After more than 16 years, why the Chase Sapphire Preferred should still be your first rewards card

Update: Some offers mentioned below are no longer available. View the current offers here.

I've been in the world of points and miles for a long time, and I've been asked more times than I can count which rewards credit card travelers should get first.

My answer is almost always the same: Chase Sapphire Preferred® Card (see [rates and fees]).

The Sapphire Preferred has been around for over 16 years, but that doesn't mean it is stale. In fact, it just got a refresh that made it an even stronger card to start with while retaining a low $95 annual fee.

Plus, for a limited time, the Sapphire Preferred is offering 100,000 bonus points after spending $5,000 on purchases in the first three months from account opening.

Can you think of anything that has kept the same price for over 16 years yet added even more value? Because I can't.

Getting started can be the biggest, scariest step. So if that's where you are in your rewards travel journey, here are five reasons why the Chase Sapphire Preferred is still the card I most frequently recommend to my own friends and family members.

Earn 100,000 valuable bonus points quickly

I promise I'm not starting here just because there's a limited-time offer. But it would be silly to start anywhere else, because rewards are only fun if you actually have points to use.

And the fastest way to build a meaningful points balance is with a strong welcome bonus. Right now, for just the third time ever, the Chase Sapphire

To earn that bonus, you'd need to charge an average of $1,667 to the card each month for three months, which may sound like a lot at first.

But remember that everyday expenses count. Groceries, gas, cellphone bills, insurance premiums, medical expenses and even some utility payments can all help you reach the spending requirement. Those routine purchases can add up surprisingly quickly and unlock a welcome bonus that TPG values at more than $2,000 based on our June 2026 valuations.

Limited-time offer on the Chase Sapphire Preferred: Earn 100,000 bonus points after spending $5,000 on purchases in the first three months from account opening.

Get award points that are easy to use

Let's talk about what makes the Chase Sapphire Preferred especially beginner-friendly: the easy-to-use points.

