The Best Investment Apps for 2019

Gone are the days of having to take care of important financial business over the phone or in a face-to-face meeting. Thanks to a slew of helpful apps, you can manage your investment strategy right on your smartphone.

Have you been letting your retirement investment goals sit on the back burner because of a busy schedule? The popular investment apps below may take away that excuse. In fact, some of these apps are so easy to use, they can almost put your investment strategy on autopilot.

Here we take a look at the pros and cons of five investment apps to help you find the perfect tool to simplify your retirement plan.

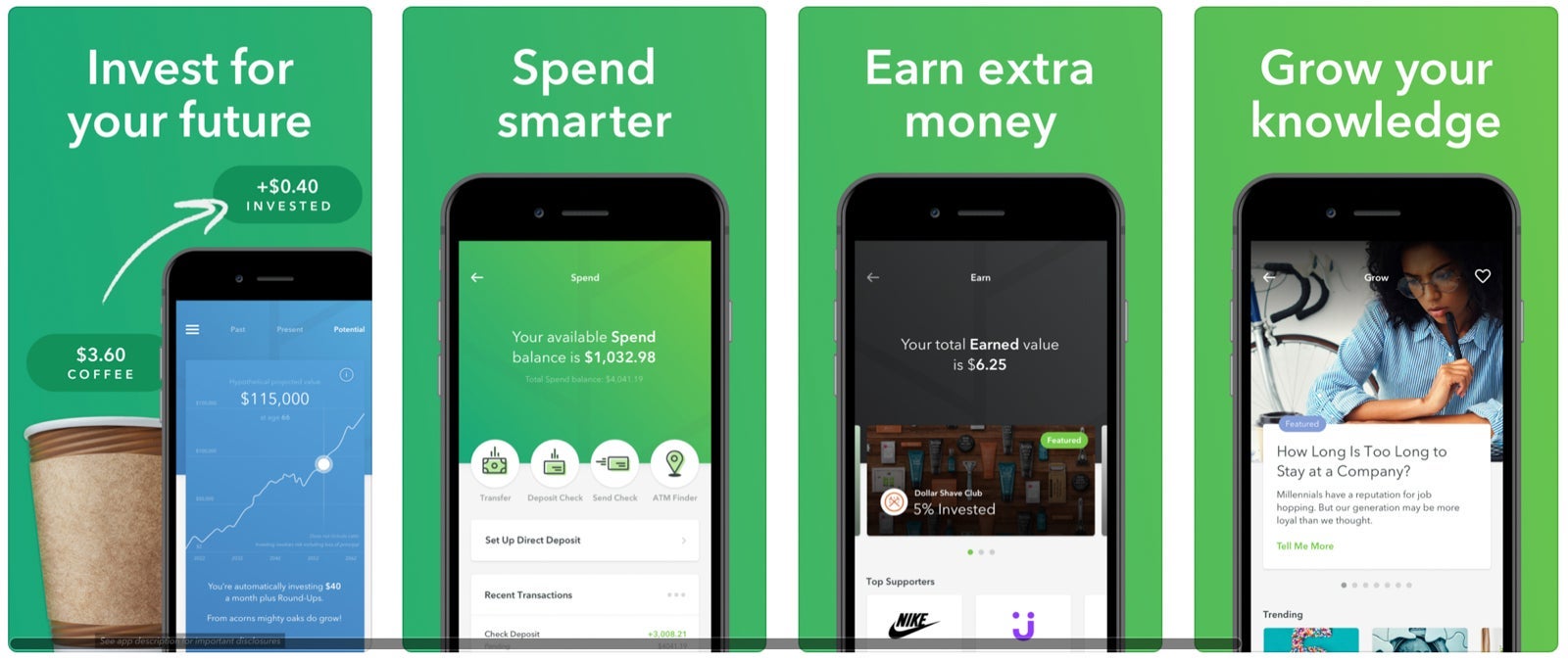

Acorns

Are you new to the world of investing or retirement savings? If so, Acorns offers a simple solution to help you get started.

Acorns allows you a unique way to save toward your goals by rounding purchases from your debit and credit cards to the next dollar amount. The app then invests the "extra change" for you based on the preferences you set up. The money is redirected toward an investment portfolio that matches risk with your comfort level.

