Debunking Credit Card Myths: Will I Always Earn Bonus Points With Certain Merchants?

Update: Some offers mentioned below are no longer available. View the current offers here.

We devote a lot of time to travel rewards credit cards here at TPG. By strategically opening and utilizing these cards, you can unlock valuable redemptions like first-class flights and luxurious hotel rooms. However, there are a number of misconceptions out there when it comes to credit cards, so today I'll wrap up our series that debunks these myths and allows you to begin planning for your next vacation.

Previous entries included having too many cards, closing a card you don't use, not paying your balance in full and paying an annual fee. Today I'll shift to one of the most popular ways of boosting your account balances: earning bonus points.

Myth #19: I am guaranteed to earn bonus points at certain types of merchants.

When it comes to travel rewards credit cards, one of the best ways to maximize your earnings is by using them strategically at different merchants. Depending on the type of purchase, you'll be eligible to earn bonus points by using certain cards. Some of my favorite cards that fit this bill include:

- Chase Freedom: (No longer open to new applicants) Offers 5x bonus points at rotating categories each quarter, which includes gas stations and commuter transportation in the first quarter of 2017

- Chase Sapphire Reserve: Offers 3x bonus points at restaurants and on a wide array of travel purchases

- The Platinum Card from American Express: Recently updated to offer 5x bonus points on airfare

Unfortunately, these bonuses do not always post as expected. This is all due to the relatively inane element of the financial industry known as merchant category codes (MCCs for short). In essence, every merchant is classified under a certain category, and if your card offers bonus points within that category, you should be eligible to earn a bonus when you swipe your card there.

In reality, it doesn't always work out that way. There are some merchants that are coded differently than you would expect, and you may wind up missing out on points as a result.

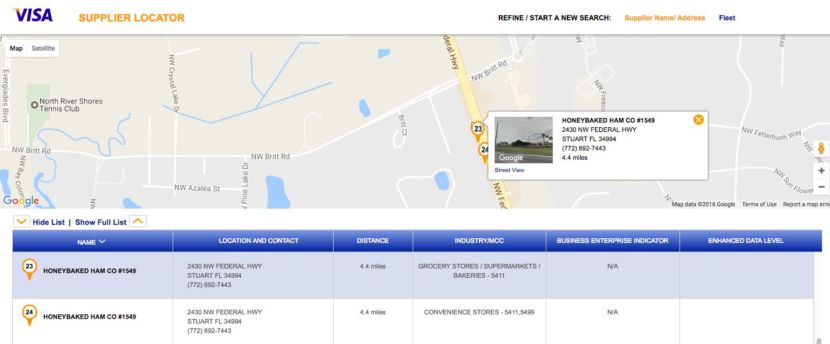

For example, back in June I visited the local Honeybaked Ham store to grab lunch while out shopping with my wife and daughter. I figured it would be coded as dining, so I used my Chase Sapphire Preferred Card (this was before the Sapphire Reserve announcement). However, I was surprised to see that I was only awarded 1 point per dollar spent when it posted to my account. When I visited this handy MCC look-up tool, I noticed two different entries for that particular location, neither of which was a restaurant:

The total was only $17.78, so I only missed out on 18 Ultimate Rewards point (worth a mere 38 cents based on TPG's most recent valuations). However, if I was counting on a large purchase earning hundreds or even thousands of bonus points, I'd be out of luck.

To prevent this from happening, I'd encourage you to start with the look-up tool I mention above to get an idea of how your purchase will be categorized. If possible, try making a small purchase before going for a larger one and check to see how it's categorized in your online account. Finally, if you find a discrepancy, consider bringing it to the attention of your card issuer. If it was a mistake on their part, they'll usually resolve it quickly. I found that to be the case when a Hilton stay didn't post properly on my Citi Hilton HHonors Reserve Card back in 2014, one that netted me close to 5,000 extra points. Unfortunately, if the merchant isn't coded properly (like with my Honeybaked Ham example above), there typically isn't anything the credit card company can do.

Bottom Line

When you use your credit cards at different types of merchants like grocery stores and gas stations, you'd like to think that you're getting all of the bonus points you deserve. Unfortunately, that isn't always the case, since some stores are classified in quirky ways that could prevent you from earning the double or triple points you'd expect. The best advice is to simply check your accounts each month to make sure that you aren't being shorted, but if the merchant isn't coded the way you want, you may be out of luck.

Have any of you missed out on bonus points because of an odd coding at a merchant?