Does canceling a credit card hurt your credit?

Update: Some offers mentioned below are no longer available. View the current offers here.

At TPG, we spend an incredible amount of time discussing which credit cards you should open, which cards pair well together and even how to build an overarching credit card strategy. An equally important topic that rarely gets as much attention is when — and why — you should consider closing your credit cards.

If you have credit cards you no longer find valuable, especially if they charge an annual fee, your first instinct may be to cancel them. Your strategy for closing cards deserves as much attention as your strategy for opening them because closing accounts can potentially affect your credit score.

Related: How do credit scores work?

Is It bad to close a credit card?

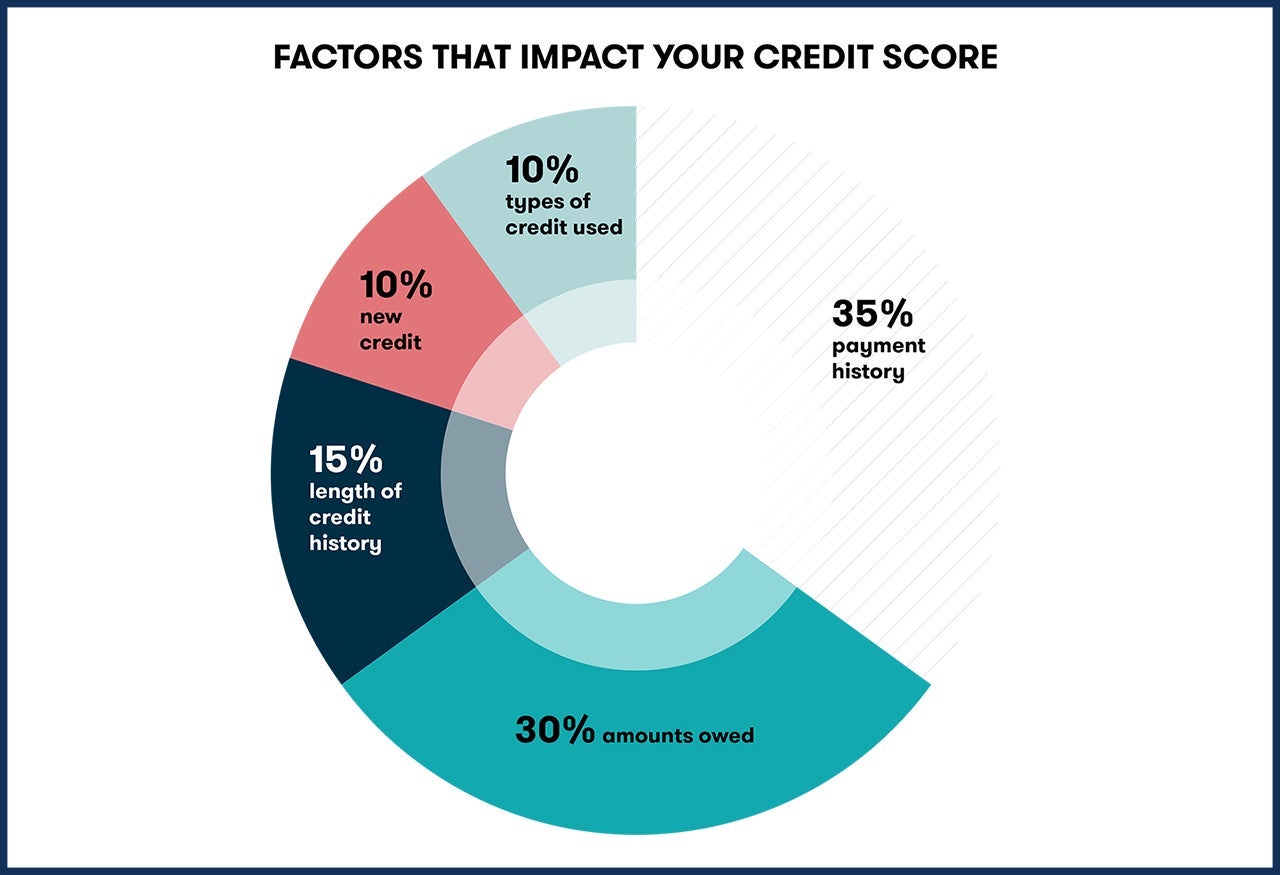

Does canceling a credit card hurt your credit, and does that make it bad to cancel a credit card? The answer may seem complex, but let's break it down. The main components of a credit score are:

- Payment history

- Amounts owed

- Length of credit history

- New credit

- Types of credit used

The two main factors affected when you close a credit card are your credit utilization and the length of your credit history.

Your credit utilization rate is the ratio of how much of your total available credit across all credit cards you are using. The less credit you're using, the better your credit score. When you close a card account, particularly one with a high credit limit, the total available credit decreases, thus raising your credit utilization rate and consequently lowering your credit score.

Additionally, closing a credit card could harm your credit history length. FICO includes the age of your oldest and newest credit accounts, and the average age of all your accounts. If you close a credit card that's been open for several years and has a lengthy credit history, that could negatively affect the average age of your accounts. A decrease in the average age of your accounts would subsequently decrease your credit score.

It can be bad to close a credit card as it may affect your relationship with an issuer. American Express's card application pages include the following information related to welcome bonuses:

"We may also consider the number of American Express Cards you have opened and closed as well as other factors in deciding your welcome offer eligibility."

So, if Amex feels that an individual consistently opens credit cards and closes them, they may limit their eligibility to earn welcome bonuses in the future.

Related: How to check your credit score for free

How does canceling a credit card affect your credit score?

Once a credit card is closed, you effectively lower your total line of credit across all your cards, increasing your credit utilization ratio and decreasing your credit score. It can also lower the average age of your credit accounts, decreasing your credit score further.

An example is if you have three credit cards: two have $5,000 limits, and one has a $10,000 limit. Canceling the credit card with a $10,000 limit would be more detrimental to your credit score as you drop your total available credit to $10,000 from $20,000. A 50% decrease in your available credit will surely increase your credit utilization rate and negatively affect your credit score.

A high credit utilization shows issuers heavy borrowing, which, to them, could be a sign of financial distress, and this is why credit utilization affects 30% of your FICO score.

Canceling a credit card could hurt your credit score based on the age of the closed card. Closing a credit card won't immediately affect your length of credit history (worth 15% of your FICO Score) by lowering your average credit age. Even after you close a positive account, it may remain on your credit for up to 10 years. But after that, it could decrease your score.

Related: What is a good credit score?

Should I close my credit card?

This might seem obvious, but you should only close a credit card if you're spending more on annual fees than you're getting in return.

Cards such as the Marriott Bonvoy Brilliant® American Express® Card with an annual fee of $650 (see rates and fees) are those that I get much more in value than the annual fee. I get up to $300 in annual statement credits on eligible worldwide restaurant purchases and an up to 85,000-point annual free night award valid at hotels participating in the Marriott Bonvoy program. (Certain hotels have resort fees.) This card is in my long-term "keep" pile. If I were to stop traveling and lose my Marriott elite status, I might change my mind.

If your card doesn't have an annual fee, you should keep it open even if you don't use it that often to preserve (and potentially even strengthen) your credit score over time. If it doesn't cost you anything to keep a card open, you shouldn't close it. It would be bad to close a credit card that costs you nothing annually, as it would hurt your credit score. However, you should make a small purchase on it at least once every six months so it doesn't get closed due to inactivity.

If you have several credit cards open with annual fees that are becoming a burden on your finances despite the benefits they offer, carefully consider which cards are valuable and useful to you and which cards you wouldn't mind departing with. It's also important to consider the credit limits on each card and how long your account has been open when deciding which cards to cancel.

Related: How to decide if a credit card's annual fee is worth paying

How to close credit cards safely

If you choose to close a credit card, here are some steps to ensure it is closed properly.

