Does switching credit card issuers affect your credit score?

Update: Some offers mentioned below are no longer available. View the current offers here.

Reader Questions are answered twice a week by TPG Senior Points & Miles Contributor Ethan Steinberg.

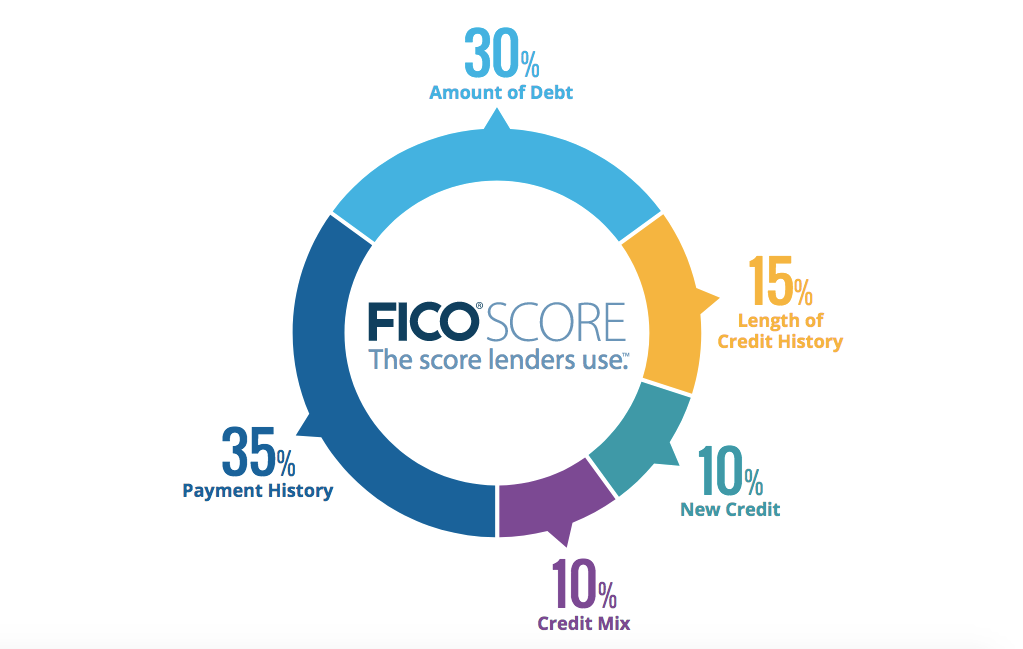

One of the most important factors that affect your credit score is the length of your credit history, which is why you want to be especially careful before closing any of your older cards as this could have an adverse effect on your score. TPG reader Billy wants to know if switching to a different issuer would impact his score ...

[pullquote source="TPG READER BILLY"]Hello I was wondering if switching card companies will hurt my credit score? I have been using Chase as my main issuer but am considering switching to Amex. Will my credit score crash by closing the significant amount of credit I have with Chase? [/pullquote]

For more TPG news delivered each morning to your inbox, sign up for our daily newsletter.

This is an interesting question, though it's one of just several things Billy needs to consider. First of all, your credit score doesn't change at all whether you use Chase, Amex, Citi, Capital One or someone else as your primary credit card issuer. Different types of cards, such as personal versus business or credit cards versus charge cards may report differently to the credit bureaus, but which issuer you use won't have any real impact.

However, the second half of Billy's question is much more important. Closing out an older credit card, especially one with a large limit, could really dent Billy's credit score. Not only would it decrease his average age of accounts, but it would also lower his total available credit making his utilization ratio skyrocket.

If he decides to switch to primarily using Amex cards, perhaps because the network of Membership Rewards transfer partners work better with his travel goals, here's what I would suggest doing to minimize the impact to his credit score:

- First, Billy should take his oldest Chase card and downgrade or product change it to a no-annual-fee product. If he primarily has Chase Ultimate Rewards earning cards he should pick either the Chase Freedom (No longer open to new applicants) or Chase Freedom Unlimited. Because these cards don't charge an annual fee, Billy can pick one to keep open forever. He doesn't need to use it regularly, just make a small charge every three to six months to keep the account from being closed.

- When Billy goes to close his other Chase cards, he should first ask to transfer his available credit lines to the Freedom or Freedom Unlimited so they don't get lost in the account closures.

The information for the Chase Freedom has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.

By taking these two simple steps, Billy can keep his oldest Chase card active and open forever and not lose any of his credit limits when he closes his other Chase cards, effectively mitigating the two biggest risks to his credit score.

Related: Chase cash-back showdown: Chase Freedom versus Chase Freedom Unlimited

Bottom line

Your credit score won't be affected by which issuer you use for your primary cards, but closing out old accounts and switching to a new bank could create some problems. Downgrading to a no-annual-fee card, consolidating your credit limits around that card and then continuing to keep that card open can help you make the switch without your credit score dipping.

Thanks for the question, Billy, and if you're a TPG reader who'd like us to answer a question of your own, tweet us @thepointsguy, message us on Facebook or email us at info@thepointsguy.com.

Featured photo by Popartic/Getty Images.

TPG featured card

at Capital One's secure site

Terms & restrictions apply. See rates & fees.

| 5X miles | Earn 5X miles on hotels, vacation rentals and rental cars booked through Capital One Travel |

| 2X miles | Earn unlimited 2X miles on every purchase, every day |

Pros

- Stellar welcome offer of 75,000 miles after spending $4,000 on purchases in the first three months from account opening. Plus, a $250 Capital One Travel credit to use in your first cardholder year upon account opening.

- You'll earn 2 miles per dollar on every purchase, which means you won't have to worry about memorizing bonus categories

- Rewards are versatile and can be redeemed for a statement credit or transferred to Capital One’s transfer partners

Cons

- Highest bonus-earning categories only on travel booked via Capital One Travel

- LIMITED-TIME OFFER: Enjoy $250 to use on Capital One Travel in your first cardholder year, plus earn 75,000 bonus miles once you spend $4,000 on purchases within the first 3 months from account opening - that’s equal to $1,000 in travel

- Earn unlimited 2X miles on every purchase, every day

- Earn 5X miles on hotels, vacation rentals and rental cars booked through Capital One Travel

- Miles won't expire for the life of the account and there's no limit to how many you can earn

- Receive up to a $120 credit for Global Entry or TSA PreCheck®

- Use your miles to get reimbursed for any travel purchase—or redeem by booking a trip through Capital One Travel

- Enjoy a $50 experience credit and other premium benefits with every hotel and vacation rental booked from the Lifestyle Collection

- Transfer your miles to your choice of 15+ travel loyalty programs

- Top rated mobile app