Does applying for a new credit card hurt your credit?

Update: Some offers mentioned below are no longer available. View the current offers here.

The idea of earning free flights and hotel stays just by signing up for the right credit cards seems too good to be true, and there are plenty of myths about how it all works. When introducing someone to the world of reward travel, you may have to dispel some of those misconceptions.

One of the most common things people believe when they apply for new credit cards is that those actions will negatively and permanently impact their credit scores. While it is true that recklessly opening new lines of credit and abusing them (i.e., racking up large balances, carrying interest and missing payments) can hurt your credit score, there is no long-term impact on your score from simply opening new accounts.

Since credit card sign-up bonuses are the foundation of travel rewards, here's a look at how your credit score is affected when you open a new credit card.

How does applying for a credit card impact your credit score?

Even if you've researched and decided which card to start with, you should not apply for it until you understand how your credit score is calculated.

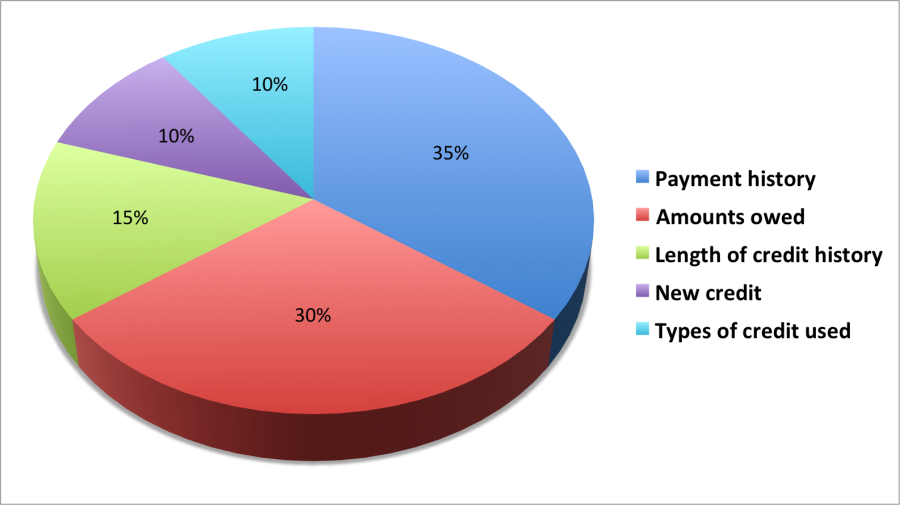

Here's a breakdown of the factors involved:

- Payment history (35%): It's no surprise that the category that carries the most weight is your on-time payment history.

- Amounts owed (30%): Also referred to as the utilization rate, this is the total balance on all your credit cards divided by your total credit limit.

- Length of credit history (15%): Also known as the average age of accounts, the longer your credit history, the higher your score will be.

- Credit mix (10%): This refers to the various lines of credit you may have, including credit cards, student loans, a car loan and a mortgage.

- New credit (10%): New inquiries on your credit report account for 10% of your score.

Related: How credit scores work

How can applying for a credit card hurt your credit score?

Hard inquiries vs. soft inquiries

Your credit will likely be checked dozens of times throughout your life, whether you're applying for a credit card or starting a new job. There are two different types of inquiries, and it's important to understand the difference.

Hard inquiries are times when your credit is checked in connection with an application for a new line of credit, such as a credit card or loan. These inquiries get reported to the credit bureaus and are the ones that appear on your credit report — and ultimately affect your score.

A soft inquiry would be checking your credit report (to determine whether you were under 5/24 with Chase, for example) or letting your employer check your credit as part of the hiring process. Soft inquiries are not reported to the credit bureaus and won't impact your score in any way.

Related: TPG reader credit card question: Is the Chase 5/24 rule based on inquiries or new accounts?

How do hard inquiries affect your credit score?

Almost every time you apply for a credit card, you will receive a hard inquiry on your credit report. Some exceptions exist — for example, American Express often does not inquire about existing customers until the new application is approved. While the exact impact may vary from case to case, generally speaking, you can expect your score to drop by about five points each time you apply for a new credit card.