Logan Allec, CPA and owner of Money Done Right, likes investment apps like Acorn because "apps make investing simple and easy for young people in ways that traditional brokerage accounts don't."

Acorns in particular can work great for younger workers with higher levels of debt. Allec explains, "It might be unrealistic to ask a 25-year-old making $40,000 a year with $32,000 of student loan debt to deposit an extra $100 a month into to a traditional brokerage account. But can she invest the spare change left over from her morning coffee? Yup! And just like that, she's a stock market investor without even trying."

What you might like:

Here are some of the advantages of using Acorns to manage your savings and investment goals:

- Low fees ($1-$3 per month)

- Free for college students (valid .edu email required)

- Automatically save and invest (just link your credit and debit cards to the app)

- $0 account minimum

What you might not like:

There's isn't much not to like about Acorns. The app, however, might not be a good fit if you're currently sitting on a bunch of credit card debt.

Although Acorns may only have you investing pennies on every purchase you make, if you aren't paying your credit card balance off in full each month, you will be charged interest on those round-ups.

If you decide to use Acorns, you probably shouldn't connect any credit card accounts to the app until you've gotten a handle on paying off your credit cards in full each month.

Want to learn more about how the Acorns app works? Check out this review.

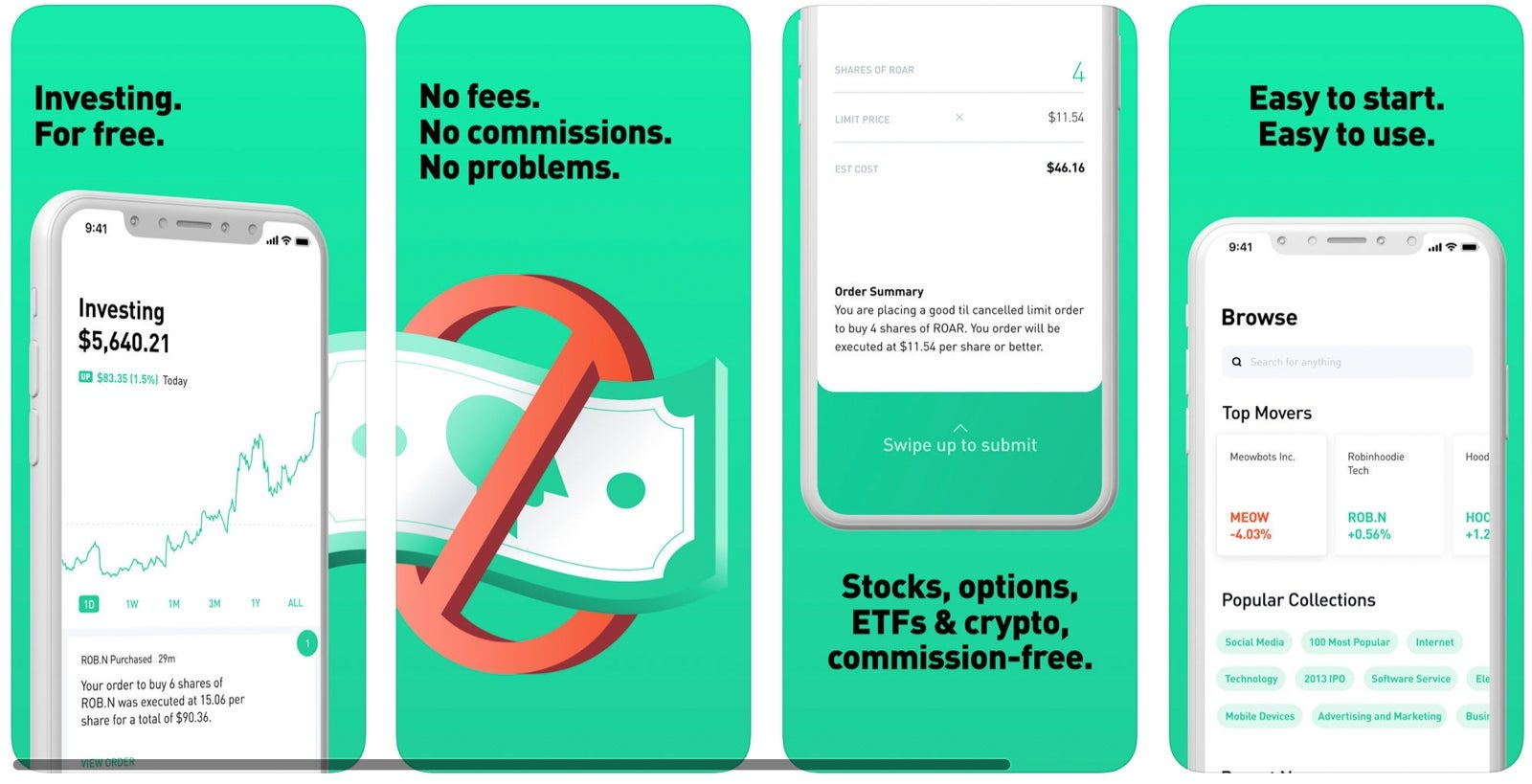

Robinhood

Does the idea of free investing appeal to you? If so, Robinhood might be right up your alley.

What you might like:

Here are some of the other features of the Robinhood app you might appreciate:

- No commissions or trade fees

- Features tools for newcomers and advanced traders

What you might not like:

Robinhood won't give you access to a full range of investments like mutual funds. Instead, your choices will be limited to Exchange-traded funds (ETFs), stocks, options and cryptocurrencies.

Kyle Kroeger, former investment banker and Founder of MillionaireMob.com, believes the app is a useful tool. Kroeger, who writes about investing on a daily basis, recommends combining the Robinhood app with M1 Finance (more on that below).

"I think people should use both, not one or the other," Kroeger says. "Both apps are completely free and have slick, easy-to-use interfaces. I recommend that users turn to Robinhood for an actively managed portfolio of stocks and M1 Finance for long-term investing and retirement accounts."

