Where Have All the Rewards Debit Cards Gone?

The travel rewards landscape is always shifting, and it's on us to shift with it in order to take advantage of the best opportunities for earning points and miles. Today, TPG Contributor Richard Kerr explains why one such opportunity is disappearing, but not quite gone yet.

Not long ago, award travelers had plenty of options for earning points and miles from both credit cards and rewards debit cards. However, debit options have become scarce, and the remaining debit rewards programs aren't nearly as rewarding as they used to be. In this post, I'll offer some insight into the changes within the banking industry that brought about the downfall of the rewards debit card, and cover the few options that still exist for those who can put them to good use.

The Durbin Amendment

Soon after the financial crisis of 2007-2010, the Obama administration asked for financial regulatory reform and large-scale changes, essentially directed at former "too big to fail" banks. From these solicitations emerged the Dodd-Frank Wall Street Reform and Consumer Protection Act. In the final days of the bill's approval process, Senator Richard Durbin of Illinois added an amendment that would limit debit card interchange fees, which are the swipe fees charged by a card-issuing bank to an acquiring bank for the acceptance of card-based transactions. In essence, merchants are charged by card issuers for the privilege of being able to accept your debit card.

Interchange fees are meant to cover the liability, overhead and transactional costs assumed by a card-issuing bank, though on debit transactions these fees had become huge sources of profit for any bank that offered checking accounts. Powerhouse corporations (such as Walmart) have enough influence with a bank to negotiate low fees in order to accept certain cards. Prior to the Durbin Amendment, a local shoe repair business either had to accept the bank's fee (cutting into profits or passing the cost on to consumers) or only accept cash from customers. The Durbin Amendment — which was very unpopular within the banking industry, as you can imagine — directed the Federal Reserve to cap interchange fees at rates that were ambiguously defined as "reasonable." The Fed settled on limiting interchange fees for debit transactions to 0.05% of the transaction amount plus 21 cents (plus another 1 cent if certain security criteria are met).

The amendment now also allows businesses to offer a discount to customers who pay with cash and enforce minimums for credit card transactions (since interchange fees eat up a large portion of small transactions).

Post-Legislation Effects

A PhD candidate's dissertation in Economics could be written on the effects of the Durbin Amendment. Here are some highlights from 10,000 feet:

1. Given how hastily the amendment was passed (and how ambiguously it was worded), the Federal Reserve's decision was heavily scrutinized. Several lawsuits, a reversal, a reinstatement of the original rate and (just this past January) a denial by the Supreme Court to hear the case have left the interchange fees capped at the original 0.05% plus 21 cents instituted by the Fed.

2. As with all new rules, businesses look for ways to circumvent or compensate to ensure the bottom line is unaffected. Before the Durbin Amendment, my research says Visa would charge 0.95% plus a 20-cent transaction fee per swipe. Because that fee has now dropped to 0.05% and 21 cents, the bank has no reason to incentivize you to use your debit card, and no reason to pay the cost of sustaining a rewards program. Cue the end of free checking, the beginning of increased checking account fees and the slow death of debit cards that earn points and miles.

3. Because the Durbin Amendment does not deal with credit card transactions, credit card fees have increased to compensate for the loss of revenue from debit cards. Interestingly, fees in the US are staggeringly high compared to most places in the world.

4. Prepaid debit cards and financial instruments are not regulated by the Durbin Amendment. We have seen a huge rise in these products in the marketplace, many of which have exorbitant (i.e., very profitable) fees.

5. One issue the Durbin Amendment failed to address is third-party processing companies that accept or decline your transaction and then send it to your bank, which then pays the merchant (minus fees). These processors often have opaque pricing models that charge well above the fees imposed by the issuing bank, and are perhaps as large a problem as interchange fees for small and medium businesses.

Today's Rewards Debit Cards

Despite the recent changes, a handful of rewards debit cards have persisted, and while they're not as lucrative as they used to be, they still offer a way to boost your loyalty account even for transactions that normally wouldn't earn points or miles. Here are the options:

UFB Direct Airline Rewards Checking — Earn 1 AAdvantage mile for every $3 spent at point-of-sale transactions. There is no minimum balance requirement and no monthly maintenance fee, so even though the earning rate is abysmal, having the option available won't cost you anything.

PayPal Business Debit MasterCard — Maybe the best of the bunch, this card earns 1% cash back for purchases made online or over the phone, or those that require a signature. There is no annual fee and no cap on rewards.

Hawaiian Airlines Visa Check Card from Bank of Hawaii — Possibly the worst of the already bad options, this card earns you 1 HawaiianMile for every $2 spent, capped at only 1,000 per month. There is a $3 monthly fee.

SunTrust Delta — This was once a great way to earn SkyMiles and avoid fees, but has now become a sad reminder of the glory days. This card is no longer available publicly, and will be largely devalued for existing cardholders beginning July 25, 2015. Earnings will be capped at 2,000 miles per 30-day period (4,000 miles for Signature Advantage members). The annual fee is increasing to $95, and regular members will earn 1 mile per $2 spent instead of per $1 spent.

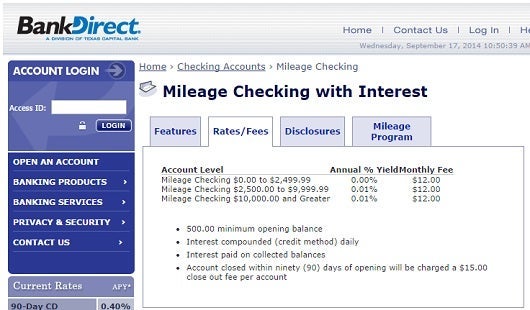

BankDirect AAdvantage Mileage Checking — There are sign-up bonuses available to those who open a new account — up to 26,000 miles for those who use direct deposit, online bill pay and the BankDirect debit card. Nevertheless, BankDirect now offers only 100 miles per month for every $1,000 on deposit up to $50,000, and 25 miles per $1,000 after that. There's also a $12 monthly fee, and at most 0.01% interest. Even if you have $50,000 to park somewhere, I think you can do better.

For what it's worth (which isn't much), several local and regional banks offer rewards checking accounts that earn a couple cents per transaction or a fixed rate of 1% on certain types of transactions.

Bottom Line

Even the less-than-stellar return offered by debit cards today can still be worthwhile to award travelers. First, I encourage us all to remember that credit cards are not for everyone. If you struggle with credit card debt, find it difficult to stick to a set budget, or have a low credit rating and can't get approved, then earning points, miles or cash back from a credit card shouldn't be your main strategy.

Secondly, many businesses are now passing credit card merchant fees on to consumers. If the savings of using a debit card outweighs the points or miles you would earn with a credit card, then go with the debit card. For example, you can pay your federal taxes with a credit card, but expect a fee of around 2% for the service. Unless you're earning rewards that offer a return of more than 2%, a debit card may be a better option. Finally, there are some purchases that simply can't be made with a credit card, so having a rewards debit card in your arsenal can help you earn rewards where you wouldn't be able to otherwise.

Though debit card earnings are small, this hobby is a marathon, and every little bit that you can add to your bottom line helps!

Do you use a rewards debit card?

[card card-name='Gold Delta SkyMiles® Credit Card from American Express' card-id='22034414' type='javascript' bullet-id='1']