This might seem scary if you've been working to improve your credit score for a long time, but it's important to remember that the exact number is rarely what banks look at when evaluating your application. They'll put you into a range, say, 700-750 — so if your score drops from 740 to 735, it is unlikely to affect future approval odds.

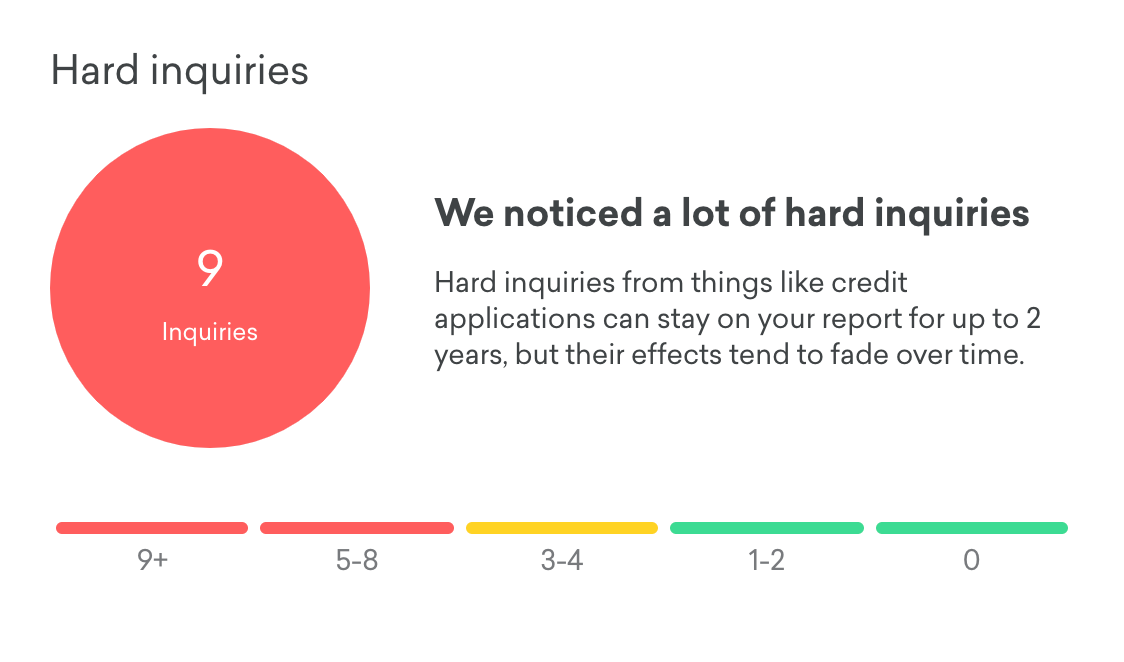

Too many recent hard inquiries can drag down your score. Credit Karma says your score starts to be affected with three to four recent inquiries, especially once you get above five. The inquiry will stay on your credit report for up to two years, but the impact fades over time. If you see a jump in your credit score one month that's not linked to any obvious event, such as paying off a balance, it may be the effect of your inquiries fading in relevance.

Related: What is the difference between a hard and soft pull on your credit report?

How can applying for a credit card help your credit score?

While the hard inquiry might lower your credit score in the short term, opening a new credit line can help you increase it in the long run. It provides another opportunity to pay your bills in full and on time, which will help your payment history as it's calculated into your credit score. It also increases your available credit, meaning you can more easily keep your credit utilization rate low.

Plus, if you leave the credit line open, you can increase the length of your credit history over time. As long as you use the new credit card responsibly and follow our 10 commandments of credit card rewards, the new card can ultimately help your credit score.

Related: 6 things to do to improve your credit score

Bottom line

A crucial step in becoming comfortable applying for credit cards is learning about the factors that affect your credit score and knowing that an application has a minimal impact on your score. A five-point drop is a small price if it helps you unlock a sign-up bonus worth $1,000 or more in free travel.

Remember that the drop is only temporary. The effect of the inquiry will fade over the course of two years, but in the long term, you can also boost your score by continuing your history of on-time payments and increasing the average age of your credit accounts.

Related: The best credit cards of the month