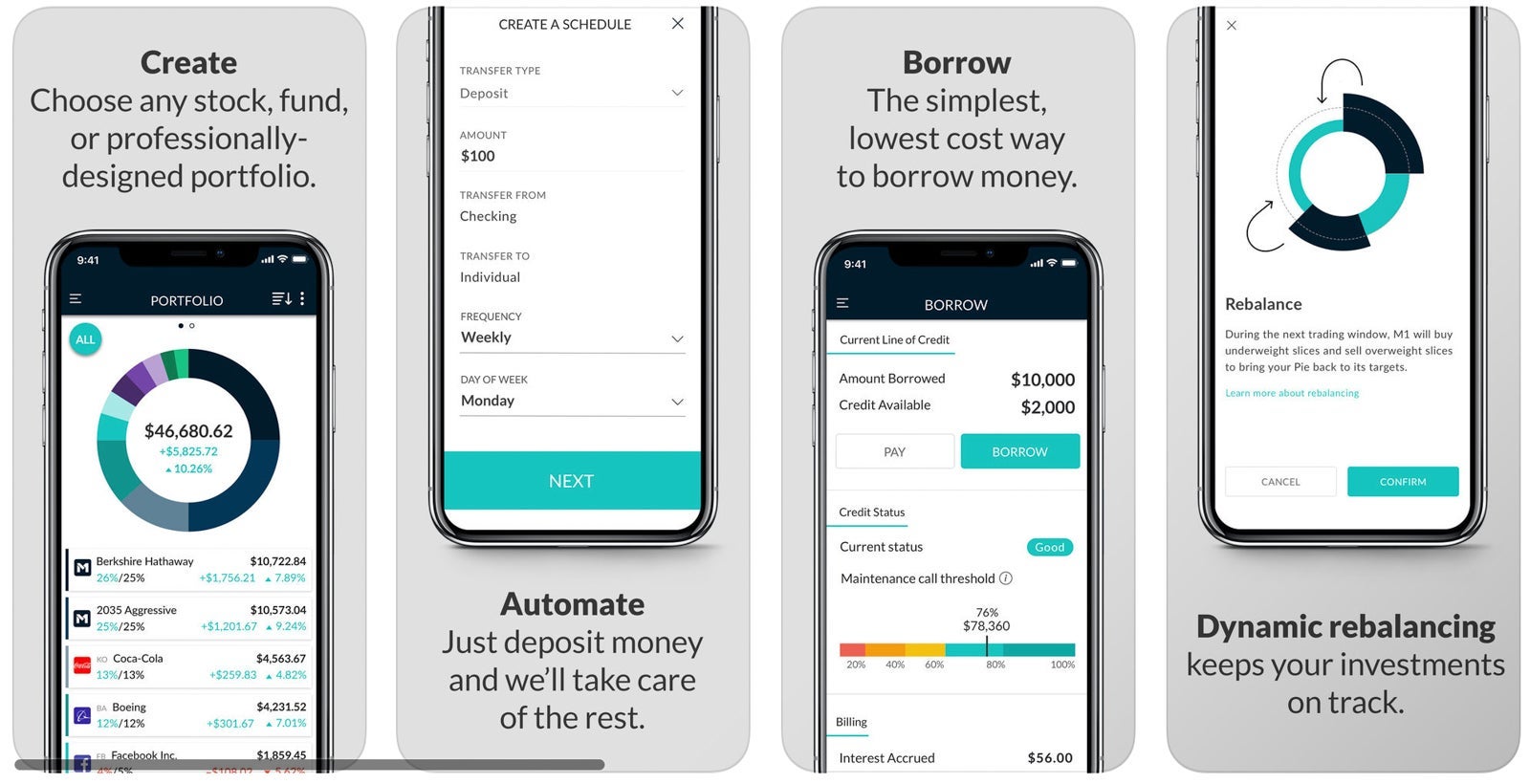

M1 Finance

Jon Dulin, Personal Finance Expert at MoneySmartGuides.com, is a big fan of the M1 Finance app. Dulin explains, "M1 Finance lets me build a completely customized stock dividend portfolio and buy fractional shares, all at zero cost to me. The app shows me everything I need at a glance. I don't waste time searching."

What you might like:

M1 Finance has a number of appealing features, including:

- Commission-free investing

- Automatic deposits

- Easy tax reporting (integrates with H & R Block and TurboTax)

- Free consultation with a product specialist

What you might not like:

If you're interested in tax loss harvesting, M1 doesn't offer this feature. Tax loss harvesting occurs when you sell a stock or fund at a loss and then purchase a similar stock or fund in exchange. The result is that your portfolio mix doesn't undergo much change. Any losses you incur can be used as a write off to offset investment gains (and up to $3,000 of your standard income).

However, M1 does feature include a "tax minimization" feature which aims to help users reduce the amount of taxes they owe when they sell securities.