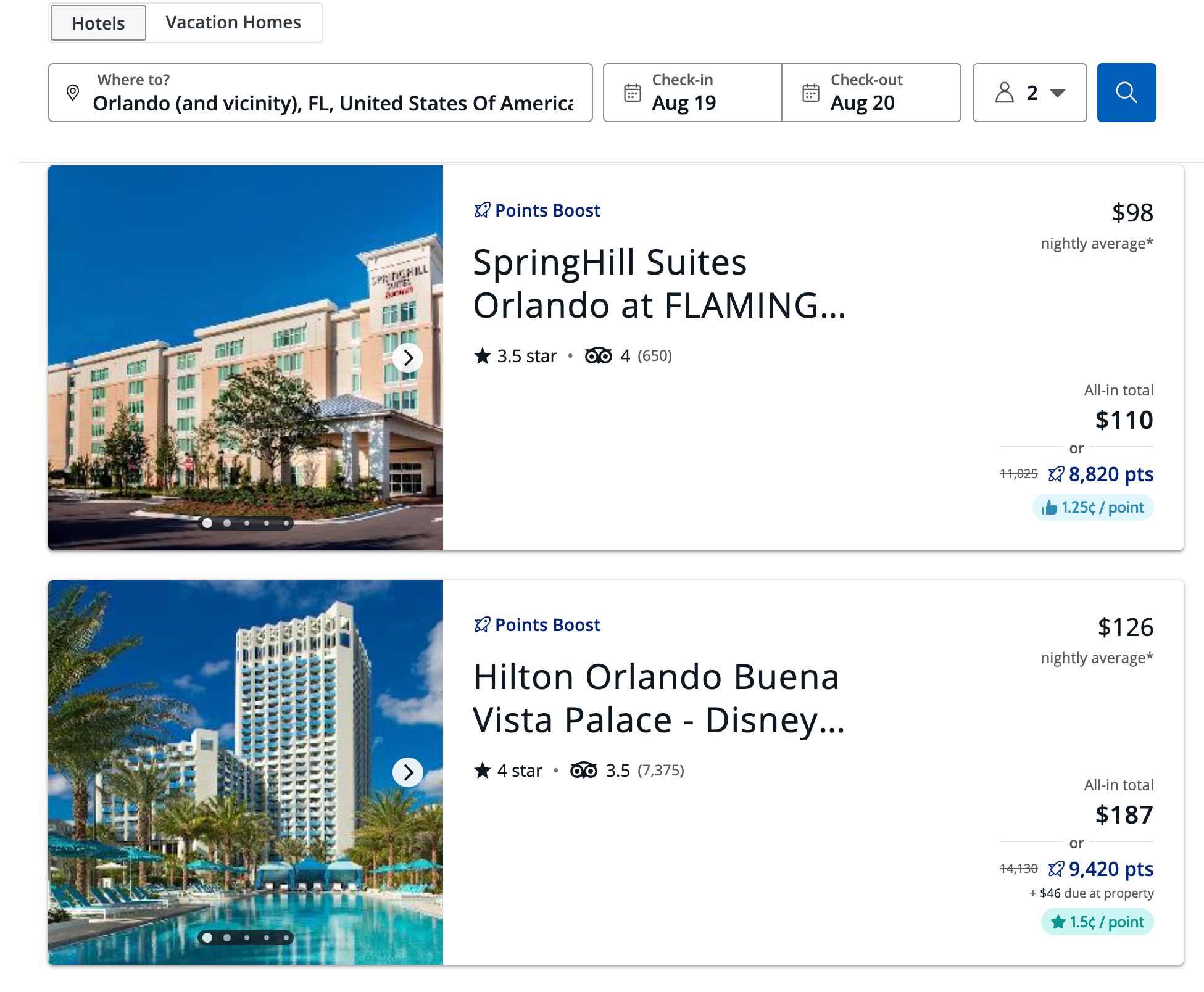

Use the points for up to $1,500 in flights and hotels via Chase Travel

There are two main ways to use Chase Ultimate Rewards points for travel, and the easiest option is booking directly through Chase Travel℠.

If you know how to book a trip through Expedia or another online travel agency, you already know how to use Chase Travel. You can search for and book flights, hotels, rental cars and more using either cash, points or a mix of both.

At a minimum, your points are worth 1 cent each toward travel booked this way. However, select hotels and flights and experiences qualify for Chase's Points Boost feature, which can increase the value of your points to as much as 1.5 cents each.

That means the current 100,000-point welcome bonus could be worth up to $1,500 in travel booked through Chase Travel.

Or, stretch your points even further with transfer partners

If you're willing to learn a few more rewards redemption tricks, you can potentially get even more value by transferring your Chase points to one of Chase's 14 airline or hotel partners.

You can transfer points to programs such as United MileagePlus, JetBlue TrueBlue and Air France-KLM Flying Blue for flights, or World of Hyatt or Marriott Bonvoy for hotel stays, to name a few. Depending on how you redeem them, 100,000 points can go a surprisingly long way — whether that's several domestic flights, a few nights at a resort or even a business-class flight to another continent.

Admittedly, using transfer partners requires a little more research than booking through Chase Travel. But that's part of what makes Chase Ultimate Rewards points so appealing: You can keep things simple, or you can unlock even more value as your confidence and curiosity grow.

The current Chase transfer partners are:

- Aer Lingus AerClub

- Air Canada Aeroplan

- Air France-KLM Flying Blue

- British Airways Club

- Emirates Skywards

- IHG One Rewards

- Iberia Club

- JetBlue TrueBlue

- Marriott Bonvoy

- Singapore KrisFlyer

- Southwest Rapid Rewards

- United MileagePlus

- Virgin Atlantic Flying Club

- World of Hyatt

Chase Ultimate Rewards points on the Sapphire Preferred transfer to these partners at a 1:1 ratio (except Hyatt, which is 4:3) but sometimes go higher with occasional transfer bonuses.

This means that 100,000 Chase Ultimate Rewards points could become the equivalent of 100,000 United miles, Aeroplan points, Marriott points and the list goes on. This is valuable flexibility rather than being locked into earning and redeeming with one loyalty program.

The annual fee is low, and it has lots of valuable perks

Premium travel rewards cards can absolutely be worth their annual fees. But for someone just getting started, it's understandable to hesitate before signing up for a card that costs $795 or even $895 per year.

That's another reason the Sapphire Preferred is such a compelling place to start. Its annual fee is just $95, yet it still offers valuable travel perks and rewards that can easily justify that cost.

Some perks can quickly more than offset the annual fee.

For example, there's now a $100 annual Chase Travel hotel credit that can more than offset the $95 annual fee if you use it. Cardholders can also receive an application fee credit worth up to $120 for Global Entry, TSA PreCheck or Nexus once every four years.