Create an exit plan

Planning an exit strategy involves taking systematic steps to cancel a credit card while keeping two main objectives in mind: safeguarding your credit score and preserving your rewards. It's important to avoid damaging your credit score by simply closing cards and to ensure you don't lose any accumulated points or miles.

Safeguard your rewards

When closing a credit card, it's crucial to prevent any loss of rewards that may be left in that account. If you're not ready to utilize the points, consider transferring them to an airline or hotel partner or a family member's account. Alternatively, you can use them to purchase gift cards, redeem them for cash or apply them as statement credits.

Clear the balance

If you're familiar with our travel rewards credit card commandments, you're likely aware of the importance of settling outstanding payments before canceling a card. Verify that your final payment has been successfully processed before canceling.

Terminate recurring payments

Once you've decided to cancel a credit card, ensure that you remove it as the designated payment method for any recurring bills. You can do this by visiting the respective company's website or contacting them directly to update your payment details.

Cancel the card

You can cancel your card by secure message or phone by contacting your card issuer. You should also get written confirmation that you have a zero balance.

Safely dispose of your old card

After successfully canceling your credit card, it's wise to dispose of it properly to prevent potential misuse. Taking this precautionary step will help ensure that nobody attempts to use the card once it has been closed.

Review your credit report

After closing the card, reviewing your credit report once more is always a good idea. According to regulations, you are entitled to receive a complete credit report from the three major credit bureaus (Experian, Equifax and TransUnion) free of charge once a week. To obtain your comprehensive reports, visit the annual credit report website and click the "Request your free credit reports" button.

Related: Credit card fraud: How to spot and report it

Alternatives to canceling a card

Even if the math has shifted and you're no longer getting enough value to keep a card open (or you no longer want to pay the annual fee), there are a couple of things to consider before you close the account.

Downgrade to a no-annual-fee card

If your primary concern is not paying an annual fee, some issuers will let you downgrade or change your card to a version that doesn't have an annual fee. For example, you could downgrade a Chase Sapphire Reserve® (see rates and fees) to a no-annual-fee Chase Freedom Unlimited® (see rates and fees). You retain your line of credit and do not affect the average age of cards on your credit report.

However, each issuer has its own rules on product changes. With Chase, you must wait until the account is at least a year old. This strategy is also a little harder with cobranded airline and hotel credit cards, as you're generally only allowed to "product change" within the same family. For example, American Express offers a few no-annual-fee cards for you to choose from.

Ask for a retention offer

Suppose a credit card issuer gives you a welcome bonus of 50,000 points to open a new card. In that case, they'll want to keep your business, especially if you spend regularly on your card after that three-month introductory period. Even if you're 99% sure you want to cancel a credit card, it can't hurt to ask about the possibility of an annual fee waiver or a retention offer, which could result in receiving bonus miles after completing a spend requirement.

It seems crazy to think that a giant corporation will waive your fees simply because you ask, but it's entirely possible. All you have to do is threaten to walk away, and suddenly, a new limited-time offer might appear on your account. Many TPGers have used this strategy successfully many times, although it doesn't always work, and you certainly aren't entitled to anything.

When calling for a retention offer, you'll need to be explicit to ensure they understand what you're asking. I usually say something like, "I love X, Y and Z perks, but I'm just not sure I can justify paying the annual fee on this card for another year. I was wondering if there were any retention offers on my account or if getting an annual fee waiver might be possible."

You need to call in to cancel most credit cards anyway, so the extra couple of minutes spent asking this question are well worth the time.

Related: Quick Points: How to use retention offers for extra points and miles

Bottom line

Canceling a credit card is a big decision. There is a lot to consider before doing so, including considering how it would affect your credit score. There are cases when it makes sense to close a card, and while it is not bad to close a credit card, keep in mind it may hurt your credit to close a card, so weigh your options carefully as you might be better off simply downgrading or holding onto the card.

For rates and fees of the Marriott Bonvoy Brilliant, click here.