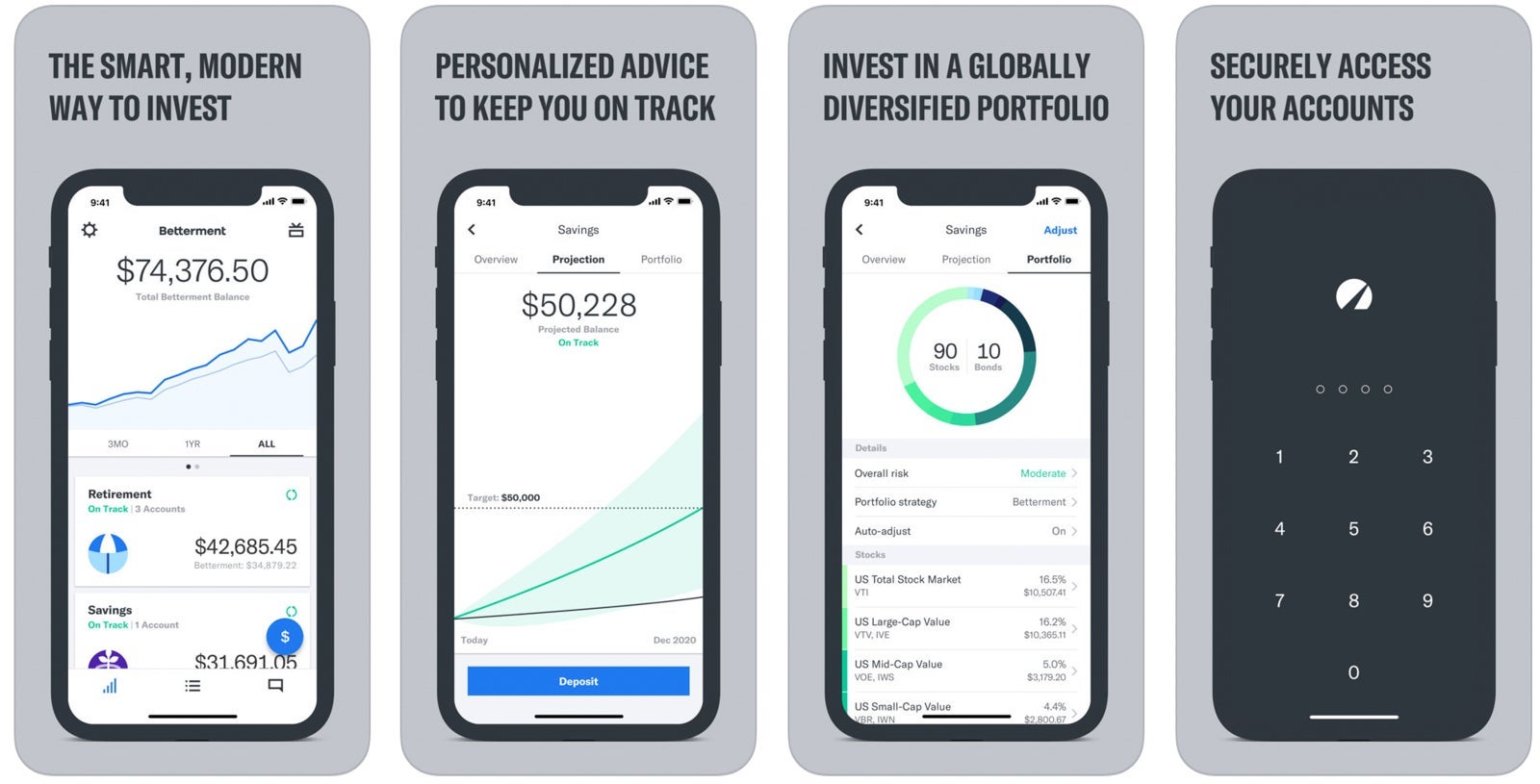

Betterment

Riley Adams, licensed CPA and Founder of Young and the Invested, personally uses Betterment to manage his investment objectives.

"A year ago, I changed from Vanguard to Betterment, a robo-advisor. Betterment uses scientific research to optimize which ETFs you hold based on your investing objectives. Additionally, the service automatically rebalances your holdings across time as you make contributions, take withdrawals or near your investing objectives," he said.

Betterment offers tax-efficient investing strategies to minimize the amount of taxes you pay on realized gains, he added. If your accounts aren't tax-advantaged (e.g., 401(k) or IRA), harvesting these tax losses can increase your returns by minimizing your capital gains each year.

What you might like:

Here are a few of Betterment's popular features:

- Commission-free investing

- Automatic deposits

- Customized experience (e.g. new investor, hands-off investor or hands-on investor)

What you might not like:

If you're trying to find a fee-free investing option, Betterment isn't it. Annual fees for the service range from 0.25% — 0.40% of your account balance.

Do you want to save money on investment fees, but you prefer a little guidance along the way? As a robo-advisor, Betterment can represent a nice hybrid between do-it-yourself investing and hiring a financial planner.

Mint

Mint doesn't quite qualify as an investment app. It can help you monitor your investments, though, so it's worth mentioning.

Money Coach Cody Berman of FlyToFI.com says that, in addition to tracking investments, Mint is one of his favorite budgeting apps. "The software automatically captures my spending data and displays it in an easy-to-digest manner. Budgeting has never been easier."

What you might like:

Here are a few features of Mint that you might appreciate:

- Free account

- Managing your investment portfolio and finances in one app

- Asset allocation tracking across all your investment accounts (IRAs, 401(k)s, mutual funds, brokerage accounts, etc.)

- Identifying unnecessary investment fees you're paying

What you might not like:

Mint does not facilitate investing or stock trading itself. While the app will offer you some basic investment recommendations, it's more of a tracking tool to monitor your overall financial picture in one location.