Additional Sapphire Preferred benefits include:

- Complimentary Apple TV and Apple Music subscriptions for one year (enrollment required through Chase Benefits & Rewards by Dec. 31, 2026)

- Strong travel protections, including trip cancellation and interruption insurance, trip delay reimbursement, and emergency evacuation and transportation coverage

- Complimentary DoorDash DashPass membership (activation required through Dec. 31, 2027)

- Up to $10 in monthly DoorDash credits for eligible nonrestaurant orders through Dec. 31, 2027

The Sapphire Preferred strikes a sweet spot by delivering meaningful travel and other benefits without a yearly commitment to a pricier premium card.

Related: The 8 best credit cards with annual fees under $100

Earn points quickly

A great welcome bonus like the one available now can get you started, but the best rewards cards continue delivering value long after you've earned that initial pile of points.

That's another area where the Sapphire Preferred shines.

The card offers strong earning rates across a variety of everyday spending categories — some of which even rival or outperform cards with much higher annual fees.

- 5 points per dollar spent on travel booked through Chase Travel

- 5 points per dollar spent on Lyft rides (through Sept. 30, 2027)

- 5 points per dollar spent on eligible Peloton equipment and accessory purchases over $150 (through Dec. 31, 2027)

- 3 points per dollar spent on dining

- 3 points per dollar spent on gas purchases and electric vehicle charging

- 3 points per dollar spent on select streaming services

- 3 points per dollar spent on online grocery store purchases (excludes Target, Walmart and wholesale clubs)

- 3 points per dollar spent on vacation homes at brands such as: Airbnb, Vrbo, Plum Guide, HomeAway, Homestay.com and Vacasa

- 2 points per dollar spent on all other travel

- 1 point per dollar spent on everything else

What I especially appreciate is that the categories are broad enough to capture how many people really spend their money. For example, travel includes everything from plane tickets and hotels to subway passes and even some parking garages. Dining includes everything from high-end restaurants to fast food and DoorDash delivery services.

Since these points are worth 2.05 cents each (according to TPG's June 2026 valuations), you are getting anywhere from 2.05 to 10.25 cents in value per dollar charged to the card, depending on the category you're spending in.

Related: The power of the Chase Trifecta: Sapphire Reserve, Ink Preferred and Freedom Unlimited

It's easier to get approved when you are newer to rewards cards

Last but not least, there's a practical reason to start with the Sapphire Preferred. In short, Chase makes it easier to get Chase-issued credit cards before you get too far into your rewards credit card journey.

Chase has an unwritten but well-documented rule that it generally won't issue a new credit card account once you have opened five or more card accounts across all banks in the last 24 months. Informally, this is known as the Chase 5/24 rule.

That seems easy enough if you are used to only getting a new credit card once every few years, at most. However, once you get into credit card rewards, it can be easy to use up those slots as you get an airline card, a hotel card, etc.

I've seen plenty of travelers realize they want a Chase card after they've already filled up those five slots and are forced to wait before they can qualify.

Related: Here's who is eligible for a Chase Sapphire Preferred

Because of this restriction, it makes sense to start by getting a Chase card, like the Sapphire Preferred, as one of your first cards before you run into a wall with opening new Chase accounts for some time.

Related: The best ways to fill your 5/24 slots

Bottom line

When friends and family ask me where to start with earning points and miles in their everyday lives, my answer is almost always the same.

The Chase Sapphire Preferred is easy to use, flexible and rewarding. It earns valuable points, offers cardholders multiple ways to redeem them, comes with useful travel perks and — importantly — still costs just $95 per year. I can't think of much less that costs the same as it did 16 years ago.

And it certainly doesn't hurt that right now it is offering its highest-ever bonus of 100,000 points after meeting the spending requirement.

But even outside the big bonus, my advice would be the same. In my experience, the biggest mistake people make with travel rewards is thinking they need to do tons of research just to get started. The truth is, you don't need to know everything on Day 1. You just need to start earning points with a card that's flexible, affordable and rewarding.

The Chase Sapphire Preferred is exactly that. And 16 years after its debut, it remains one of the very best entry points into the world of points and miles.

To learn more, read our full review of the Chase Sapphire Preferred.

Limited-time offer: Earn 100,000 bonus points after spending $5,000 on purchases in the first three months from account opening with the Chase Sapphire Preferred Card.