Chase Eliminates Price Protection and Return Protection on Yet Another Card

Update: Some offers mentioned below are no longer available. View the current offers here.

After years of offering a full range of generous benefits, it seems that credit card issuers are currently engaged in a "race to the bottom" when it comes to secondary credit card benefits.

It started in early April with an announced cutback to Citi's generous Citi Rewind purchase protection, which goes into effect July 28. Next came the news of Chase eliminating price protection and return protection on its United Explorer Card which went into effect June 1. The next shoe to drop was the announced elimination of price protection and cutbacks to points earning and lounge benefits on the Chase Sapphire Reserve, effective August 26.

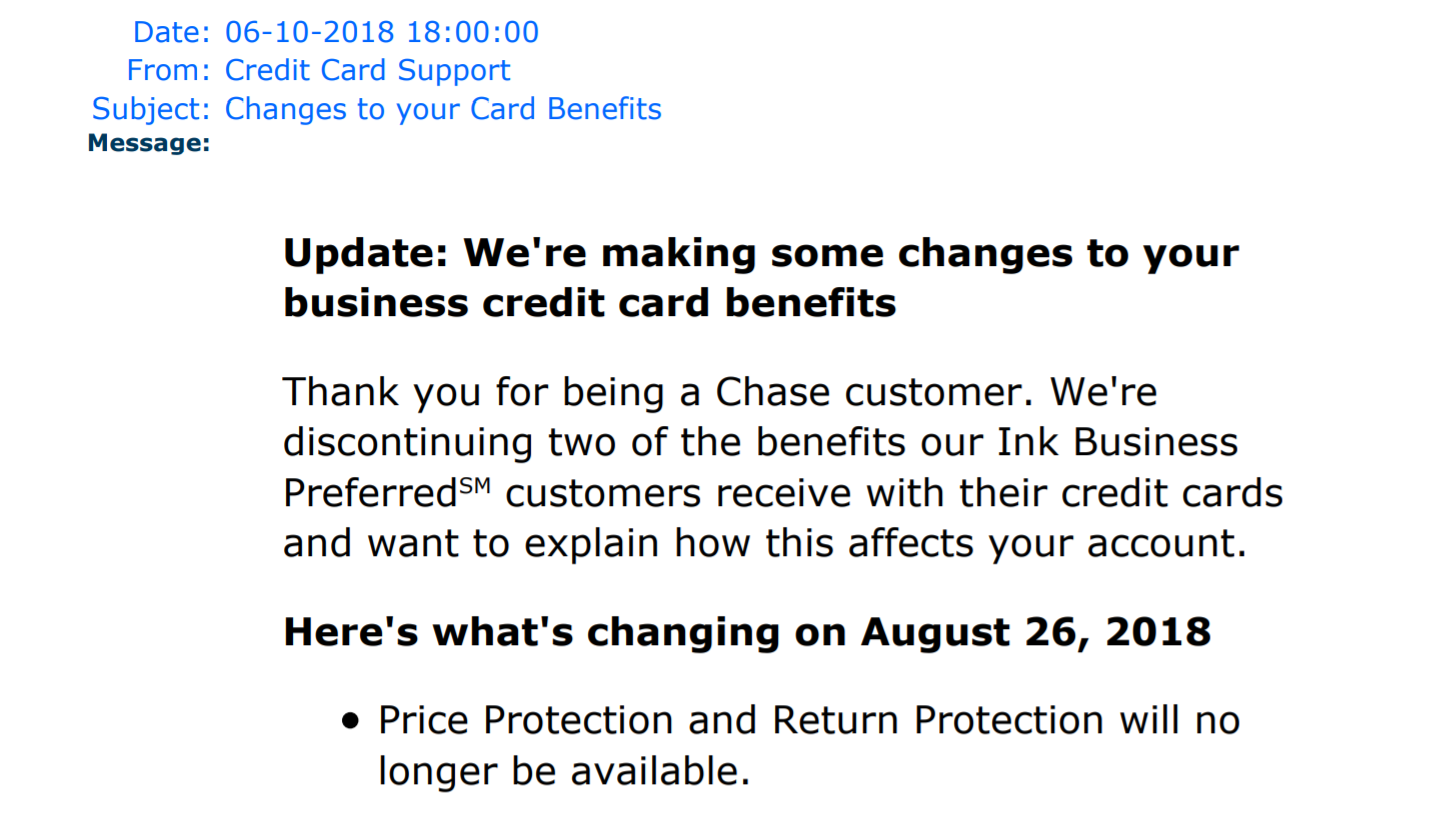

Now, we have another card cutback to add to the list. Chase sent out secure messages on Sunday to Chase Ink Business Preferred Credit Card cardholders announcing the elimination of price protection and return protection:

Until August 26, the Ink Business Preferred offers 90-day return protection, up to $500 per item and $1,000 per year. The price protection benefit offered through August 26 allows cardholders to file for a difference in price if they find a cheaper price with 90 days of purchasing an item, capped at $500 per claim and $2,500 per year. Then starting on August 26, both of these protection benefits will disappear.

Why all of these changes? Well, it turns out the bots are to blame. While in the past most cardholders would ignore — or barely utilize — these secondary card benefits such as price protection, the advent of auto-generated claims have caused an explosion in the number of claims and payouts that card issuers have had to shoulder.

One would think there'd be a middle ground here: either set a minimum claim amount — to avoid processing and paying out claims for 42 cents — or a maximum number of claims per year. However, the changes made by credit card issuers have been either to reduce the maximum payout per year (Citi) or eliminate the benefit altogether (Chase).