Should you trust investment management to an app?

Successfully investing your money for retirement is an important goal to achieve. When you retire, you don't want to have free time without any money to make the best of it.

Yet the truth is that investing can be risky as well. Investing doesn't come with a manual. There are no guarantees and there are many aspects of the process which are out of your control.

Still, there are some things you can control. You can control whether you want to pay a professional to guide you and manage your investments. Or, you can choose to minimize investment fees and take a do-it-yourself approach.

So how do you decide?

According to the US Securities and Exchange Commission says if you're the type of person who will read as much as possible about potential investments and ask questions, you might not need investment advice. If, on the other hand, you're busy with your job, family or just life in general and feel uncomfortable investing on your own, professional help might be your best choice.

Here's the bottom line. Only you can decide which option is best for you. If you're ready to give investing on your own a try, one of the apps above might make the process a lot easier to manage.

TPG featured card

at American Express's secure site

Terms & restrictions apply. See rates & fees.

| 4X | Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 4X | Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 5X | New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App. |

| 3X | Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines. |

| 2X | Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com. |

| 1X | Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases. |

Pros

- Valuable dining and food-related credits

- Flexible rewards with airline and hotel transfer partners

- Multiple travel and purchase protections

- No foreign transaction fees

- Access to Amex Offers for additional savings (enrollment required)

Cons

- Not as useful for those living outside the U.S.

- Some may have trouble using Uber and other dining credits

- You may be eligible for as high as 100,000 Membership Rewards® Points after you spend $8,000 in eligible purchases on your new Card in your first 6 months of Card Membership. Welcome offers vary and you may not be eligible for an offer. Apply to know if you’re approved and find out your exact welcome offer amount – all with no credit score impact. If you’re approved and choose to accept the Card, your score may be impacted.

- Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year.

- Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year.

- New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App.

- Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines.

- Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com.

- Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases.

- Pay It® lets you tap in the American Express® App to quickly pay for small purchase amounts throughout the month and still earn rewards the way you usually do. Plan It® gives you the option to split up big purchases into equal monthly payments with a fixed fee. You’ll know upfront exactly how much you’ll pay.

- Updated! $120 Dining Credit: Earn up to a total of $10 in statement credits monthly when you pay with the Gold Card at Grubhub (including Seamless), Buffalo Wild Wings, Five Guys, The Cheesecake Factory, and Wonder. This can be an annual savings of up to $120. Enrollment required.

- $100 Resy Credit: Get up to $100 in statement credits each calendar year at over 10,000 qualifying U.S. Resy restaurants after you pay for eligible purchases with the American Express® Gold Card. That’s up to $50 in statement credits semi-annually. Enrollment required.

- $84 Dunkin' Credit: Earn up to $7 in monthly statement credits after you pay with the American Express® Gold Card at U.S. Dunkin’ locations. Enrollment required.

- $120 Uber Cash on Gold: Enjoy up to $120 in Uber Cash annually with your Gold Card. Just add your Card to your Uber account and you'll get $10 in Uber Cash each month to use on orders and rides in the U.S. when you select an Amex Card for your transaction.

- New! As an American Express® Gold Card Member, you can enjoy complimentary Hertz Five Star® Status. Enjoy benefits like skipping the counter at select locations, adding an additional driver at no additional cost*, and vehicle upgrades**. Benefit enrollment and Hertz Gold+ registration are required. *Additional drivers must meet standard rental qualifications and must be a spouse or domestic partner to qualify as complimentary. Other additional drivers subject to fees. **Benefits are subject to availability and vary by location. Additional Hertz program Terms and Conditions including age restrictions apply.

- Take advantage of a $100 credit towards eligible charges* at over 1,300 upscale hotels worldwide when you book The Hotel Collection through AmexTravel.com or the Amex Travel App **. *Eligible charges vary by property. **The Hotel Collection requires a two-night minimum stay.

- Book your travel through the Amex Travel App with added peace of mind – backed by American Express® service and support. Only for American Express® Card Members.

- Whenever you need us, we're here. Our Member Services team will ensure you are taken care of. From lost Card replacement to statement questions, we are available to help 24/7.

- No Foreign Transaction Fees.

- Annual Fee is $325.

- Terms Apply.