply for a credit card, the issuer contacts a credit bureau (or several) to pull a copy of your credit report. If that issuer doesn't check Experian, having Boost will likely have no bearing on the status of your application.

Another thing to keep in mind is that lenders may not be familiar with seeing utility and cell phone payments on your credit report since Experian Boost launched relatively recently.

Who should consider getting Experian Boost?

For those with thin credit history and a "very poor to fair" score, Experian Boost could potentially expand your credit history.

By definition, those with "thin profiles" have less than five accounts to their name. According to Experian, 87% of consumers within this demographic saw an average FICO score increase of 19 points with Experian Boost.

Besides helping those with not-so-great credit, Experian Boost could possibly assist Americans that are deemed "unscoreable."

These individuals don't have enough credit history to even be assigned a score. However, in an initial first-year study, 47% of "unscorable" customers were able to obtain a credit rating after participating in Experian Boost. Granted, the majority of them fell into the Very Poor or Poor categories, but the potential impact is certainly there for a segment of the population to benefit from this product.

Are there other ways to increase your credit score?

There are several other ways to work towards getting a bump in your FICO (and VantageScore) numbers. One such option is applying for a secured credit card.

Secured cards require a security deposit upon opening, and the amount is generally tied to your overall credit limit. Using a secured card responsibly over time can improve your credit score.

Related reading: Best secured credit cards

Bottom line

Since its launch, 1.3 million consumers have used Experian Boost to increase their credit score. With that said, even with tools like Experian Boost, your credit score is a complicated algorithm, and the program isn't for everyone. It's mainly targeting individuals with either no credit to their name or those that fall into the "very poor to fair" buckets.

You don't have to feel tied to Experian's products and services as there are other options out there. However, this free service could be worth a try for those who are looking to build or repair their credit. And if you see any negative impacts on your score, you can easily disconnect your linked accounts.