How to Start Building Credit with an Authorized User Account

Update: Some offers mentioned below are no longer available. View the current offers here.

Getting started with the points and miles hobby is no small task, but it can be even more daunting if you're just starting to build credit. Today, new TPG Contributor Akash Gupta shares tips for doing just that, based on his own experience.

It's been about two years since I first received my Social Security Number (SSN) in the US as an international graduate student — and just a little over a year since I actually learned what to do with it. In light of this recent milestone, I've found myself thinking about how there are truckloads of information on racking up credit card points and miles, but very little guidance for people who have absolutely no credit history and are looking to enter the rewards hobby.

Most sources mention procuring a secured credit card first, and then painstakingly building one's credit over the course of many months. Another method is getting added as an authorized user on a card, which is what I will focus on in today's post. Following the steps below is a good way to start from zero and build a solid credit score relatively quickly — and ultimately get approved for the rewards cards you want.

Step 1: Choose The Right Card Issuer (and Cardholder)

Out of the three major card issuers — American Express, Chase and Citibank — only Amex asks for the SSN of an authorized user (both online and on the phone). Amex also tends to be quite lenient when it comes to approving people for its starter cards, even if they only have authorized user (rather than primary user) accounts on their credit reports.

Chase doesn't even give authorized users a separate card number, and Citi has to be requested specifically to add the SSN. Even then, though, it's difficult to qualify for your own Chase or Citi card, such as Chase Sapphire Preferred or Citi Prestige, with just an AU account. Meanwhile, Barclays, Discover, Bank of America and Capital One do collect the SSN of authorized users, and there's a good chance you'll be approved for your own card after being added as an authorized user with one of these issuers. However, this method has proved to be quickest and 100% successful with Amex.

If you're looking to be added as an authorized user, it's essential that you ask someone with an Amex (or other issuer) account in good standing. It helps if the cardholder has a good credit score as well — and this could even have a positive effect on your new score. Also, keep in mind that it doesn't matter what kind of card you're added to, as you won't be able to bank the rewards in any case.

Step 2: Request the Add-On

To get up and running, the primary cardholder needs to add you as an authorized user online or on the phone, making sure to include your SSN in the request.

Step 3: Start Spending and Pay on Time

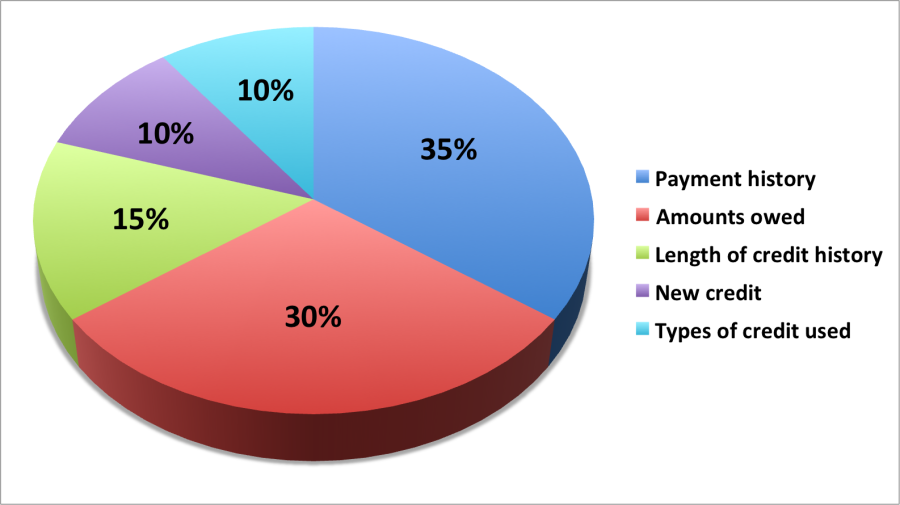

Once you activate and receive the card, create an online account for it. Then, you're set to start charging purchases to the card. To build credit, it's extremely important to pay off your balances for each statement on time. For more information on avoiding dings to your score, see Vikram Birring's post on 5 Lesser-Known Things That Affect Your Credit Score.

The Results

In less than two months, as an authorized user on a classmate's Amex PRG card, I saw a score of around 640 — previously I had been told that my credit reports were too thin to generate a score. Already in Amex's systems, I then applied for a Blue Cash Everyday® Card from American Express (I was rejected for it just two months earlier) and was instantly approved. I removed myself as an authorized user, and the account disappeared from all credit reports shortly, except from that of Transunion (removal has to be requested manually in some cases).

A month into the Blue Cash card, I applied for a Chase Freedom card (No longer open to new applicants) and was instantly approved again! Note that both my initial applications were for starter-level cards with the respective banks; don't expect to be approved for more premium plastic like the Platinum Card® from American Express when you're just getting started.

After just three more months of responsible credit management, I was approved for my own Premier Rewards Gold Card from American Express, Chase Sapphire Preferred and the Citi / AAdvantage Executive World Elite Mastercard in the same week — all cards that require excellent credit. Fast-forward one year and nine applications, and I've never been rejected for a credit card again, and have accumulated over 500,000 miles and points through bonuses, all while being a student with virtually no income.

Bottom Line

Was my experience just a one-off case? Absolutely not. I've used the same strategy to help five of my friends. Two of them got a 650+ score from scratch in just one billing cycle and within less than three weeks of being added as an authorized user! After waiting out the second billing cycle, they were also instantly approved for their own starter-level Amex cards. This process helped us out, and it will likely do the same for anybody else in the same boat.

For more information on getting started with credit cards — particularly those of the points- and miles-earning variety — check out TPG's Beginner's Guide.

What are your favorite tips for getting started with building a good credit score?